Chile’s privatised pension insurance is one of the most celebrated and indeed imitated arrangements of its kind in the world today. The system of privatised accounts managed by private funds introduced in 1981 was deemed to be so successful that it became a model from which countries as diverse as Poland and Nigeria have borrowed elements from. In 2004, US President George W. Bush even went so far as to call it a “great example” which America could learn “lessons from” when reforming its own pension system. If imitation is indeed the sincerest form of flattery, then Chile’s pension system clearly has a lot of admirers.

The murky political setting from which Chile’s pension revolution arose cannot be avoided, however. In the early 1980s, Chile was ruled by the military regime of General Augusto Pinochet – now widely acknowledged to have committed numerous human rights abuses, including the kidnap, torture and murder of large numbers of its own citizens.

In democracies, welfare reform is always challenging, not least because those who are accountable to the electorate are mindful that somebody almost always loses out. ‘Win-win’ scenarios, as we will see, are very much a rarity in pension reform. But for reasons that should be obvious, a public backlash is not something the Pinochet regime would have spent too much time agonising over.

The ‘Chicago Boys’

General Pinochet first seized power following a military coup d’état on 11th September 1973, that came about after a severe economic crisis and perceived breakdown in democracy destabilised the presidency of socialist leader Salvador Allende. After deposing Allende, who died in uncertain circumstances as troops surrounded La Moneda Palace, Pinochet’s first priority in power was to do something about Chile’s inflation-ravished economy. With no economic expertise within their own ranks, the military regime brought in a group of Chilean economists educated in Chicago under the tutelage of the eminent American economist Milton Friedman.

“So severe was the danger of a complete collapse, small minor tweaks would not suffice. The country, the Chicago Boys said, needed nothing less than a form of economic shock therapy.”

The ‘Chicago Boys’, as they came to be known, were just about the counter opposite of the Allende regime in ideological terms. While Allende’s government had seen the solution to Chile’s economic predicament as more nationalisation and more central planning, the Chicago Boys, in stark contrast, advocated leaving market forces to steer the economy.

But so severe was the danger of a complete collapse they argued, that small, minor tweaks would simply not suffice. The country, the Chicago Boys said, needed nothing less than a form of economic ‘shock therapy’, an unfortunate term – given the grim political realities amid which the policy was implemented – that had been coined by their mentor, Friedman. A multitude of free market polices were subsequently introduced in a very short space of time. Government intervention and public enterprises were restricted; businesses expropriated under Allende were returned to the private sector; price controls were abolished and financial markets deregulated; labour unions were suppressed; and progressive taxes either abolished or significantly reduced.

Within a couple of years, inflation began to return to more manageable levels and, after the recession of 1975, growth began to accelerate once again, thanks largely to a surge in foreign direct investment, and the country entered into a boom that would last the rest of the decade. Now, spurred on by shock therapy’s apparent success, the Pinochet regime set its sights on the state’s final remaining frontier: the welfare system.

The Piñera plan

Social security in Chile first came into being in the early 1920s with reforms that established a system in which retirement income was provided by a range of state administered pay-as-you-go (PAYGO) pension funds. PAYGO schemes have, perhaps unfairly, been likened by some to a “Ponzi” scheme: active contributors finance retirement payments to pensioners and increasing obligations are supposedly met by both drawing on the stock of accumulated savings and their accumulated net income. This arrangement worked, to begin with. However, by the early 1970s benefits had been increased to such a degree that the system in Chile was no longer financially sustainable, even if the government chose to raise contribution rates (which were, by that time, already representing more than 50% of a workers annual salary).

José Piñera, Chile’s Minister of Labour, and one of the leading members of the Chicago Boys, had longed for many years to oversee the overhaul of Chile’s pension system. For Piñera, the Bismarckian PAYG system inherited by the Pinochet regime was an anathema to his laissez-faire principles. For one thing, the system was mildly redistributive. However, in Piñera’s eyes the worst sin of all was that it almost completely ignored the investment potential of the market. In the late 1970s he drew up a plan that would radically change that.

On 4th November 1980, the military government approved decrees designed to reshape the country’s pension system. The state managed and, by then, insolvent pension regime, was to be replaced by a system based on individual retirement accounts administrated by private companies, or “administradoras de fondos de pensiones” (AFPs).

All Chileans already in employment – with the exception of the armed forces – would have a choice on whether to opt in to the new scheme, or remain on the ‘grandfather’ system, but were offered financial incentives to go private. New entrants to the labour market however, were not offered the former state pension. Under the new, privatised system, workers no longer paid a social security tax to the state or collected a state-funded pension. Instead, those that opted to switch to the new system were required to deposit 10% of their wages to an AFP of their choice. Workers were also free to contribute an additional 10% of their wages each month if they hoped to retire early or obtain a higher pension. One of the keys to the new system was the ability for contributors to change from one AFP to another. That helped to foster competition between the various providers to offer a higher return on investment, better customer service and lower commission.

Once the age of retirement is reached, Chileans on the private scheme had two options. First, a programme of withdrawals could be set up, subject to limits based on the life expectancy of the retirees and their dependents. Alternatively, contributors could choose to use capital in their account to purchase an annuity from a private life insurance company.

“Miracle of Chile”

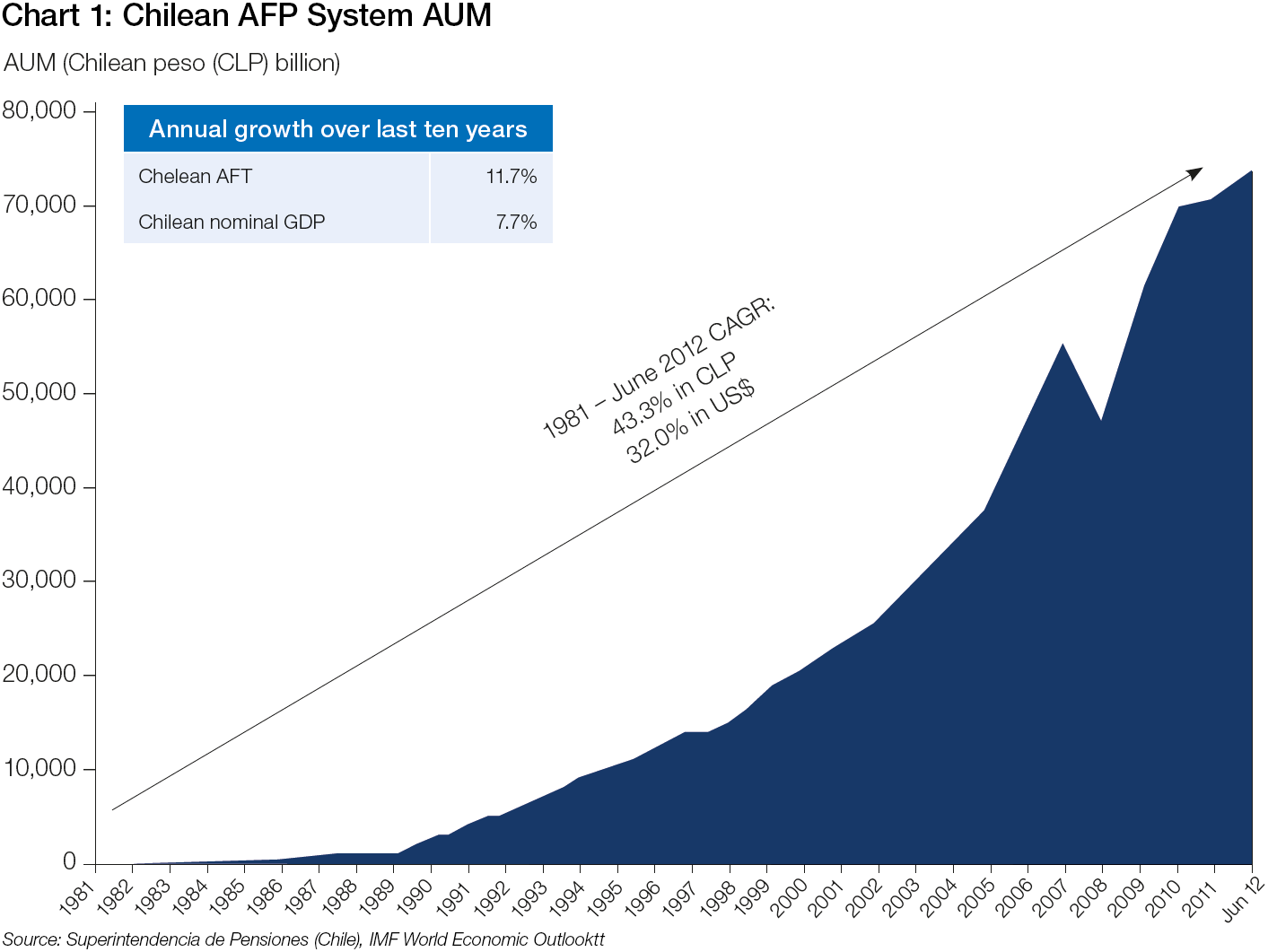

There was clearly much to admire in the new pension system Piñera helped establish. Since the system became active on 1st May 1981 the funds have averaged a real return on investment of around 10-12% per year, around three times higher than even Piñera himself anticipated. Of course, like with any investment vehicle, annual yields have fluctuated to a degree, however, when it comes to pensions, it is the average over the long term that is important.

Chart 1: Chilean AFP System AUM

AUM (Chilean peso (CLP) billion)

Source: Superintendencia de Pensiones (Chile), IMF World Economic Outlook

There were some knock-on benefits too. As Chileans began to deposit money into the new private scheme, a huge pool of capital, approximately $162 billion or 62% of GDP, accumulated. When this capital began, in turn, to be invested back into the Chilean economy it provided an enormous boost in investment, helping to drive the growth surge of the 1980s that some observers, including Piñera’s one-time mentor Friedman, called the “Miracle of Chile”.

Using these facts, Piñera has been able to make a convincing case that his reforms were not only the right thing to do economically, but also from a social justice perspective. “The new pension system has made a significant contribution to the reduction of poverty,” he claimed in a recent by-lined article for The Washington Post. This feat was accomplished, he continued, by “increasing the size and certainty of old-age, survivors and disability pensions and by the indirect, but very powerful, effect of promoting economic growth and employment.”

Ageing gracefully?

The general thrust of Piñera’s argument is difficult to dispute. With a measure as radical as wholesale privatisation of a public benefit scheme, however, debate was always going to be polarised to some degree. In recent years, Chileans, now ruled democratically, have revisited the Piñera reforms and a number of shortcomings have been highlighted.

One of the perceived shortcomings was a lack of universal coverage. Private pensions, by their very nature, only covered those Chileans who had paid in. Therefore, labour market trends, such as long periods of unemployment, informal employment or withdrawal from the labour market due to family obligations, meant that a significant number of workers – up to 40% by some estimates – were not making the regular payments that would guarantee them an adequate pension in retirement. Something had to be done.

In 2008, the Chilean government, under the presidency of the Socialist Party leader Michelle Bachelet, decided the time was right for a revamp. But the Piñera reforms were not swept under the carpet entirely – at least for the time being. Instead Bachelet government brought in a World Bank-approved “three pillar” reform to provide a basic universal pension for individuals within the bottom 60% of income distribution not covered by a private scheme. Under the new system, individuals who did not contribute to a pension during their working life are provided with a small monthly sum of around $150, while those who did contribute but accumulated little are entitled to an additional subsidy of the same amount.

The overhaul may not stop there, however. This year, Bachelet was elected for a second time after winning a landslide victory over the conservative Independent Democratic Union candidate, Evelyn Matthei. On the campaign trail, Bachelet made repeated promises to look again at the private pension system, and analyse whether it has lived up to its promises. No formal decision has been made, as yet. However, conservative opponents are concerned that this might spell the end for a system which they say remains the “envy of the world”.

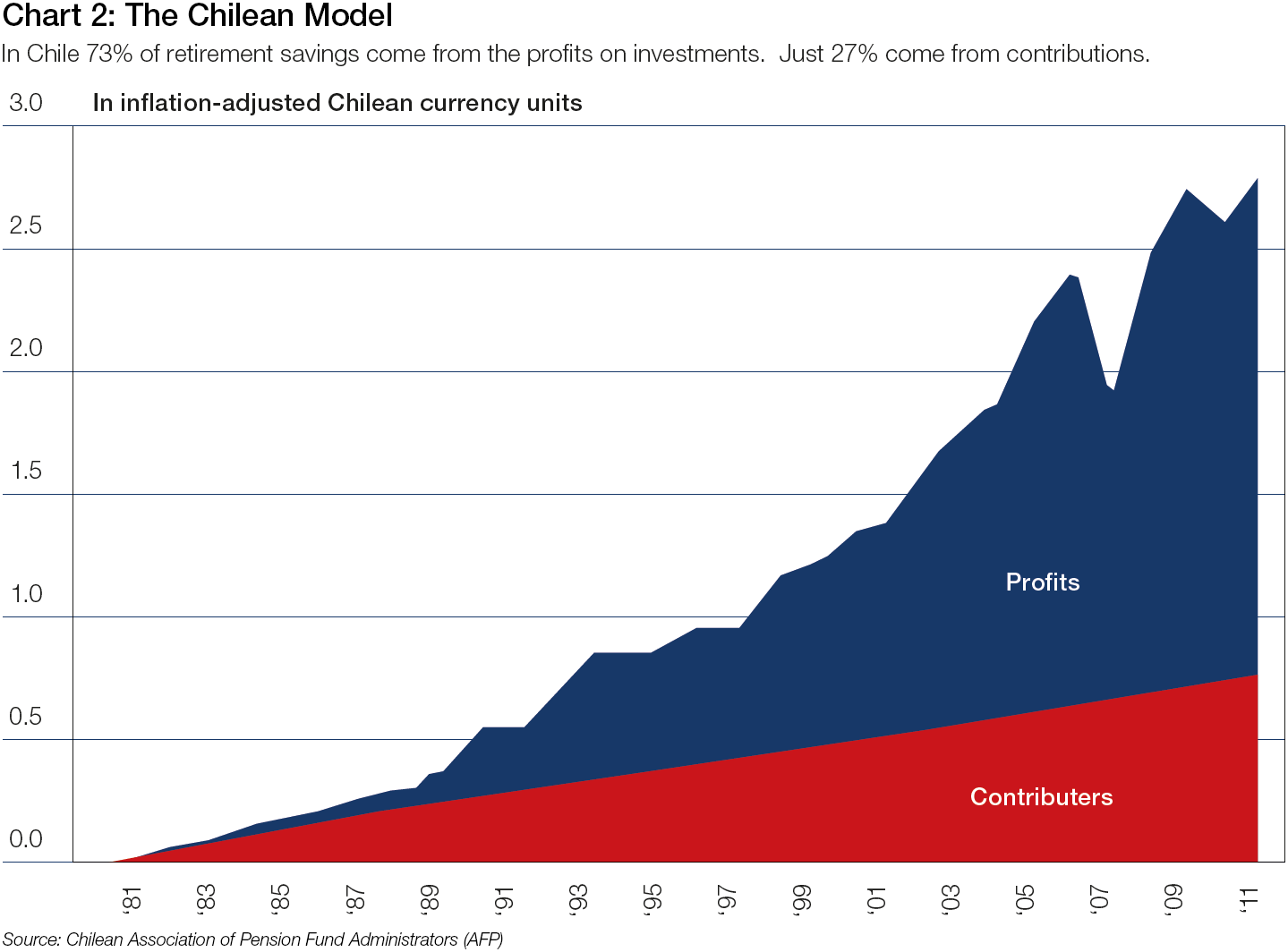

Chart 2: The Chilean Model

In Chile 73% of retirement savings come from the profits on investments. Just 27% come from contributions.

Source: Chilean Association of Pension Fund Administrators (AFP)

Learning from Chile

But should other countries continue to hold Chile up as an example to envy and to learn from? The reforms introduced by Piñera certainly helped to bring dynamism to the Chilean economy and addressed the shortcomings of the old system (the same shortcomings many state pension systems in the West are now grappling with). But the large numbers of Chileans left without pension coverage shows us that the system was not perfect. A system that fails nearly half of its population cannot, after all, claim to be an unmitigated success. This, perhaps, helps to explain why, where countries have sought to learn from Chilean pension reform, few have chosen to import the model wholesale.

Instead, most countries have sought to borrow the most successful elements of the reform – namely personal accounts with private providers leveraging the investment potential of the market – but balanced with the option of state provision to provide coverage for those who still need it.

There may also be another reason why other countries have struggled to follow the Chilean plan to the exact letter. That reason is consent. It goes without saying that the experiment undertaken by Chile over a quarter of a century ago was highly radical in its nature. Indeed, the system that was adopted was – and remains – so radical that it seems doubtful many democratically elected governments would view it as a practicable solution.

Even former UK Prime Minister, Margaret Thatcher, a close friend of Pinochet – and hardly someone who could be accused of harbouring socialist sympathies – dismissed the idea of following Chile’s example as too extreme when it was suggested to her. Chile, she was reported to have said, was indeed a “remarkable success” but added that Britain’s “democratic institutions and the need for a high degree of consent” make “some of the measures” taken to reform pensions “quite unacceptable.”

The extent to which other countries can follow Chile though may be beside the point, though. Back in 1940s war-torn Britain, William Beveridge, to many the founding father of the welfare state, designed a system of state administrated insurance to protect citizens from the risks associated with life events – such as old age – that could see them slide into poverty. What José Piñera proved was that it is possible, to an extent, to take the state out of the equation in the provision of such insurance. And when that happens, those who are covered often find themselves better off as a result. “The ultimate lesson,” he later wrote, “is that the only revolutions that are successful are those that trust the individual, and the wonders that individuals can do when they are free”.

Please enter the email that you signed up with below. If your email is

connected to a member account, we will send you a reset link.

This website uses cookies and asks for your personal data to enhance your browsing experience. We are committed to protecting your privacy and ensuring your data is handled in compliance with the General Data Protection Regulation (GDPR).