In an environment where banks continue to feel the impact of regulation, collateralised products open up a new world of opportunities for investors. Tri-party repos, for example, can offer investors both sustained revenues and lower risk – a genuine breath of fresh air for corporate treasurers in today’s low-yield environment.

Pascal Morosini

Executive Director, Global Head of GSF Sales and Relationship Management

Pascal Morosini is Executive Director, Global Head of GSF Sales and Relationship Management, at Clearstream.

Pascal joined what was then Cedel Group in 1994 to work in collateral valuation operations. In 1997, he moved to triparty repo operations, and two years later he joined Clearstream Banking’s Customer Relations Department as a Global Securities Financing sales specialist. He is now responsible for sales and relationship management for all GSF products worldwide.

Pascal holds a Diploma in Banking Management from the “Centre Universitaire de Luxembourg” and has also participated in the Clearstream Banking Global Markets training programme.

Corporate treasurers could be forgiven for viewing tri-party repos as a complicated type of transaction. The reality, however, is not nearly as complex as some might think. Indeed, tri-party repos are one of the simpler forms of secured investment: they are essentially bank deposits secured by independently held and managed assets.

And in the current economic environment, that security could not be more welcome. Several high-profile bank failures in recent years have highlighted that unsecured bank deposits are not necessarily as safe as they were previously considered. Yet some corporates have more cash on their balance sheets than ever before – which presents them with somewhat of a dilemma.

Increasingly, corporates are thinking outside their traditional investment boxes and as a result, tri-party repos are falling into favour. A tri-party repo offers corporate investors the advantage of collateral (in the form of securities) in return for depositing cash for the duration of the transaction.

“It allows corporates to either diversify their counterparty network or lend more cash with their house banks if unsecured lines are already fully utilised”, says Pascal Morosini, Executive Director, Head of Global Securities Financing Sales and Relationship Management at Clearstream. “But the biggest and undisputable advantage is that tri-party repo is much more secure than cash deposits.”

Driving the market

One of the key drivers of the growth in the tri-party repo market is regulation. For large corporates who have obligations under the European Market Infrastructure Regulation (EMIR) or Dodd-Frank to post collateral for OTC derivative transactions with central counterparties, tri-party repo offers a significant advantage over alternative products. “The collateral corporates hold against cash can be sold immediately should a counterparty default. This collateral can also be used to cover derivative liabilities that corporates have with their prime brokers and clearing members,” explains Morosini.

For this reason, tri-party repo is increasingly considered an alternative to money market funds (MMFs) for corporates with cash to invest in securities. Additional regulation in the MMF space is also causing corporate investors to turn towards tri-party repos.

Against the backdrop of regulatory pressure on investors, tri-party repo presents an opportunity for corporates, who to date have largely invested their cash on a unsecured basis, to invest in collateral-backed deposits.

“The low-yield environment, which continues to put a strain on investors, is another reason why now may be a good time for corporates to move into the tri-party repo market. Subject to the type of collateral investors are willing to receive in return for their cash, the yield on tri-party repos can even sometimes beat what they are earning on their current investments,” notes Morosini.

Role of the tri-party agent

Clearstream, a leader in the tri-party repo market, acts as collateral agent and securities depository (ICSD). In its custodian role it holds accounts for banks and global custodians, who in turn hold securities on behalf of their clients. More than €12 trillion of deposits are held within Clearstream by around 2,500 customers around the world. In its tri-party collateral agent role, Clearstream manages collateral worth more than €650 billion for more than 550 customers.

“Clearstream acts as a neutral collateral agent, handling all the administration related to the transfer of collateral from one counterparty to another,” says Morosini. “We value and allocate the collateral, monitor and process substitutions, execute margin calls, issue reporting and maintain and cross-check the eligibility criteria. In essence, our role is to ensure that sufficient eligible securities are transferred to cover any given exposure at any moment in time.”

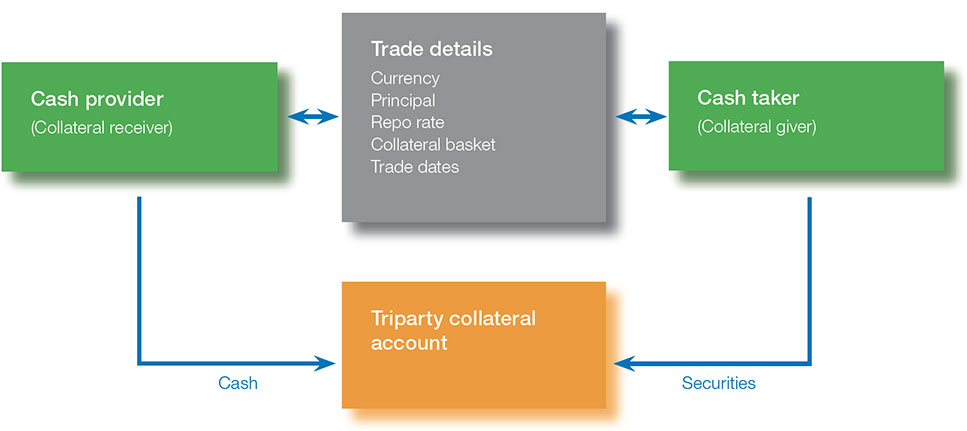

Chart 1: How it works, Clearstream tri-party repo service flow diagram

The company’s role as tri-party agent is an important risk mitigation factor, as Clearstream is not directly part of the transaction. This neutrality guarantees – for both parties in a transaction – that should one default, the collateral will remain segregated and be immediately available for resale.

In addition, Clearstream’s tri-party repo service offers a number of unique features. The principal trading relationship remains between the counterparties, and only one signature of the Collateral Management Service Agreement (CMSA) with Clearstream Banking as the agent is required. Collateral profiles (either customised or designed according to industry standards) are predefined within the CMSA appendix, making it very easy and straightforward to sign up for the service.

Furthermore, the tri-party repo service presents distinct advantages to both the givers and receivers of collateral. Collateral givers can finance a broader basket of assets, tap into new sources of financing, use automatic asset allocation and unlimited substitutions, and be assured of optimal collateral allocation across products and locations. Receivers of collateral benefit from security of holding, an optimised balance sheet, low maintenance costs and full reuse of the collateral received.

Elsewhere, the outsourcing of back office operations to Clearstream provides corporates with access to a wide range of counterparties across the world. Clearstream clients have full control over their asset portfolio and benefit from efficient use of their cash and securities as well as from risk management solutions tailored to their individual needs. The solution is a flexible money market instrument at the heart of Clearstream’s Global Liquidity Hub which can form an integral part of a corporate’s wider liquidity strategy.

Clearstream offers a full suite of products under the Global Liquidity Hub, ranging from securities lending and borrowing to the posting of initial margin to central counterparties for cleared OTC derivative trades. The growing desire of corporates for greater security of the money they deposit with banking partners is reflected in the growth of the Clearstream platform, which now has more than 30 corporate users, with a combined $25 billion in cash.

In practice

For a cash provider using Clearstream, once a tri-party repo deal is concluded, the user instructs its back office to pay the cash to its Clearstream account via its cash correspondent bank. Once this has cleared, Clearstream arranges the simultaneous exchange of the cash on the account for the securities from the counterparty. A core feature of the Clearstream platform is its delivery versus payment (DVP) functionality, which ensures that cash is not paid to the counterparty until the securities have been received, meaning the investor is never exposed.

Users must also inform Clearstream of the transaction with the counterparty; this can be carried out via various channels, including the 360T platform, the Bloomberg Professional service, or Clearstream’s own CmaX online communications portal. “Once you have deposited the cash in your Clearstream account and informed us of the transaction, you do not need to handle the collateral side of the transaction,” says Morosini. “Clearstream handles all the administration of the transaction, and the investor can remain passive until the transaction is automatically unwound.”

What’s in it for corporate treasurers?

Tri-party repo was initially created as a means for broker-dealers to maximise the use of small asset positions left in their accounts. Today it has expanded to cater to the needs of the larger corporate world. Though initially conceived as an inter-bank product, Clearstream’s platform is bringing tri-party repo to a much broader market. “Clearstream is opening the door for corporates to the tri-party repo market,” says Morosini. “We are facilitating and streamlining access to our state-of-the-art Global Liquidity Hub with our simplified legal agreements. Our goal is to industrialise and commoditise this product and offer it to a much wider audience so they too can reap the benefits.”

Indeed, greater numbers of corporate treasurers are starting to see the benefits of sustained revenues with lower risk that tri-party repo can offer.

In short the benefits could be summarised as follows:

Access to a broader range of counterparties, thus diversifying risk and creating yield enhancement opportunities.

Security: cash loans are secured by collateral in the form of securities.

Simplicity: trades are negotiated like cash deposits.

Outsource back office workload: all the administration regarding the management of securities is done by Clearstream

Simplified legal documentation for instant access to a large number of counterparties.

Evolution and innovation

But what makes Clearstream’s offering stand out? For starters, Clearstream’s tri-party repo product has matured with the market, meaning that since its launch in Europe in 1992, the service has become more flexible through the implementation of a streamlined signatory process. Users of the service have also benefited from the ability to re-use securities within the system, a feature that was put in place in 2006.

The company’s collateral management exchange engine (CmaX) has also been developed as a result of its longstanding industry experience and close market consultation.

Building on its core tri-party repo offering, Clearstream launched its GC Pooling product in 2005 in collaboration with Eurex Clearing AG, the central clearer of the Deutsche Börse Group. “This is essentially a tri-party repo transacted through a central counterparty with full counterparty anonymity. This product, which has on average €180 billion of outstanding, dramatically lowers risk to counterparties for corporates. It is currently unrivalled in the market and is now available for corporates,” Morosini explains.

In addition to these innovative products, Clearstream’s principal lending product ASLplus was launched in 2006. Through this service, Clearstream borrows securities (mainly high-quality assets such as government bonds) from its custody clients and re-lends them in its own name under a principal structure (as opposed to an agency structure). ASLplus, which is the market leader in terms of German government bond distribution, has around €50 billion outstanding.

A principal agreement is required to trade repos. This could be a Global Master Repurchase Agreement (GMRA), a document traditionally used for bilateral interbank repo trading which is negotiated with each counterparty individually. Some corporate treasurers have been deterred from trading repo as the negotiation process can be cumbersome and numerous provisions apply solely to bilateral repo, and are hence not relevant for those wishing to use tri-party repo.

Clearstream has sought to simplify the process by designing a standardised tri-party-only principal agreement, the Clearstream Repurchase Conditions (CRCs). Like the CMSA, this agreement is multilateral and only needs to be signed once with the agent. Counterparties do the same and the relationship is formed by acceptance of the collateral receiver’s eligibility criteria. The combination of the CMSA and CRCs effectively gives corporate treasurers membership to a club within which they can trade with other members without having to sign further agreements. The standardised nature of this setup saves both time and legal costs. This innovation alone can speed up the process for accessing tri-party repo counterparties by up to 12 months for corporates – particularly small and medium-sized companies.

Beyond innovation, Clearstream also prides itself on the level of service it offers its customers and the advanced technological portal through which this is provided.

And as more corporates start to appreciate the potential benefits of tri-party repo, these unique features, believes Morosini, will see Clearstream’s market share continue to grow. After all, Clearstream’s tri-party repo service offers the advantages of being secure and sophisticated, while at the same time being simple and transparent for corporates to set up.

Clearstream

Clearstream is part of the Deutsche Börse Group and provides post-trade services to financial and corporate customers in more than 100 countries with access to 54 markets.

Our tri-party repo services through our Global Liquidity Hub provide corporate treasurers with a safe, flexible, collateralised money market product with innovative options including a unique ‘one time’ master repurchase agreement (CRCs) and end-to-end integration with vendors such as 360T.

With access to trade reporting services via REGIS-TR and OTC derivative clearing via Eurex, the Deutsche Börse Group offers a ‘one-stop-shop’ for all your treasury activities.

Please enter the email that you signed up with below. If your email is

connected to a member account, we will send you a reset link.

This website uses cookies and asks for your personal data to enhance your browsing experience. We are committed to protecting your privacy and ensuring your data is handled in compliance with the General Data Protection Regulation (GDPR).