Although China’s bond market is the third largest in the world, with USD 9 trillion1 outstanding, the concept of corporate bond defaults – or indeed downgrades – has until now been alien to the vast majority of local retail and institutional investors. However, with default rates now on the rise, investors increasingly need to understand the credit risks when investing in China, and the ways to mitigate them.

Rising corporate default rates

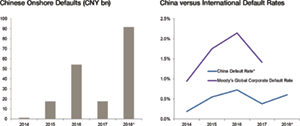

Prior to 2014, China had never suffered a corporate default. Entities encountering financial difficulties were either taken over or bailed out, which ensured that investors never suffered losses, but also reinforced the perception of an implicit government guarantee and intensifying moral hazard.

The Chinese government’s efforts to eliminate this moral hazard, improve capital allocation and create a closer link between risk and return have been the trigger for the gradual financial evolution witnessed over the past decade. These regulatory changes cumulated with the new Asset Management Product (AMP) rules announced in April 2018, designed to curtail shadow banking activity, remove implicit guarantees and improve investment transparency.

However, a significant side effect of these new AMP rules is the reduction in access for borrowers who previously used shadow banking channels for funding. With formal lending channels also tightening, the number of defaults in China has risen sharply, reaching a record high in 2018 (although defaults remain low relative to global bond markets2).

AMP rules triggered defaults, as overall credit profiles improve

Source: Bloomberg, Wind, and J.P. Morgan Asset Management; data as of 18 October 2018.

*The ratios are median numbers in S&P coverage. Default rates are the number issuers defaulting divided by the number of total issuers. 2018 default rates and amount are estimated.

Credit analysis is challenging

For bond and cash investors, understanding credit and counterparty risks in China has therefore become increasingly important.

However, credit analysis is challenging, due to a combination of opaque financial data, complex financial interconnections and an inconsistent domestic ratings system that rates 70% of issuers triple A and 97% of issuers AA- or better3.

Often, there are large differences between the domestic and international ratings for many Chinese banks and corporates. Onshore credit spreads reflect these differences.

De-leveraging has stabilised banks’ credit profiles

Source: Bloomberg, Wind, and J.P. Morgan Asset Management; data as of 18 October 2018.

To address these challenges, investors should focus on the issuer’s potential level of government support and its standalone credit profile.

The first of these factors – government support – remains important. But is should not be overestimated. Only a limited number of issuers enjoy strong government links – especially those with social benefits, monopolies and direct government involvement. Other issuers may have weak government support from lower ranked provincial or city governments.

Increasingly important is an analysis of the issuer’s capital, earnings, liquidity and management. Similar to western financial markets, a “bottom-up” approach to understanding the issuer’s financial condition, resiliency and quality is critical in determining the issuer’s willingness and ability to repay their debts.

Adopt a rigorous credit process

Slower economic growth and tighter financial conditions have created a challenging environment for many Chinese bond issuers. This suggests a growing likelihood of further defaults.

In this environment, it’s vital for investors to adopt a rigorous credit process that primarily focuses on the credit profile of an issuer’s counterparties, while also considering the level of government support. Such rigorous credit analysis should help investors minimise the risk of suffering downgrades or defaults when investing in China.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.