Once upon a time, most treasurers did not have much direct involvement in tax planning. Tax decisions were typically left to the specialists, while treasurers got on with doing what they do best – managing cash.

Things are starting to change. Whether it’s the unorthodox methods that companies like Apple are using to deal with their trapped cash, or meeting the requirements of regulations such as the Foreign Account Tax Compliance Act (FATCA), tax issues are assuming an increased importance in the world of corporate treasury. Tax and treasury have always sat side-by-side, structurally, within most organisations. And there are, for that very reason, a number of businesses that have a single head of both functions. One such company is Irish airline Aer Lingus. “Aer Lingus, like a number of other companies, has recognised that there is a close relationship between tax and treasury,” says Tom Milligan, the group’s Director of Insurance, Tax and Treasury. “Whether it is managing assets and liabilities, or compiling forecasts, tax and treasury here are absolutely working together.”

Having responsibility for both tax and treasury sometimes pulls Milligan into strategic debates in areas that might be unfamiliar to the average treasurer. Fleet planning is a case in point. Aer Lingus’s aircraft fleet is comprised of owned, operating-leased, and finance-leased aircraft. When the company plans to expand its fleet, a process which typically begins many years in advance, it does so on the basis of available seats per kilometre (ASK), an equation that is used in commercial aviation to measure passenger carrying capacity. But in order to provide these ASKs, the most tax-efficient route to financing the fleet must first be determined.

It is no surprise then that Milligan and his treasury team are heavily involved in the decision-making process. “How those aircraft come into the fleet will be a combination of those owned, operational-leased and finance-leased methods decided by the fleet planning committee, which I sit on,” explains Milligan. “And I can bring to that committee both the tax and financing implications of the different methods of bringing those aircraft in.”

Working side-by-side

The point is that when financing expertise is combined with in-depth knowledge of tax affairs, it can help the business to achieve the most tax-efficient financing structure: something which can be of enormous strategic value. Keeping tax under the same roof as treasury is not an arrangement unique to Aer Lingus, but it is not particularly widespread either. Where it does exist, it is very often the case that one of the disciplines – tax or treasury – remains the main area of expertise, with a team helping with the management of the other area.

“You don’t tend to get tax and treasury managers so much anymore,” says Mike Richards, Managing Director of MR Recruitment. That is at least partly because tax management is seen as an area that requires a high-level of knowledge expertise, he explains. “There are treasurers, who, of course, have a good knowledge of tax. But it is such a specialism – even more so than treasury – that the roles are more often than not kept separate.”

Nevertheless, the fact that such roles do exist tells us something about the closeness of the two functions. This proximity demonstrates that, even when the two functions are managed separately, it is still a good idea for treasurers to develop a rounded understanding of the tax implications of their decisions – even if most do not require quite the same level of expertise as Milligan does in his role. If the treasury and tax manager are not the same person, then they are at least very likely to be working ever more closely together.

Synthetic repatriation

Working closely together can have a number of other benefits. The first of these concerns the growth of cash stockpiles on the balance sheets of many multinationals in tandem with the availability of cheap financing on the capital markets. To illustrate the point, it may be useful to look at a funding deal recently secured by a large consumer electronics company. In April 2014, Apple announced one of the largest corporate bond offerings of the year so far. The $12 billion bundle of floating and fixed-rate notes ranging between three and 30 years were issued in order to help the tech giant fund a $90 billion share buyback programme. To observers, however, there was something initially puzzling about the news. Why would the world’s most cash-rich company – with a reported $150 billion cash pile on its balance sheet – need to go to the bond markets for financing? Would it not be cheaper for the company to finance the buyback through its cash reserves instead?

The reason it didn’t, of course, is corporate tax. Nearly all of the cash on Apple’s balance sheet is held by overseas entities and had the company chosen to fund the buyback by bringing home all of its cash from international operations then it would, under US tax law, have been obliged to pay 32% to the Inland Revenue Service (IRS). For Apple, that would have meant a whopping $45 billion tax bill. Considered in that light, it’s not difficult to see why, especially in the current ultra-low rate environment, Apple’s financial executives saw a bond issue as the cheapest way of meeting the company’s domestic cash needs. This strategy is not unique to Apple. A recently published report by Standard & Poor’s analyst Andrew Chang looked at roughly 1,700 US-based multinational companies and found that debt has become a very significant factor in the growth of cash on the balance sheet for a lot of these companies.

For every dollar of cash they accumulated over the past three years, debt increased by almost $4, the study found. At first, the cash flow of most of the companies analysed appears to be more than sufficient to meet their domestic needs – be that capex, buybacks, or dividends. But when Chang looked at it more closely he realised that a substantial amount of the cash on the balance sheet was coming from flows that were being generated overseas. Companies were understandably reluctant to repatriate these flows under the current US tax code. “Essentially there is a mismatch of cash flow and cash uses,” Chang tells Treasury Today. “What we found was that a lot of companies are now issuing debt at very low interest rates in order to ‘synthetically’ access the cash that they have overseas as an alternative to paying a very high rate of tax. This is a trend which we expect to continue over the near term, barring any significant tax reform in the US.”

Changing regulation

The other main trend that is forcing treasurers to become more mindful of tax issues is regulation. Today, the introduction of regulation means that treasurers simply cannot ignore tax issues. FATCA, which came into effect at the beginning of July 2014, is the most significant of these. The regulation was introduced by the US government to prevent US taxpayers from avoiding tax by investing through non-US financial institutions and offshore investment vehicles. Although FATCA is aimed at financial corporates, in certain circumstances treasury centres and holding companies could find themselves defined as a foreign financial institution (FFI) under the regulation. Some treasury centres will be exempt, but the obligation will be on tax and treasury managers to evaluate whether they or their subsidiary is defined as a FFI under the regulation or not. Whatever the outcome, it means more regulation for the treasurer to understand and digest, as Aer Lingus’s Milligan acknowledges. “Compliance around tax is assuming a much greater focus than it had a couple of years ago and a lot of it is to do with anti-avoidance legislation such as FATCA,” he notes.

There is also the prospect of a co-ordinated tax on financial transactions in Europe. As with FATCA, banks and other financial institutions are meant to be the primary target of the proposed Financial Transactions Tax (FTT). Nobody is in any doubt, however, that end users such as corporates would also suffer, indirectly, if one were to be introduced. In fact, with the levies expected to put a squeeze on liquidity in the bond and derivatives markets, nearly every area of treasury operations – from intercompany funding and risk management to external financing – could be affected to some degree.

Owing to political disagreements, the probability of such a tax being introduced across every EU country now appears unlikely. But experts say that the prospect has still given companies some pause for thought, particularly with respect to how their treasury operations are organised across geographies. “I have heard some anecdotal evidence that some companies might move some of their treasury operations out of the FTT countries into non-FTT countries, simply so that the FTT won’t be an issue when or if it is implemented,” says Capita’s Fleming. “That would be an extreme step, but it will definitely be a consideration for some. And I think a few may well do that depending, perhaps, on the scale of their hedging activities in Europe.”

So recent regulatory demands, just like the issues around trapped cash, are certainly impacting, not only the way tax and treasury departments interact with one another, but also wider strategic decisions taken by the business. But there is also one another way in which such issues are having a profound influence on treasury. That is by encouraging treasurers to build a much deeper knowledge of tax affairs.

A new skill-set

In survey after survey, treasurers say that their role has changed significantly in the past couple of years as they get drawn into areas that were once outside their purview. Tax, as the above examples testify, is certainly one of these areas. If the experts are right, and this trend continues in the years ahead, then treasurers will surely find themselves requiring a much more detailed knowledge of tax issues than they have had until now. “I think that at the level of global treasury it is going to create the need for a whole new skill set,” says Fleming. “Now there are many treasury departments who need to arrange funding on the US capital markets – even though they have significant cash overseas – and that means they will enhance their capital market skills.”

Moreover, with so much cash building up in overseas subsidiaries, treasurers of those companies affected by US tax policy on repatriation may also need to become a little bit more adventurous in their approach to liquidity management. “That is certainly driving them to look beyond bank deposits,” says Fleming. “Since these organisations have become so cash rich, they are having to consider increasingly sophisticated investment techniques to diversify their counterparty risk and are looking more to collateralised deposits, short-dated bonds, and treasury bills that a typical corporate would not normally get involved in.”

This is not the end of the story, however. Tax rules are constantly changing and keeping on top of all the many nuances will, no doubt, require specialist expert advice. Treasurers, then, may find themselves using that hotline to the tax manager more and more in the years ahead – wherever the business operates.

A global issue

A good understanding of tax becomes particularly essential for the treasurers of businesses that operate in multiple legal jurisdictions, where tax can have an enormous impact on everything from risk management to inter-company funding decisions.

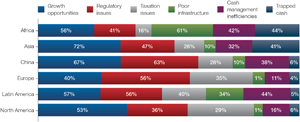

It is commonly understood that tax issues tend to become more salient for companies as they enter emerging markets. However, Treasury Today’s 2013 European Corporate Treasury Benchmarking Study reveals a slightly more nuanced picture. Although one emerging region, Latin America, was seen by the largest number of treasurers (40%) as an area where tax issues pose a great challenge, in other regions dominated by emerging economies, such as Asia, tax issues were actually seen as problematic by a fewer number (26%) than in Europe where 35% cited tax issues as a challenge.

Chart 1: How do you view the following in terms of challenges and opportunities?

Source: Treasury Today 2013 European Corporate Treasury Benchmarking Study

This demonstrates that even if your cross-border activities are limited to advanced markets, such as Europe or the US, tax issues cannot be ignored. “Particularly when you move cross-border, you have to be conscious that nearly everything you do has a tax implication,” says Neil Fleming, Director of Treasury Solutions at Capita Asset Services. “So usually it becomes a partnership relationship between tax and treasury. I don’t think a treasurer would try anything new without getting tax involved to some degree.”