Since the 1980’s, businesses have looked to adopt a Shared Service Centre (SSC) model, in order to outsource their low value, high volume financial activities with the promise of reduced operating costs and improved efficiency and control. Whilst for many this has proved a success, progressive companies are realising that a SSC can be of strategic value to the business. Here Ricky Kaura, Managing Director – Head, Corporate Sales Asia Pacific at Standard Chartered Bank, outlines how greater value can be unlocked from a SSC.

Ricky Kaura

Managing Director – Head, Corporate Sales Asia Pacific

Based in Singapore, Ricky Kaura is a regional head in the International Corporates Transaction Banking Sales organisation, encompassing responsibilities for the bank’s largest multi-national network corporate clients requiring treasury management and working capital solutions in Asia Pacific. His teams include regional hubs managing the client’s Asia Pacific Treasury Centres as well as local country resources.

Previously Kaura was with J.P. Morgan for over two decades, and had been based in the US, the UK, the Netherlands, Japan and Singapore, where he held various business and functional executive roles, including heading the firms’ Treasury and Securities Services division’s Strategy and Business Development/M&A group for Asia Pacific. Prior to this, he held leadership roles including representing one of the firm’s legal entities as President & Representative Director, as well as running the firm’s overall Treasury Services franchise in Japan and ASEAN.

It is undeniable that since the global financial crisis the role of the corporate treasury function has grown beyond its original brief to become more closely aligned with the business and operate as a true, value adding strategic partner. It could be argued however, that the evolution of the function has not only been facilitated by market realities, but also due, in part, to the fact, that for many companies the laborious low value, high volume activities such as payments and collections are now completed in a SSC – leaving the treasury free to focus on more strategic matters.

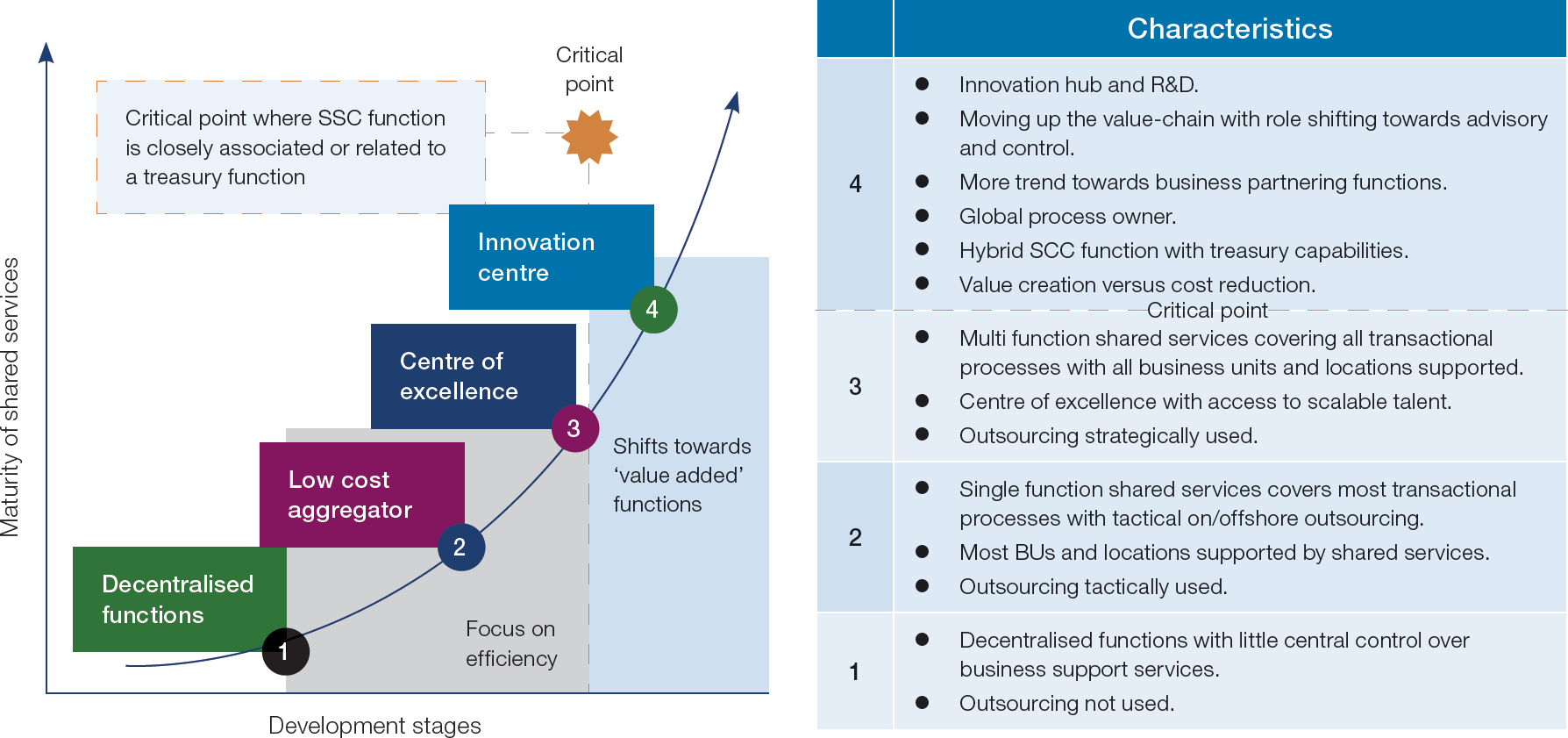

Whilst a successful strategy, there is a quiet revolution occurring in a number of progressive companies which are realising that a SSC can follow the lead taken by the treasury and offer even greater value to the business. For these companies, the SSC is no longer a low cost, process-driven function, but a centre of excellence driving process change from within and, in some cases, fundamentally changing the way the financial supply chain operates.

When carefully considered, the elevated position of the SSC makes sense. The centre has an intimate and holistic understanding of some of the most vital financial functions in the business, accounting for numerous key performance indicators. Its management team has likely developed a vast amount of knowledge around process optimisation and the various technological innovations that can enable this. And, overall, it probably has already proven that it can contribute materially to the commercial success of the enterprise – it is time to recognise this.

The SSC is increasingly a board level conversation, and its leadership team is beginning to form the ‘holy trinity’ of financial strategy with the CFO and treasurer, working together to drive change and offer value to the rest of the organisation. And for those businesses wondering where to start, it may be prudent to look at one of the most tangible and compelling areas where the ‘trinity’ can add value: improving the collections process.

A centre of efficiency

Cash collection objectives are straightforward: namely to collect payments quickly and cost-effectively, and reconcile these promptly and accurately against outstanding invoices. But, whilst a simple concept, implementation is fraught with difficulties. In particular, the diversity of collection instruments, both within each country and across regions, especially where there is a heavy reliance on cash, cheques and other local documentary instruments. This creates fragmentation and hampers efforts to standardise, accelerate and reduce the cost of collection. It also places an increased burden on the sales team in the field which has to focus its efforts on collections, rather than its core function, selling. As companies look for competitive advantage, the often underestimated burden and associated opportunity costs can be significant.

It is here that the SSC and treasury can begin to work together in order to resolve these issues and seek more efficient, ideally electronic, payment methods, particularly those that improve the predictability of collections, such as direct debits and increasingly mobile wallets where these are supported, with the latter growing at startling rates. Both functions have something to offer to this process: the treasury can evaluate the various markets, and utilise its understanding of the regulatory environment and the various challenges the sales teams are facing; the SSC can use its intimate knowledge and analytics of the collections process to evaluate how the new proposed methods of collection will impact the operation and make a recommendation based on this. In theory, and with close cooperation, the views can be married together and the best solution can be obtained, leveraging digitisation efforts and process re-engineering to drive optimal processes that facilitate reconciliation efforts.

One of India’s leading direct to home (DTH) satellite service providers conducted a project similar to this in order to solve their growing collection challenges. In brief, sales teams were spending too long on collections, and traditional advance payment models limited the ability to set up innovative arrangements with channel partners.

To resolve this, the treasury and SSC worked with Standard Chartered to implement a national ACH (automated clearing house) model with an innovative e-collection platform for same day collections, and supported the roll-out countrywide. This accelerated the collections clearing cycle from two to three days to same-day settlement, and allowed new mandates to take effect within a week, from 21 days under the previous arrangements, with automated confirmation.

In this example of how the treasury and SSC can work with a banking partner to offer greater value to the business, not only was working capital improved, but sales teams needed to spend far less time on collection activities, with far greater control over these processes.

A further area where a SSC can seek to add greater value to the overall enterprise’s collections process is through working with the treasury to push for, and implement solutions that provide rich and structured payment information. This is crucial because in today’s market environment, corporates of all sizes, and particularly those operating in emerging markets, are conscious of the risk of over-extending credit lines to customers in their sales networks. Most therefore monitor credit lines very tightly, and block new sales until collections have been posted to keep outstanding exposures under credit lines within acceptable levels. If a business does not have the ability to post collections promptly and accurately however, there can be a considerable impact on sales revenues and customer relationships.

Chart 1: SSC – stages of maturity

Source: KPMG and Standard Chartered Bank

Incoming payments therefore need to be supported with sufficient structured information to identify the payee and the invoice(s) to which the amount relates. This in turn facilitates sophisticated rule-based solutions for prompt, accurate reconciliation and posting to customer accounts. However, in Asia, obtaining rich, consistent information on incoming flows to facilitate this is challenging because of disparate payment methods and diverse payment formats across clearing systems, currencies and banks. Remittance information is therefore held in different fields within a payment instruction or advice, is of varying length and quality, and there is a risk that this data may be truncated or lost during the exchange of payment information as it passes through different clearing systems and banks.

To overcome this challenge, a growing number of companies are implementing virtual accounts, where each customer is provided with a unique account number for remitting funds, enabling them to identify individual customers. In these instances the accounts receivable teams that sit within the SSC can perform accurate, automated matching of payments to customers. This ensures that when the solution is tied with an automatic reconciliation solution that extracts files from a customer’s ERP or accounts receivable system, reconciles open invoices with information captured from clearing systems using customised matching rules, before passing the reconciled invoices back to the accounts receivable ledger to update the customer accounts.

In doing this, the SSC has the ability to become the single source of truth within the company and to facilitate a clean line of communication to the credit teams regarding who can and cannot be extended further credit, thus potentially enabling further sales, fostering greater relationships with customers and perhaps giving the business a competitive advantage.

Moreover, in this instance, aside from the strategic value that the SSC can add, it is also able to improve on its more traditional metrics as there can be a reduction of external accounts, more efficient, cost-effective processes, enhanced working capital and the ability to access working capital finance programmes for further working capital improvement.

Maximising the value of a SSC

By focusing on these two examples, the SSC, working in conjunction with the treasury department can go a long way towards adding value to the business. And today, thanks to the development of innovative technology, digitised optimal processes and solutions, this can be achieved more readily than ever before.

Building a SSC is a long-term strategic decision to support the business and deliver tangible value to the organisation. Ricky Kaura works closely with his teams who are actively involved in creating transformational approaches for clients, encompassing advanced solutions within their broad eco-systems. An area that Standard Chartered continues to lead within the Transaction Banking business, and an area of excellence for the bank. Kaura was previously with J.P. Morgan Chase & Co for over two decades, holding various business and functional executive roles, as well as being elected to the Asian Banker’s “List of Leading Practitioners”. He began his career at International Business Machines (IBM), General Electric (USA) and J.P. Morgan before joining Standard Chartered. For more insights on how Standard Chartered’s award-winning teams can help your journey, email ricky.kaura@sc.com