Embarking on an initial public offering (IPO) is a big step for any company. Obtaining a listing can bring many benefits, from fulfilling the company’s need for capital to enhancing its public image. IPOs are also sometimes used as an exit strategy for startups, as an alternative to selling the business.

Many treasurers will progress through their careers without ever being involved in an IPO. But when an IPO does take place, the treasurer may have the opportunity to play an important role in the process. “Every IPO benefits from having a primary point person,” says Adam Farlow, Partner and Head of Capital Markets, Europe, Middle East & Africa at Baker McKenzie. “The treasurer is often the perfect person for that – someone inside the company who knows where to find information and to pull together the right internal team.”

Farlow notes that IPOs are intense exercises for everyone involved, and that often – particularly late in the process – the CEO and CFO are pulled in lots of directions to do early look investor meetings, analyst presentations and the roadshow itself. “Having a treasurer who knows the business intimately, and that is available, therefore makes a huge difference,” he says.

How can the treasurer help?

Roger Lamont, Treasury Advisory Services Director at Deloitte, says that treasurers are key to an IPO for three main reasons. “They play an important role in the process, both by raising cheaper debt and using their investor relationship skills,” he explains. “Post IPO, they can also avoid shocks by managing the financial risks in the group properly.”

Raising debt.

Where debt is concerned, Lamont explains that listed businesses typically have lower leverage than privately owned or private equity-owned businesses. “As a result, the business typically needs to deleverage in preparation for an IPO, and that reduced leverage allows the company to raise cheaper debt.”

Managing investor relationships.

At the same time, Lamont says that treasurers are accustomed to managing external stakeholders such as banks and credit rating agencies – as well as bondholders if the company has capital markets debt. “These skills are obviously key while going through the IPO process, and once listed,” he says. “Effectively you already have a team within the group that has the necessary skills and experience of facing the market. The treasurer is therefore best placed to help the company through the IPO in terms of the roadshow and investor management process.”

Managing risks.

The third component of the treasurer’s role, according to Lamont, is managing financial risks such as FX and commodity risks after the IPO has taken place. He explains that once a company is listed, there is more pressure on the company to meet its announced forecast earnings. It is therefore important for treasurers to start managing the relevant risks well before the IPO occurs.

IPOs in 2017

While 2016 was a quiet year for IPOs, activity in the earlier stages of this year has been considerably higher. “Although the London IPO market is down on prior record years, 2017 has been stronger than 2016 in both volume and number, and the pipeline into 2018 feels stronger than ever,” comments Farlow.

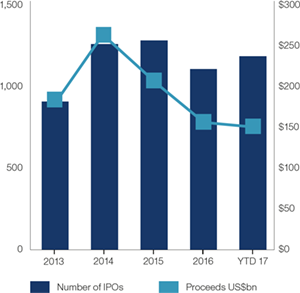

At a global level, EY’s third quarter report on the global IPO market noted that IPO volume in the first nine months of the year had already exceeded the total volume from 2016, with 1,156 deals already completed and US$126.9bn raised. Accordingly, the report notes that 2017 is on track to be the busiest year since 2007 where global IPO activity is concerned.

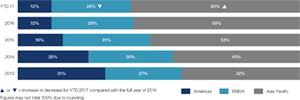

According to the report, activity was dominated by Asia Pacific, which accounted for 60% of the IPOs taking place over the first three quarters of the year. The report noted that there is a particular demand for technology IPOs in mainland China, which hosted 353 IPOs in the first nine months of the year.

The report also found that exchanges in both EMEIA and the Americas have been more active in the first nine months of this year compared with 2016, noting that activity in the US was “unusually slow” last year, with contributing factors including the uncertainties around the US election and interest rate hikes.

Making the most of the treasurer’s skills

No two deals are alike, and the treasurer’s role in an IPO will depend on a number of different factors. “It varies tremendously from deal to deal, much as the role itself varies from company to company,” says Farlow. “In some deals, we virtually never see the treasurer. In others, they are driving the process – and these invariably have smoother execution.” Farlow also points out that many early-stage companies don’t yet have treasurers, with the role sitting with the CFO or FD. “But even for those companies, the earlier they can be on-boarded, the better for the process.”

Lamont adds that the nature of the treasurer’s specific responsibilities will play a part in determining their role in an IPO. “There are businesses I’ve looked at where cash management is the only real issue the treasurer has to deal with, as there is a strong debt structure already in place,” he says. “The treasurer’s role in that type of IPO is likely to be much smaller than at a company where the treasurer’s responsibilities are larger or more complex. This might be the case when the business is being carved out of a group, or where there is a significant FX risk, or if the debt needs to be refinanced.”

It is clear that treasurers can be highly involved in an IPO process. Marianna Polykrati, Group Treasurer at Greek food company Chipita, experienced such an involvement when Edita, a joint venture between Chipita and the Berzi family, completed a dual listing on the Egyptian Exchange and the London Stock Exchange in 2015. “Myself and Chipita’s legal department were on board for a month and a half, assisting with all the documentation and assignments and working with global coordinators and bookrunners,” Polykrati explains.

With Chipita now in the early stages of exploring and evaluating a potential IPO, Polykrati is involved in several aspects of the process such as optimising the capital and debt structure and managing the logistics. However, she says that her previous experience with the Edita listing is unlikely to be directly relevant to the current process. “The Egyptian market is very unique, and we weren’t involved for the duration of the deal,” she observes. “The treasury’s role in this IPO will be much more thorough.”

Hitting the ground running

For Daniel Jefferies, a timely move to take up the role of Group Treasurer at Equiniti in May 2015 meant that he was involved from an early stage in planning for the company’s IPO later that year.

“I came to Equiniti at a reasonably early stage in their decision-making process,” he explains. “It’s not uncommon in that scenario for an organisation to evaluate a number of different tactical and strategic options – so it might be a trade sale, it might be a merger, it might be another private equity sponsor, or it might be the IPO route.”

Chart 1: IPO activity

Source: EY Global IPO trends: Q3 2017

In the case of Equiniti’s IPO, Jefferies says that he played a part in helping the company work through the different options – although the decision was ultimately driven by the owners, private equity group Advent International.

Once the decision had been made to go up the IPO route, Jefferies’ focus shifted to the debt structure of the deal. “Obviously an IPO is an equity raise,” he says. “You’re normally raising equity to allow an owner to exit or reduce a holding. But there is commonly a debt component as well – and it was the debt component where the bulk of my attention was focused.”

Chart 2: Regional share by number of IPOs

Source: EY Global IPO trends: Q3 2017

Jefferies actively chose to take on as much of the debt capital process as possible in order to free up management for the work involved in meeting investors and advisors. “On the debt side, our arrangement was fairly straightforward as we were just going for a bank deal,” he says. “We had existing high-yield notes in issuance and a fairly typical structure that you’d find with private equity ownership. Obviously the high-yield notes would be redeemed. We would retire the existing working capital facility and put in place a new debt facility.”

Equiniti secured new bank funding in the form of a term loan and revolving credit facility, which meant the company moved from a highly levered situation to a crossover credit structure. “So we weren’t in high-yield territory, but we weren’t in investment grade territory either – we were some way from that,” says Jefferies. “That’s something you can aspire to and trade into over time as you improve your bottom line.”

An IPO is not without its challenges. Farlow says that the single most important item is not to underestimate the amount of work involved in the process. “Good company counsel and underwriters can do a lot to help manage the process,” he says. “But ultimately, this is the company’s story that has to be told in the way the company wants to tell it. The day the IPO closes, life will be different and the company will have to deliver on that story that has been told to investors, so don’t let the process get in the way of allowing management to tell that story.”

Educating the market

In the case of Equiniti’s IPO, Jefferies says that one challenge was that as the company was moving from a high-yield structure to a pure bank deal, the company’s presence in the bank market was limited. “We were coming to the table with a business that wasn’t well known, and that wasn’t known in the bank market,” he explains. “We therefore had to educate people not just about the terms of the deal, but also about the terms of the credit itself – what is the business? What does it do? What drives the top line? What drives the bottom line? How are you going to do it?”

Jefferies says these factors made the IPO process more complicated than in a typical refinancing deal. “In a refinancing, even if it’s a new bank deal, you will be known and people will understand your business,” he says. “There will be information about you in the public domain, whether through S&P or Moody’s or through existing bank lending. But if you don’t have this, you have to work hard with your advisors and your new lenders to educate them on what you’re doing and how you’re going to do it.”

After the IPO

The work involved in an IPO doesn’t stop once the IPO itself has taken place – and treasurers will need to consider how the IPO will affect treasury operations in the future. Jefferies emphasises the importance of getting a deal in place that will be right for the company going forward. He notes that in any financing deal, the most difficult part is delivering on the numbers after the financing has actually been secured.

“After closing the deal in 2015, the business went away and worked very hard in 2016 and delivered on the numbers,” says Jefferies. “And in 2017 we’ve just announced a major acquisition which takes us into a new geographic territory.” He explains that it’s important to remember that rather than seeing the launch of an IPO as the end of the journey, treasurers should regard that as day one. “You then have to keep up the work to get that credit known in the wider market.”

For Equiniti, the success of the process was demonstrated when the company undertook a debt raise as part of the rights offer process. “The uptake on our deal has been very encouraging, both with existing members and new members,” says Jefferies. “I would say that’s due to the hard work the company has put in over that period.”

Investing in treasury

Treasurers may need to consider other new requirements which can arise following an IPO. “One point to note is that your treasury operations and infrastructure may require some investment post IPO, reflecting the additional requirements,” says Lamont. “You’ll potentially need additional people, processes and systems to deliver that.”

“You have to take on board that this is a unique piece of experience that may never be repeated in your career.”

Daniel Jefferies, Group Treasurer, Equiniti

For example, he points out that a smaller treasury team may need to put in place more rigorous segregation of duty controls. “Another example is that with increased scrutiny you may need stronger and better reporting, which may require additional resources or systems.”

Stepping up

Finally, Jefferies has some advice to offer other treasurers who may be embarking on the IPO process. “You have to take on board that this is a unique piece of experience that may never be repeated in your career,” he says. “You’ve got to enjoy it, as well as working hard and being prepared to engage with the relevant stakeholders. You may not always find that the asks are clearly defined, but you have to be prepared to say, ‘What can I do to facilitate this process?’ That’s how you, as a treasurer, can add value and make a difference.”

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.