Being able to calculate the cost of capital is important when you are seeking to raise funds from investors to invest in a particular project. At the heart of any cost of capital calculation is the balance between risk and reward expected by the potential investors. These investors are assumed to be risk averse. This means that the greater the risk, the greater the return they will expect on any investment that they make.

The concept of a Capital Asset Pricing Model was developed in the 1960s and provides a link between the risk and the return that investors expect. The model defines a line, described as the security market line, that can be drawn on a graph and which states that the expected return on an investment is directly proportional to that investment’s volatility. This volatility is known as beta or ß. The average ß is 1.0. Less risky investments have a ß of less than 1.0 whilst riskier investments have a ß of more than 1.0.

The relationship is defined as:

r = Rf + ß Rm – Rf

where:

r is the expected return on the investment

Rf is the return on a risk-free investment (for example, a short-term government security or cash)

Rm is the rate of return for the appropriate asset class (i.e. other investments the investor will be considering) or the average return of the market as a whole

ß is the volatility of the security with respect to the appropriate asset class or the market.

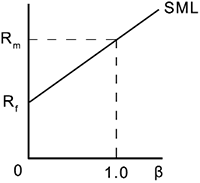

This can be shown diagrammatically:

Diagram 1: Capital asset pricing model

The line in the graph is the security market line. Note that it crosses the y-axis at the point, Rf, which represents the return on a risk-free investment. This also shows that the ß of a riskfree investment is 0. By definition, a portfolio containing all of the assets in the asset class, or the market as a whole, will have a ß of 1.0 since it will be the average.

The security market line is important as it shows the minimum return that an investor will expect on a project. Indeed, according to the model, because the ß (the slope of the line) is calculated with respect to the asset class or market as a whole, all stocks will lie on the security market line.

This can be used to calculate the expected rate of return on an investment in Company A. If we assume that the return on a government bond is 3.0%, the return in the stock market as a whole is 8% and the ß of Company A’s stock is 0.8, then we can use the formula above to calculate the expected rate of return for that stock:

r = Rf + ß Rm – Rf

r = 3.0 + 0.8 8 – 3 = 7.0 %

In other words, an investor would expect a return of 7.0% when investing in Company A.

Please enter the email that you signed up with below. If your email is

connected to a member account, we will send you a reset link.

This website uses cookies and asks for your personal data to enhance your browsing experience. We are committed to protecting your privacy and ensuring your data is handled in compliance with the General Data Protection Regulation (GDPR).