The one certainty in the current economic environment is that change is firmly on the agenda. Many may equate this with increased pressure and even risk, especially where the regulatory agenda is seen as one of tighter control. But as new developments in the European landscape unfurl, the smarter treasury operation can position itself to benefit from the very thing that others may fear.

SEPA has not had an easy ride. The Eurozone took quite some time to get used to the idea of standardised payment processes. The protracted but necessary cross-border discussions between the various stakeholders ensured that many would view it as an exercise in bureaucracy not efficiency. Indeed, now that it is a reality, some are yet to embrace the strategic and transformational benefits SEPA can bring, with focus in the main on tactical implementation and compliance. The truth for all concerned is that the hard work and expense that brought SEPA into being will remain; banks, corporates and vendors need to work together to unlock its potential. For those that do grasp ‘the art of the possible’, a world of treasury optimisation and opportunity awaits. Not least of that potential lies in the increased scope for centralisation.

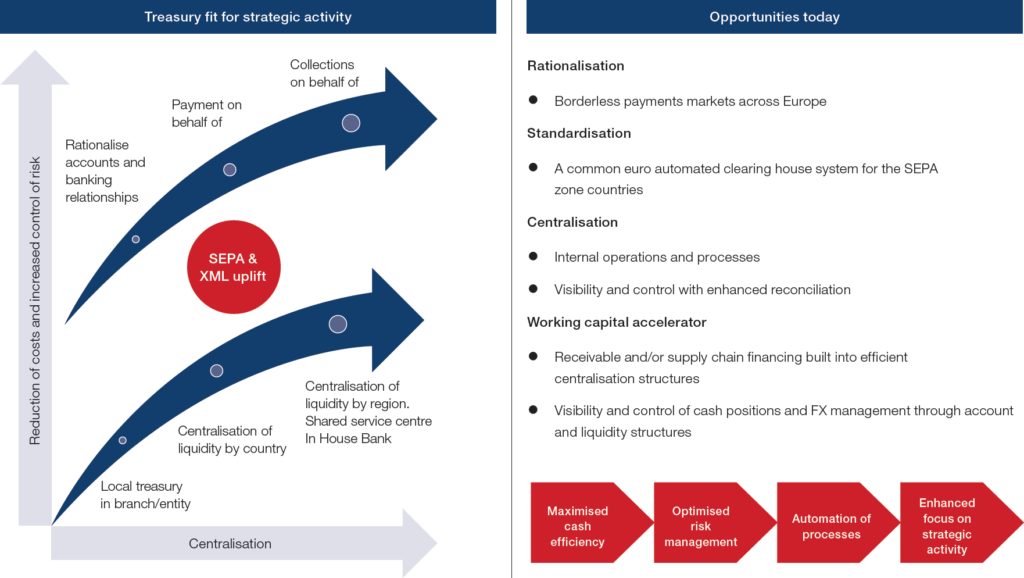

Centralise, rationalise, optimise

Companies have for some time been able to globally, regionally and domestically centralise their liquidity using a wide range of tools, such as zero-balancing and cross border sweeping. But what SEPA, and the XML data format in particular, has brought is standardisation. This gives corporates the opportunity to more readily explore the centralising, rationalising and streamlining of their accounts payable (AP) and accounts receivable (AR) processes – even combining these with their existing liquidity structure.

It is perhaps fair to say that most of the market focus, up to the point when SEPA officially went live, was on ensuring compliance and that businesses would be able to carry on with payments and collections. A lot of time and effort was expended on this and once they had made it happen, many felt they needed a break, notes Ian Blackburn, Regional Head of Commercialisation Europe, Payments and Cash Management. The value-adding SEPA benefits that were promised could wait. “I think that hiatus is now reaching an end and corporates are starting to look at how they can use that commonality.”

Many businesses are reviewing their account structures and considering what operational gains can be put in place. “The promise around SEPA is that although it is not perfect, there are further chapters to the harmonisation story – with niche products and specific payment types in certain countries – customers realise that they may not have to have so many accounts in one country,” says Michèle Zaquine, Senior Proposition Market Manager, Europe, Payments and Cash Management. “Businesses may not be able to rationalise as much as they’d like, but they might be able to make operational gains.”

In terms of rationalisation and centralisation, SEPA has in effect become a great enabler although it remains essential to assess what is the most appropriate course of action in the light of existing business models. At the highest level, a couple of different scenarios have arisen, says Blackburn. There are companies that do not necessarily have ‘bricks and mortar’ outside of their home market and SEPA has allowed them more easily to reach an increased number of markets whilst retaining their accounts in one place.

Those that do have a distributed physical presence will have had the benefit from day one of potentially lower prices for payments execution. The fact that SEPA gives a region-wide standard maximum clearing cycle of D+1 (a payment execution time at the latest by the end of the next business day) has equally allowed them not only to have certainty around the timing of their payments but has also facilitated the migration of non-urgent transactions away from the real-time gross settlement system (RTGS) to D+1, bringing cost efficiencies.

“What corporates are now looking at is a broader picture,” says Blackburn. “They are asking if they really need to have as many accounts around the region, how they can reduce their account maintenance fees, and how they might be able to rationalise accounts to simplify their liquidity management.” However, it may be a bit too soon for companies to consider placing all activities under one account, albeit theoretically possible under SEPA. Corporates are understandably focused on counterparty risk, which precludes the ‘one bank, one account’ approach. Also, for certain types of payments, most corporates would want to have accounts in-country. SEPA does not cover cheque or cash and in some markets local clearing systems – such as LCR in France or RIBA in Italy – where if a client is undertaking transactions through those mechanisms, a local account is required.

For banks, this is all part of the exercise of discussing with customers the precise nature of their payment and collection flows, and therefore whether or not certain accounts need to be maintained. This discussion may also include a technology review, considering if an existing ERP module, for example, can be enhanced to cover all operations or if the business wishes to maintain other instances of that system in-country. Zaquine comments that this has become “a much broader discussion” requiring not just an understanding of payment flows but also any issues around working capital optimisation before it is possible to use the available tools effectively.

Chart 1: SEPA, XML and treasury uplift

Payments, collections and working capital optimisation

For companies that do opt for centralisation, even if some accounts must sit outside of that model, a business can still go a long way to optimising its processes and reducing administrative costs. “But, it is easier to centralise the payments side than the collections,” says Blackburn. “Payments information is easier to track (just by extracting payment run files and sharing that information with the unit that is making the payment) whereas receivables are more challenging if the business is not able to control how the cash comes in (reconciliation is a challenge if, for example, the client does not quote references).”

There are signs that the status quo is rebalancing as the emergence of the ‘on-behalf-of’ model becomes more applicable to collections, facilitated by easier global harmonisation of invoice numbering. “Corporates are also keen to learn more about new banking techniques on the receivables side,” says Blackburn. Of note here is the ‘virtual account’ concept. Here, a corporate sets up a central account, or a smaller number of header accounts, on the receivables side. Appended to these accounts will be any number of virtual account number which are uniquely allocated to each counterparty. Each payment can only be routed via the counterparty’s unique account number and this always links back to the relevant main account. This offers a major improvement on the normal reconciliation process.

Other developments have been around data enrichment. Many corporates have realised that XML can be used beyond the SEPA landscape. Zaquine feels that it “really opens up the parameters for them having more useful data.” Combining SEPA XML data with information from outside that process has definite advantages. “By packaging a consolidated receivables management reporting tool for customers that puts all their credit receipts in one place and on one report, it gives clients that enriched data.”

By allocating this data back to their TMS or ERP system, it is possible then to start managing receipts by exception. Consolidation of information facilitates auto-reconciliation in the back office; the system is positioned to inform what has not been received and what is yet to be applied. The potential to lower overheads previously employed on sales ledger management is clear. Further, integrating data into their ERP system allows the corporate to more easily deploy that data for control, reconciliation and working capital purposes (quicker clearing cycles, reduced fees and lower overheads for allocating and matching against the sales ledger).

There is a forecasting and liquidity benefit too. If a corporate can combine the cash side with a more strategic way of looking at Days Sales Outstanding (DSO) and its payments processes, and look to reduce the cycle, this too ties in with working capital improvements. In preparing the ground for a supply chain finance or receivables finance programme that can reduce the time it takes to collect the money, there is potential for an immediate impact on cash flow. Processes such as dynamic discounting can have a similar effect.

“The centralised and rationalised treasury model is also solid ground on which to build a more robust internal governance structure,” says Blackburn. Scalability of risk and control systems becomes more challenging for companies that grow rapidly through acquisition. “But those that have taken the leap and have started to centralise will reap the benefits in terms of governance and future scalability.”

Further opportunities

By moving to a more centralised treasury model with fewer accounts, it becomes much easier to consider these improvements. “There are many components involved but as the corporate moves along the curve towards centralisation it will see more opportunities to manage its supply chain and business flows,” Zaquine notes. “SEPA and XML are just the foundations for what can become a more optimised model.” She feels that because many corporates have realised that XML is not specifically limited to payments and collections and that it is a global format that has a much wider use. Indeed, the decision by the European Central Bank (via the Euro Retail Payments Board) to press for a region-wide roll-out of an instant payments-type product (similar to Faster Payments in the UK) takes SEPA to the next level.

Specific to SEPA is the Additional Optional Services (AOS) concept. These have been permitted as a means of fine-tuning SEPA’s relevance to specific jurisdictions; extended remittance information required by Finland or France’s Change Account Identification. Some AOSs are very market-specific but if an AOS has the potential for full European reach then Zaquine believes it has the chance to be adhered to by other communities – but it will be the community operating as one, not an individual corporate or the banks, which will make this happen. For this reason, she believes that there will not be a flood of AOS requirements as SEPA gains momentum; they will arise only when the need arises and when the market pushes for it. The real question then around any AOS is its reachability. “If there is not sufficient reachability it will create market fragmentation,” she warns.

The changing face of European payments

The whole story, notes Blackburn, then moves further beyond SEPA, becoming one of the European authorities’ FinTech-driven desire to create a level playing field. Although typically consumer-driven, these technologies can quickly impact the corporate space. In addition to promoting the efficient use of existing SEPA tools (SEPA Credit Transfers and SEPA Direct Debits), concepts such as mobile and e-commerce are gaining ground as a means of enabling corporates to access information and to transact in real-time. In part, the new FinTech landscape will be facilitated by proposed revisions to the European Commission’s first Directive on Payment Services (or PSD1) which now has political agreement, at least in principal, to move ahead. Subject to further discussion and final approval by the European Parliament – possibly by September 2015 for a Q3 2017 implementation – PSD2 will mainly affect access to payment accounts, liability for process failures, transparency requirements on charges, and customer authentication measures.

One of its key aspects is the introduction of a regulatory framework ‘conducive to the emergence of new players’ known as third-party providers (TPPs). “It is something we welcome,” says Tony Richter, European Head of Regulatory and Market Delivery, Payments and Cash Management. “We recognise the need for competition; we are working with the authorities in order to make that happen.” In welcoming TPPs, Richter acknowledges that existing regulated payment service providers (PSPs) need to consider how best to work with them as market participants. The PSP view of the TPP concept is not one of out and out defensiveness; indeed there are new opportunities presented. For example, there is nothing to stop a PSP taking TPP status, potentially broadening its product proposition for customers that wish to operate through this channel. Not discounting any approach, HSBC is running an “innovation work-stream” to tap into the new opportunities coming through.

On 6th May the European Commission announced its detailed plans to deliver by the end of 2016, a Digital Single Market for Europe with 16 key initiatives grouped under three pillars:

- Better access for consumers and businesses to digital goods and services across Europe.

- Creating the right conditions and a level playing field for digital networks and innovative services to flourish.

- Maximising the growth potential of the digital economy.

“The objective is to open up competition in the European landscape to allow for digital opportunities to thrive within a clear framework and in the EU Single Market.”

Raising the game

The coverage of TPPs by PSD2 is also viewed by Richter as a positive step for the overall market in that all newcomers must match the standards to which current PSPs are required to adhere. For service users, this is an important point. “We want to work with the TPPs to develop the market, but there are some areas that we must tackle together, to make sure that other issues are not introduced,” he says. Changing the relationship of the bank with its customers to add, in some cases, a third party which will be transacting on behalf of the customer but over accounts maintained with their bank, demands that the new relationship has at least the same level of security.

With liability for process failure also tabled as part of the new Directive, Richter believes that if a customer has a query about a payment from their account, irrespective of whether they are using a TPP or not, almost inevitably they will contact their account-holding institution (the PSP) to seek redress. “This is a new aspect that will come into play in managing our payments business and we will need to build that into our overall proposition and processes,” he notes, adding that there may be a cost associated with this. With the additional focus in PSD2 on price transparency, all PSPs will need to review how they manage any such changes. As Richter says, a bank cannot just increase prices to cover an increased cost base. “We need to become more efficient in other ways to make sure we can continue to be profitable in the market.” But ultimately, this is good for the market.

Managing the broadening scope

Another area that is covered by PSD2 which needs further investigation is the so-called ‘one leg out’ transaction, the implications of which are “uncertain,” says Richter. The PSD1 was concerned only with payments made within the EEA, involving EEA currencies. PSD2 enables transactions where either the remitting or beneficiary bank is outside the EEA and using non-EEA currencies. Whilst the reach of the Directive itself clearly relates only to that portion of the transaction which takes place within the EEA, what is not yet clear is whether a payment can in practice be managed in this way, considering the need for transparency, security and all the other demands of the Directive. If, for example, a USD payment goes from Europe to the US, how can that portion that is in the EEA potentially be managed differently to that part which is being settled in the US?

Chart 2: Centralisation: a transverse project

These changes may seem primarily to impact PSPs, but as Richter notes, they will mean changes for the relationship with the customers, particularly around documentation. “We will need to review terms and conditions,” he states. “PSD1 was prepared with consumer protection in mind but also applied to corporates. Because corporates have different requirements to consumers, the option of a ‘corporate opt-out’ was included for certain provisions, negotiable between a PSP and its corporate customer. These must be reviewed again in light of PSD2.”

For all stakeholders, only when the Directive is in place will the analysts be able to consider the changes, both in terms of technology and processes. “We are beginning to get a feel for it but there is a lot more work to do,” says Richter. The fact that PSD2 is a ‘work in progress’ does not however detract from the need for discussion to start now. Corporates are advised to keep a watching brief with banks such as HSBC who are well-positioned to provide market intelligence on this topic. Richter has built a team to study the “quite substantial” regulatory developments and changes in the European payments space “so that we can better work with our clients and become a trusted advisor to them.” This creates a space where the bank can reach out to its clients “in a way that gives them an understanding of what’s happening in the industry and the impacts that may be coming their way in due course.”