Lloyds Bank is helping treasurers in regulated entities such as pension funds, property managers and stock brokers transform the challenges they face into opportunities with a unique set of products. In this Sector Profile we take a look at the bank’s offering.

Robert Hare

It is well known that corporate treasury models, strategies and challenges vary between industry sectors. Running a treasury operation in a regulated entity – such as a stockbroker or pension administrator – however entails a number of significant hurdles that other treasurers are exempt from.

Not only do treasury professionals in such entities have to think about the regulations that are affecting the wider treasury community, there are also specific regulations and requirements they must adhere to. These largely revolve around liquidity and the appropriate safeguarding of client money. Failing to comply can result in significant financial penalties – the last thing any treasurer wants to build in to their cash flow forecast.

Treasury professionals working for a regulated entity will also have a large amount of due diligence to perform when it comes to deposits. After all, such entities are not simply in charge of the company’s money, but their clients’ money too.

Indeed, regulated entities which manage client funds are coming under increasing regulatory scrutiny with regard to mitigating concentration risk and ensuring appropriate separation between client money and the firm’s money.

Lloyds Bank recognises that its corporate customers need to undertake regular due diligence on their counterparty banks,” says Robert Hare, Head of Specialist Banking, Lloyds Bank. “As such, we provide regular, detailed financial information on Lloyds Banking Group to help them to formulate and review their counterparty risk strategy. This greatly assists our customers, keeping them informed during these uncertain times.”

Hare also stresses the fact that Lloyds Banking Group has the UK’s largest retail branch network. It serves over 1m businesses and holds over £400 billion in customer deposits.

Moreover, the bank’s recently published annual results for 2011 show that it has an improved tier 1 capital ratio (10.8%), and an improved funding position – all of which has meant that wholesale funding has been reduced by £251 billion and substantial non-core assets have been reduced by £53 billion. The bank also has the lowest European sovereign debt exposure in its peer group – its total exposure to Greece, for example, stands at £500m.

“If you look at the strength of the UK’s sovereign rating and the fact that Lloyds Bank is a UK-centric bank that doesn’t have a big investment arm, we don’t expect to face the challenges down the line that some of our competitors do. Couple that with our strong core tier capital ratios and our cutting back on wholesale financing and we are well positioned to face the challenges as they arise,” says Hare.

“Nevertheless, we are also realistic and we recognise that security of funds is a concern in the market for clients wishing to place deposits,” says Hare. “Bank of Scotland and Lloyds TSB Bank Plc operate under separate banking licences as part of Lloyds Banking Group and as such any deposits held are covered separately under the Financial Services Compensation Scheme (FSCS),” he explains.

Deposits with either bank held under each banking licence therefore benefit from FSCS cover of £85,000 (£170,000 for joint accounts) per underlying client.

Expertise and intellectual capital

Away from these black and white figures and facts, Lloyds adds colour to its regulated entity proposition through its team of sector experts. The bank’s dedicated Client Banking team – that today manages a large number of accounts on behalf of clients and controls pension fund cash for their customers – was formed in the 1990s.

It was initially charged with helping stockbrokers who had to manage clients’ funds following the introduction of rolling settlement for stock exchange transactions. Over two decades later, the team continues to meet the needs of its deposit customers.

Spotlight on Client Banking

Lloyds Bank’s Client Banking team is a dedicated business area supporting the management of client funds. The bank currently manages over 200,000 client accounts and is a centre of excellence for managing clients’ funds for regulated entities.

Lloyds Bank has been voted Bank of the Year seven years running at the Finance Directors’ Excellence Awards.

A vastly experienced team works within the Client Banking department, with dedicated support for both customer relationship management and service, together with detailed sector specialisation for:

Stockbrokers.

Pension administrators.

Solicitors.

Property managers.

Insolvency practitioners.

“We are experts in regulatory requirements, particularly client money rules requiring the segregation of client funds from corporate cash. Our customer base includes approximately 60% of the members of APCIMS (Association of Private Clients Investment Managers and Stockbrokers) together with the majority of the independent Self Invested Personal Pension (SIPP) providers,” says Hare.

The team also plays a significant advisory role. For example, in October 2009, Individual Liquidity Adequacy Standards (ILAS) were introduced by the FSA to ensure firms have adequate liquidity resources so that they can meet liabilities when they fall due. Lloyds Bank was the first to engage with corporate customers and advise them of the ILAS liquidity regulations. “This engagement has paid dividends and as a result the bank has very much become the trusted advisor to each and every client on its books,” says Hare.

Reacting innovatively to turn regulatory challenges into positives is another of the team’s areas of expertise. Under ILAS, for example, banks will increasingly seek funds of a higher liquidity value (for example, notice and term deposits) and customers will look for maximum return for short-term funds – this sometimes creates conflicts with customers requiring to maintain cash liquidity in order to invest. As a result, the Client Banking team at Lloyds Bank has developed a range of new products and solutions, working closely with its customers to ensure their clients’ funds are correctly classified to benefit from the new regulations.

For example, it recently launched a 95 day notice account, which allows clients to obtain LIBOR plus on deposits. The bank also keeps close to its customer base of regulated entities to help them meet their own regulatory requirements – such as segregation of client funds (as mentioned above) and the Retail Distribution Review (RDR).

Tackling the low interest rate environment

“With interest rates so low, it is essential that investors optimise the return on their deposits,” says Hare. “The team has therefore enhanced the product offering with competitive market-led pricing across the whole product range. This range includes call accounts, current accounts, notice, fixed term (one day – five years), partial withdrawal, window term deposit and structured investment products.

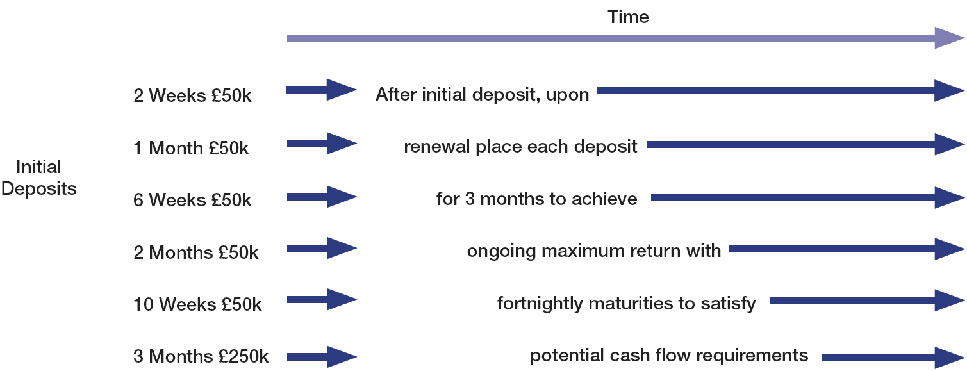

Diagram 1: Optimising deposits

According to Hare, “Lloyds Bank also has a range of specific sector products built to maximise return. These products provide simple and effective yield optimisation analytics which consider the various types of deposit a customer may hold – operational cash, core cash and strategic cash. The team can then tailor the solution to meet the individual needs of our customers.” A noteworthy example of Lloyds’ liquidity optimisation suite of tools is the Revolver Programme, which provides a staggered deposits structure to maximise return without locking the funds away for long periods of time (see diagram).

The bank has also come up with a sophisticated work-around for corporates in regulated entities to make the most of their clients’ money by having the deposits reclassified as retail rather than wholesale deposits. A substantial uplift in the liquidity value can mean that reclassified funds attract better interest rates. “It is incumbent on the banks to lead the debate in these areas – and that’s exactly what we are doing,” says Hare. “This solution is a win-win, a way of taking the challenges that regulation and legislation bring and turning them into an opportunity.”

Case study

Mattioli Woods

Alan Cowan

Section Manager

Mattioli Woods is one of the UK’s leading providers of pension consultancy and wealth management services. It employs over 250 staff in the UK, administers over 2,900 SIPP schemes and 1,400 SSAS schemes and holds over £2.8 billion of assets under advice and administration. It keeps over £65m (in over 3,000 accounts) of its own and its clients’ money with the bank.

The pension company has a long-standing relationship with Lloyds Bank, and it is a relationship that has grown stronger over the years. “The willingness of the bank to have a relationship at a high level and to engage with us and understand our requirements is really important to us,” says Cowan. “Moreover, Lloyds has a good reputation and they have a name that people know. The level of trust is excellent.”

“The company installed Lloyds Bank’s i|SITE cash management system in 2006. The straight through processing between this system and the company’s existing administration portal, a bespoke system known as MWEB, is seamless. “In the last month we have installed a feed into our admin platform that’s gone live. It builds on the efficiencies the system has given us. The i|SITE system really differentiates Lloyds Bank from other banks.”

Another plus for Mattioli Woods is the refreshing approach its banking partner has taken to its interest rate policy on deposit accounts. “The banks have always treated pension fund money as commercial and classified it as corporate cash. This means that in general, banks cannot offer our pension fund clients the rates that are on offer to retail customers. The innovative approach adopted by Lloyds Bank allows us to offer our clients better rates than some other pension providers can access.”

“As interest rates have declined, it has been a real challenge to structure our accounts such that we can continue to offer good rates for SIPP and SSAS schemes. With Lloyds Bank we have been able to negotiate our own bespoke arrangements and this allows us to pass on the benefits to our customers. The big difference is that they can price our accounts by looking at our aggregate cash balance.”

Cowan singles out Lloyds Bank’s relationship manager, Suzanne Burgoyne, for particular praise. “She is someone we can always rely on,” he says. “We like to have one point of contact – which isn’t always the case at other banks. At Lloyds Bank, we know that whatever the issue, Suzanne will take ownership and deliver a solution, often co-ordinating input from across different parts of the bank. Since the financial crisis in 2008 this kind of service has been very rare. Other banks can’t compete with that.”

i|SITE

In addition to this expertise and innovation, the bank has a sophisticated technology offering available to its customers. “i|SITE is an award winning, online cash management system providing products and services that make a difference to corporate customers and their clients,” explains Hare.

“This delivers an effective and flexible cash management service which is secure and transparent, meeting the requirements of the FSA and other regulatory bodies.” i|SITE also provides real-time cash management facilities with 24 hour secure access to accounts, account opening capability with immediate ability to transact with secure access and the ability to tailor the authorisation process. “There is also seamless integration with back office systems and the system is fully encrypted with a complete audit trail.”

The Lloyds Bank team also works closely with trade bodies such as APCIMS and AMPS (Association of Member-Directed Pension Schemes) to ensure that the bank’s technology meets the needs of their members.

“i|SITE is a well-respected and trusted system,” says Hare. “The customer managing its clients’ funds opens an account with the branch of the bank and gets an individual account. This allows them to demonstrate segregation of funds, which is important for our clients in regulated industries.”

Customer-centric approach

The Client Banking team at Lloyds Bank is a centre of excellence with expert sector knowledge, allowing it to understand its customers’ business and the challenges they face. According to Hare, the Client Banking team provides innovative deposit solutions from the bank’s extensive product range which are flexible and tailored to meet the needs of each customer. It can call upon a vast range of product partners from within the Lloyds Banking Group in areas such as transactional banking and treasury & trading to help provide customers with a full range of capabilities and solutions.

Moreover, the team supports its corporate customers throughout the economic cycle to ensure their financial health, stability and growth. It is also committed to building deep and lasting relationships with customers and supporting their ongoing contributions to the UK economy. The bank aims to achieve this by becoming its customers’ ‘trusted advisor’.

“If you’re comfortable with the trusted advisor role, you should be attuned to what is happening in the client’s business and the market. It involves giving good council to clients, generating debate, and giving your customers a heads up on innovations in the market – really, it’s all about partnerships,” says Hare.

Lloyds Bank Wholesale Banking & Markets

Lloyds Bank, part of the Wholesale division at Lloyds Banking Group, provides comprehensive expert financial services to businesses, from those with over £15m annual turnover to those with turnover in the billions. It has over 26,000 corporate clients, ranging from privately-owned firms to FTSE 100 PLCs, multinational corporations and financial institutions.

It has a network of relationship teams across the UK, as well as internationally, with the mix of local understanding and global expertise necessary to provide long-term support and advice to its customers.

Lloyds Bank offers a broad range of finance, spanning structured and asset finance, import and export trade finance; securitisation facilities and capital market funding. Its product specialists provide bespoke financial services and solutions including tailored cash management, international trade, treasury and risk management services.

Its heritage means it has an unrivalled understanding of business needs and a proven track record of supporting customers across the sectors and regions. Taking a relationship approach, it provides support to its customers throughout the economic cycle.

Contact details:

Robert Hare

Head of Specialist Banking

+44 131 658 4600

+44 7970 586 136

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Robert Hare

Robert Hare