Driving efficiencies for post-merger treasury integration

Published: Jun 2008

Global merger and acquisition1 volumes reached historic heights in 2007. Following the liquidity crunch onset, global M&A volume is likely to be lower in 2008 and the nature of M&A is expected to be different. What is certain is that cross-border activity will continue and the emerging markets will remain a dominant force. During the period 22nd December 2007 to 21st March 2008, the number of global M&A deals announced within the top industries has topped 10,000 valued at $493 billion. (Source: Reuters 31/03/08)

“Shareholders in Scottish & Newcastle have voted overwhelmingly to back the £10 billion bid for Britain’s biggest brewer by a consortium of Carlsberg and Heineken.”

Reuters 31/03/08

“Tata Motors announced it has entered into a definitive agreement with the Ford Motor Company for the purchase of Jaguar Land Rover in a $2.3 billion deal. This excludes Ford’s contribution of up to approximately $600m to the Jaguar Land Rover pension plans.”

Reuters 31/03/08

This unprecedented era of merger and acquisitions activity is being driven by three key forces:

Globalisation.

Emerging markets growth is having a major impact. In terms of global investment, 25% of every dollar invested now involves India or China. Emerging market multinationals are playing an increasingly bigger role in M&A activity – for example, Mittal of India’s acquisition of Arcelor and the takeover of IBM’s PC division by Lenovo (a Chinese computer manufacturer). The current weakness of the US dollar is also providing some attractive prey in the United States.

Investor activism.

This is becoming more and more prevalent with investors not afraid to voice an opinion and, in some cases, openly criticise management for underperformance. The recent case of activist investor Trian Fund and HJ Heinz in the US is a good example of this.

Private equity.

A recent survey reported that by 2009, up to €1 trillion2 would be at the disposal of private equity in Europe. Very few of Europe’s listed companies are now out of range of private equity bidders.

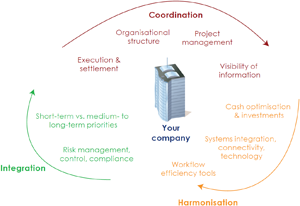

Diagram 1: M&A: Key factors for treasury to consider

Throughout this Briefng M&A refers to Mergers, Acquisitions and Spin Offs.

Figure based on €300 billion equity, €300 billion debt and €300-400 billion matched funding by 2009 – Source Deloitte Research Report – Corporate fght back: Five Disciplines to win in M&A

This Business Briefing identifies the key treasury integration factors companies should consider when acquiring or divesting companies (see diagram).

In addition, we have included two case studies to highlight some of the key elements.

A focus on settlement and execution

Before we can really focus on integrating the two organisations, it is important to settle and execute the M&A transaction. Effective execution requires outstanding end-to-end operational competence. This may have to be on a global basis where cross-border M&A is concerned. When supported by robust project planning methodology and effective use of your business partners, positive results can be achieved.

Diagram 2: Settlement and execution of the M&A transaction

As mergers and acquisitions continue to occur both domestically and cross-border, many companies need the assistance of a trusted agent to help them manage through the complexities of their transaction.

Effective planning goes a long way in mitigating the risk of things going wrong during this critical phase. Whilst the diagram on the previous page shows the key tasks as sequential, some are performed concurrently and certain companies will have considered treasury integration at the pre-deal stage. Once the execution is completed the task of treasury integration can really begin in earnest. The diagram on the right illustrates the key challenges, risks, success factors and solutions required in respect of the settlement and execution stage (for an example, please see the Philips Case Study).

The Board of Directors and shareholders will be looking for some early evidence of the benefits of their M&A decision and it is during the treasury integration phase that these first benefits can be realised. The ability to extract the maximum value from the new organisation in the shortest timeframe is absolutely vital. The treasury department is ideally placed to identify what needs to be done and, importantly, deliver some ‘quick wins’ as well as determine the longer term, more strategic treasury integration goals of the new company.

Many organisations are already re-engineering or planning to re-engineer their processes, systems, technology and working capital/cash/liquidity management practices. However, M&A activity very often provides the catalyst for such re-engineering, as the perceived benefits of an enlarged organisation accelerate the need to deliver the synergies, cost savings and other benefits which drove the M&A decision in the first place.

As an example, if bank accounts required for the new organisation are to be rationalised and cash visibility improved, debt taken on to fund the acquisition can be paid down quicker with real benefits falling straight to the bottom line. Another example of a quick win is the increase in straight-through-processing (STP), which the new company may now be able to achieve as a result of system and process synergies with early and quantifiable benefits.

Treasury integration

The diagram below identifies the main areas the treasury function needs to address as part of the treasury integration stage and, again, there will be some tactical as well as strategic decisions needed. The treasury function will work hand-in-hand with HR, procurement, technology, legal and its banking partners during this phase. The NXP Case Study opposite is an example of the real value of effective early planning and coordination to deliver an effective spin-off.

People

Process

Structure

Systems & Technology

Cultures

Visibility, control, policy, risk

In-house bank

Legacy platforms

Languages

Cost containment

Centralised vs de-centralised

ERP

Roles & responsibilities

Cash, liquidity management & investment

Shared Service Centre(s)

TMS

Locations

Bank accounts/mandates

Bank relationships

Relocations

AR/AP

Relocations

AR/AP

Training

Working capital

Contracts

Foreign exchange/hedging

Employment law

Supply chain/trade terms/suppliers

Regulatory reporting, compliance

Metrics

Performance monitoring, benchmarks

Citi GTS advises its customers on pre and post-merger treasury integration requirements. As Michael Guralnick, Global Head GTS Client Sales Management, says:

“We are able to assist on an end-to-end basis with the transaction settlement, structuring of accounts and visibility of cash by deploying highly effective tools which assist with straight through processing, reconciliation and monitoring of the flows within the merged or spun-off organisation. Our global network, operational expertise and innovative technology-based tools allow us to do this quickly and efficiently.”

Case study

Seal the deal: the critical role of settlement and execution

Royal Philips Electronics is a global leader in healthcare, lighting and consumer products based in the Netherlands.

The challenge

As part of a series of strategic acquisitions in the US healthcare sector, Philips issued a tender offer to purchase Respironics, a medical-equipment manufacturer specialising in machines that treat chronic breathing disorders in the home. The €3.6 billion ($5.2 billion) acquisition (the largest in the company’s history) was expected to progress slowly to mandatory offer status, so Philips required an agency and trust provider that could keep them fully informed of the bid’s progress and act quickly when required.

The solution

Having worked for Philips on a number of successful US acquisitions, Citi was selected as tender and exchange agent for the Respironics purchase. Throughout a series of tender extensions, Citi processed letters of transmittal from Respironics’ 25,000+ retail and institutional shareholders, the latter represented by the Depository Trust Company. Citi also provided a 24-hour hotline to inform Philips that acceptances had reached the required 90% threshold within minutes of the close of the final offer extension. This information bolstered Philips’ decision to pursue the acquisition and – once the offer became mandatory – Citi’s ability to pay out to accepting shareholders and transfer registration of shares in just two days was critical in securing a short-form merger agreement in Delaware Court of Chancery, thus avoiding further delays and costs. Having handled disbursements to accepting shareholders, Citi directed the remaining cash available to acquire outstanding minority shareholdings ($278m) to a money market fund that invested in US Treasury bonds selected by Philips. As the transaction coincided with a very substantial shift into US Treasuries by investors, Citi had to identify a second fund that met Philips’ requirements within a matter of hours to invest the cash fully while awaiting payment to the remaining shareholders. As the minority shareholdings were acquired, Citi immediately liquidated the money market fund positions to pay out shareholders and forward additional investment returns to Philips.

The verdict

Use of a flexible, responsive trusted business partner was pivotal to the successful settlement and execution of an important cross-border acquisition, such acquisition later described by Philips CEO Gerard Kleisterlee as “an excellent strategic fit.”

Case study

Mission possible: a standalone treasury in three months

NXP (formerly Philips Semiconductors) was divested in October, 2006 to a private equity consortium.

The challenge

NXP’s acquisition timetable gave its treasury team barely three months to establish fully-functioning cash and treasury processes. As Philips Semiconductors, the business had used the shared resources of Philips’ central treasury and payment factory. As NXP, it required collection and disbursement accounts in 35 countries and a centralised liquidity management structure, supported by standardised connectivity to provide visibility and control.

The solution

Citi was mandated NXP’s global cash management business on the basis of its global reach and a track record of meeting tight deadlines. Once deliverables were scoped and agreed, in July 2006, NXP and Citi appointed dedicated teams to ensure a disciplined, on-schedule implementation, tapping additional resources as necessary. Technical support was required for establishing host-to-host communication, file testing, and treasury integration with NXP’s ERP and treasury management system; close liaison with legal departments was needed to meet account opening documentation requirements.

For each country, NXP outlined its preferred account structures and worked with Citi to address any local restrictions, particularly in certain Asian jurisdictions. Using target balance accounts, domestic and cross-border cash pooling structures were established to coordinate liquidity management. Strict deadlines were set for account opening to enable NXP and Citi to conduct the necessary systems testing and to communicate account changes to business counterparties. To provide standardised connectivity and visibility, the CitiDirect® Online Banking electronic banking platform was rolled out in all countries. A centralised payments structure was implemented in which NXP’s ERP system sends payment files via Citibank® File Services for routing and in-country execution.

The result

On October 2, 2006, the deadline for completion of the spin-off process, NXP’s treasury function went live with a fully-integrated, single bank cash management solution across all regions. “Tight coordination between implementation teams was critical to achieving our goal,” said Luc de Dobbeleer, Head of Cash and Risk Management at NXP. With the backbone of the cash and treasury processes now in place, the next step was to refine and optimise the infrastructure through further automation and process standardisation.

The importance of sound project management methodology should not be underestimated in the treasury integration phase:

Diagram 3: Project management

Benefits of effective post-merger treasury integration

Some of the benefits of effective post M&A treasury integration listed below will take longer to achieve than others (see diagram below).

Diagram 4: The progression from short-term goals to longer-term strategies

Quick wins delivered sooner.

Cost savings.

Headcount efficiencies.

Process/structural and technology synergies realised quicker.

Risks mitigated.

Bank accounts rationalised.

Better decision making.

Single global treasury policy achieved.

Visibility across entire enterprise.

Control of cash and risk management globally.

Control of payables/receivables processes.

Disciplined process flow management.

Duplication of processes eliminated.

Execution and treasury integration blueprint for potential further M&A activity.

Appropriate leadership and oversight for process management across all units at centralised level.

Conclusion

M&A activity is here to stay and companies of all shapes and sizes are developing M&A strategies to deliver the growth expected by their shareholders. This is a truly global playing field and we are already witnessing a shift of focus as players from the emerging markets become investors. Successful companies are effective at M&A, but the real winners are not only extremely good at identifying the target and executing the deal – they also devote significant time and effort to the treasury integration stage of the M&A process.

After all, the prime purpose of any M&A activity is to improve what you have today. Without a coherent and effective treasury integration strategy, the benefits may take years to materialise or, worse still, not be achieved.

Citi

Citi Markets & Banking is the most complete financial partner to corporations, financial institutions, institutional investors and governments in the world. As a global leader in banking, capital markets, and transaction services, with a presence in many countries dating back more than 100 years, Citi enables clients to achieve their strategic financial objectives by providing them with cutting-edge ideas, best-in-class products and solutions, and unparalleled access to capital and liquidity.

Contact details:

Michael Guralnick

Global Head, Client Sales Management, Treasury & Trade Solutions, Global Transaction Services

EMEA Industry Head, Consumer & Heathcare and Technology, Media and Telecoms, Client Sales Management, Treasury & Trade Solutions, Global Transaction Services

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.