Trade finance plays an essential role in supporting cross-border trade. But research shows there is a sizeable gap between demand for trade finance and availability, particularly for smaller firms. What initiatives and projects are currently seeking to close up this gap – and what role can new technology play in helping to address the issue?

Trade finance plays a vital role in supporting business expansion, economic growth and financial inclusion. But it’s no secret that at a global level, there continues to be a significant gap between demand and availability.

“The market gap for trade finance is serious,” says Steven Beck, Head of Trade Finance at the Asian Development Bank (ADB). “It is large and has a major impact on our ability to create the growth and jobs that improve living standards and lift people from poverty.” He points out that the UN’s Addis Ababa Declaration on Financing for Development identified short-term trade finance as important to achieving the Sustainable Development Goals (SDGs).

“Yet ADB’s Trade Finance Gaps, Growth, and Jobs study of 2017 identified a US$1.5trn global market gap, 40% of which was in Asia,” says Beck, noting it is “no surprise” that most of the gap is concentrated in the small and medium sized company segment.

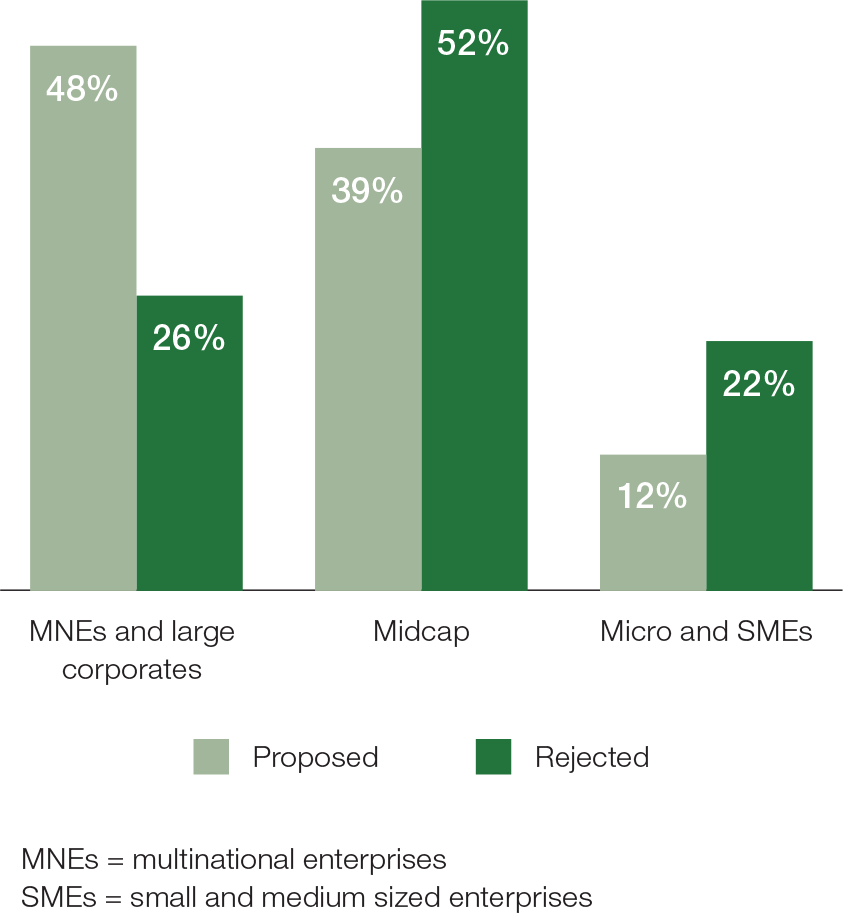

Indeed, banks reported that 74% of rejected trade finance transactions came from micro, small and medium-sized enterprises (MSMEs) and midcap firms, according to the 2017 survey. The research also found that female-owned firms “were 2.5 times more likely to have 100% of their proposals rejected by banks than male-owned firms.”

In addition, the ADB report shed some light on the reasons why banks reject trade finance applications. These included KYC concerns (29%), the need for more collateral or information (21%) and low bank profits (15%). The report noted that around 36% of the rejected trade finance transactions were considered viable.

Since the 2017 report, access to trade finance has continued to be constrained for many companies. A 2019 Global Survey by BNY Mellon found that trade finance transaction rejection rates had accelerated in the last 12 months for a third of participants. Compliance constraints and an inability to provide quality KYC constituted the leading reason for trade finance rejections, cited by 34% of respondents. A further 21% said rejections were caused by the poor credit quality of applicants/the inability for applicants to provide financial statements.

Solutions and initiatives

Finance supports growth – and it’s clear that the trade finance gap has implications for businesses, trade and economies. The ADB’s report found that 86% of firms said more trade finance would allow their businesses to grow and generate more employment. The report also noted that a 10% increase in trade finance “is associated with a 1% increase in the number of workers employed.”

Addressing the trade finance shortfall is therefore an important goal – and around the world, numerous efforts and initiatives are focused on closing the gap.

The Trade Finance Program

Beck explains that ADB’s trade finance business, the Trade Finance Program (TFP), provides guarantees and loans to banks to support trade and “helps close market gaps.” He adds that the business grew nearly 40% in both 2017 and 2018, with last year seeing 4,500 transactions valued at US$6.2bn.

“TFP focuses on more challenging markets and does not assume risk in PRC, India or Thailand,” Beck says. “Of the 21 markets where we operate, Vietnam, Bangladesh, Pakistan, Sri Lanka, Mongolia and Armenia are our most active. We’ve never had a default or loss in any of our transactions, never.”

According to Beck, this “flawless default rate” begs questions about why there is a gap. “Limited country risk appetite among the private sector in the more challenging markets is one obvious answer,” he says. “Costs and concerns about anti money-laundering (AML) and counter terrorist financing (CFT) is another.”

Chart 1: Proposed and rejected trade finance transactions (by firm size)

Source: ADB, 2017 Trade Finance Gaps, Growth and Jobs Survey

In the meantime, Beck says that ADB’s TFP is closing market gaps through loans and guarantees, which also mobilise private sector resources to these markets. “We have strong partnerships with banks and insurance,” he says. “But TFP also closes market gaps through non-transactional initiatives.”

In March, TFP convened a meeting of bank regulators, industry associations and commercial banks in Singapore “to discuss how we can drive more transparency in trade and make the due diligence process for know your client (KYC) more efficient, less onerous,” Beck notes. “There are a number of initiatives that came out of this meeting which we hope to get done by the end of the year, including an effort to standardise ‘suspicious transactions reporting’. Progress on these initiatives would help close more of the gap.”

Gathering data

While the ADB is focusing closely on this topic, other initiatives may also play a role in helping to close the gap. One is the ICC Banking Commission’s Trade Register project, which illustrates the low-risk nature of trade finance.

“Banks contribute to the ICC Trade Register, which can then demonstrate in a quantitative manner how low the default ratios are in trade finance,” explains Surath Sengupta, Head of Trade Portfolio Management and Distribution at HSBC. “It’s a big thing for banks to share data which gives more transparency and allows both banks and investors to be more comfortable financing trade,” he adds.

Making trade finance an investible asset class

At the same time, Sengupta says there is growing interest in trade finance from non-bank firms, such as funds, asset managers and insurance companies. He explains that over a long period of time, banks have created the infrastructure needed to on-board and serve this asset class – making it difficult for other parties in the financial industry to achieve something similar. “However, now they are interested in this asset class because it allows them to invest in a short-term, low-risk real economy asset,” he says. “So the question is, how can banks partner with these investors to make this asset class more investible?”

As a step in this direction, HSBC has recently announced a partnership with Allianz Global Investors which involves converting trade finance assets into a securities format. “It’s a format which is very conversant with investors, and allows them to invest in trade finance assets more easily,” says Sengupta. “And it’s also a way for us to access that liquidity. So this is a big move forward in terms of turning trade finance into an investible asset class.” He adds that there has been considerable interest from non-bank investors in this asset class and the ability to access trade finance assets.

Geoff Brady, Head of Global Trade and Supply Chain Finance at Bank of America Merrill Lynch (BofAML), agrees that there is growing interest among the investor community in “getting investment dollars into trade finance.” He cites the rise of buyer-led supply chain finance programmes – a structure “that is becoming more and more ubiquitous in the US and abroad.”

According to Brady, this type of short-term, self-liquidating funding can generate better returns than other types of credit that banks can use on behalf of a client. “Insurance companies have become interested in supply chain finance as an investment, and we’re starting to see funds showcasing supply chain finance paper,” he says.

However, Brady also notes that supply chain finance paper has a few key characteristics that make it a little more challenging for investment. “Most prominently, it’s not publicly rated and it’s not publicly traded on an exchange,” he says. “So you have to be comfortable that you understand it, and it also has to be inside your investment parameters.”

The role of technology

Technology is a particular area of interest when it comes to tackling the trade finance gap. When asked what would help address this, respondents to BNY Mellon’s survey placed enhanced technology solutions joint first with revising the regulatory environment. But questions remain about the extent to which technology can really make a difference, and whether this is happening yet.

“We’re convinced fintech can help close gaps,” says ADB’s Beck. “But there is no evidence at this point that tech is reducing gaps – only cutting banks’ operational costs.” To realise the full potential for technology in closing gaps, Beck says progress is needed on three fronts:

- Global adoption of UNCITRAL (United Nations Commission on International Trade Law) draft laws, so that digital bills of lading and other basic documents in trade have legal standing.

- Creation and adoption of global technical protocols and standards to drive inter-operability between fintech (including distributed ledger and blockchain) pilots.

- Global adoption of the Legal Entity Identifier, “an 20-digit unique globally harmonised identifier that verifies who’s who, who owns whom.”

Meanwhile, Brady cites supply chain finance as an area where technology can play a role in closing the supply chain finance gap. He explains that in the past, large buying organisations have tended to exclude their smallest suppliers from supply chain finance programmes, because the level of spend is not enough to justify the resources required to onboard them.

“Some of this gap has been filled by some of the fintechs that have come in and partnered with banks,” he says. “In some cases they are able to onboard suppliers more easily, which gives them the scale to onboard the long tail of the supplier base. We’re seeing more clients saying they want to fund the entirety of their supply chains, and not just the top 80%.” Brady adds that together with the increased investor appetite in supply chain finance, “this is helping to drive capital towards the trade finance gap.”

What about blockchain?

Blockchain and distributed ledger continues to be a hot topic in this space. Historically, trade finance has been heavily dependent on paper documentation – meaning there is plenty of room for improvement. “Trade finance is a brilliant use case for the ability to have multiple parties transacting with each other on one secure platform,” says HSBC’s Sengupta. “That will allow for more efficient end-to-end trade finance transactions – which will again help to clear one of the barriers for entry.”

In recent years, a number of international consortia have formed to explore the use of distributed ledger technology in trade finance. Notable initiatives include:

- we.trade – supports collaboration between businesses and banks in Europe; is built on the IBM Blockchain Platform using Hyperledger Fabric.

- Marco Polo – launched by TradeIX and R3; provides an open enterprise software platform for trade and working capital finance and a distributed, blockchain-powered solution.

- Voltron – built on Corda; aims to provide a digital, end-to-end documentary trade solution for banks and corporates.

The goals of these consortia include reducing operational costs, mitigating risks and expediting financing decisions. By nature, these platforms are being developed on a collaborative rather than a competitive basis.

The power of collaboration

Indeed, Sengupta notes that initiatives in this area are also helping to bring the whole community closer. “Given there is such a healthy buzz around distributed ledger and blockchain, it’s really encouraged banks to get together,” he says.

In this vein, he says that HSBC is a founding member of the Trade Finance Distribution (TFD) initiative, which incorporates banks, funds, fintechs and technology partners seeking to make trade finance more investible. Other participants include ANZ, Crédit Agricole, Deutsche Bank, ING, Lloyds Bank, Rabobank, Standard Bank, Standard Chartered and SMBC. The International Chamber of Commerce (ICC) UK and the International Trade and Forfaiting Association (IFTA) have also joined as observers.

According to a press release, the initiative “is an industry-wide drive to use technology and standardisation for the wider distribution of trade finance assets.” Aspirations of the initiative include developing “common data standards and definitions to address operational inefficiencies, transparency issues, and risks.”

Breaking down siloes

Collaboration is also at the heart of the Universal Trade Network (UTN), which was set up by the banks participating in Marco Polo project, together with TradeIX and R3, but now includes additional banks. According to the Marco Polo website, the UTN aims to “tackle the issue of separate systems of digital silos that cannot communicate or share information between each other”, allowing trading parties and financial institutions to “exchange data, and transact peer-to-peer and in real-time through an open, standard technology infrastructure powered by blockchain technology.” The UTN also aims to promote interoperability between different blockchain protocols.

“There’s some agreement that the first stop is to have standards and regulations around what we all agree to be the rules,” comments Brady. “For years we’ve had uniform customs and standards that have governed trade transactions, because they’re so international that you don’t want to be tied down to one jurisdiction. That’s part of what UTN is hoping to solve from a digital perspective – that we all agree on the rules of the road, so we can use those to plug into the same ecosystem when it comes to moving forward with the next generation of DLT or blockchain.”

The way forward

Could all these initiatives be enough to make a difference to the trade finance gap? ADB’s Beck says that while the trade finance gap is real, and has a major impact on the global community and its ability to achieve the SDGs, “What’s heartening is that the public and private sector are working together to close the gap. Certainly lots more work to be done, but there are a number of exciting gap-closing initiatives well under way that should deliver results.” He adds that the ADB plans to launch an updated market gap study in September.

It seems clear that collaboration will play a central role in addressing the shortfall. Promisingly, there is much evidence that the community is embracing a more collaborative approach. Brady points out that banks have historically moved relatively slowly towards change – and that while technology and blockchain may be the more exciting topics, the work being done to address documentation and standards is the most encouraging aspect of the efforts under way. “I’ve seen more collaboration between banks in the last four years than I have in the previous 25 years,” he says. “That’s the encouraging thing – and that’s what’s going to drive most of the change.”