When it comes to powering real-time business, the power of partnerships to drive innovative thinking matters. Victor Penna, Regional Cash Product Head, Europe & Americas, and Global Head of Structured Solutions Development, Standard Chartered, explores the demands made by new technologies and market forces on the modern treasury.

Victor Penna

Regional Cash Product Head, Europe & Americas, and Global Head of Structured Solutions Development, Standard Chartered

The rapid development of new technologies and market forces is leading corporates to disrupt their own businesses. For most, staying relevant and competing with new entrants demands action now, because the pressure to perform is mounting.

In our personal lives, digitisation is becoming all-pervasive. We expect to interact with business quickly and efficiently, often through online sites and apps to order goods or services, track delivery, raise service issues or source advice. In our role as consumers we draw upon this experience and are increasingly asking why the same type of real-time and efficient execution cannot be achieved in business to business transactions.

This expectation is also seen inside many organisations. Business managers are all too aware that their business processes are often too complex and disjointed and their own experiences as e-commerce consumers are likely to confirm this state of affairs.

With seven of the world’s biggest companies now drawn from the e-commerce sector, traditional companies have a battle on their hands. New players are perfectly positioned to find the niches and exploit them quickly, leaving slow-moving traditional companies in their wake.

Whilst many businesses are evaluating or launching online, real-time business models, the timing is now critical. The response to digital is no longer a matter of ‘if’ but ‘how’. To drive this change, many large corporates have appointed a Chief Innovation Officer to help transform their interaction with customers and suppliers through new channels.

Real-time opportunities

Many traditional companies now have a clear choice of either innovating or being disintermediated by newcomers. Taking positive action now affords an opportunity to reduce the cost of doing business through process simplification, and allows businesses to reach customers in new ways, even segments that previously may not have been accessible.

This could be as simple as launching an online business that reaches small and medium sized customers directly rather than through traditional channels. Alternatively, it could be more sophisticated, like a traditional manufacturing company incorporating Internet of Things (IoT) technology into their machinery, thus enabling their machines to call ‘back to base’ when parts and consumables need replacing or servicing is due. This provides customer convenience and automated cross-selling opportunities for the manufacturer.

Having a direct and more immediate connection with the customer changes the relationship and the nature of the interaction from reactive to proactive. The same level of interactivity can be applied right across the manufacturer’s own supply chain, bringing about a true Just-in-Time supply chain, potentially reducing or removing costly inventory holdings.

Regardless of sector, most businesses today sell to their biggest customers directly. Lower down the scale, sales tend to be through agents or distributor networks. Enabling online real-time commerce cuts out the middleman, facilitating 24/7 direct customer access to products and services by even the smallest customers. Re-engineering the way product-lines are distributed in this way makes it possible to meet business expectations – buying online and in real-time – expectations that consumers are increasingly bringing to the operation of their own businesses.

Indeed, there is strong evidence that these types of buying behaviours and expectations are working their way up from the consumer space to firstly SMEs, and then to the larger corporates. It’s a natural evolution. Progress is slower at the large-corporate end of the scale, with legacy infrastructure often presenting an obvious obstacle to selling products and services in a new way. But, by piloting new channels in select markets before rolling out enterprise-wide, even multinationals are able to meet the needs of new market dynamism.

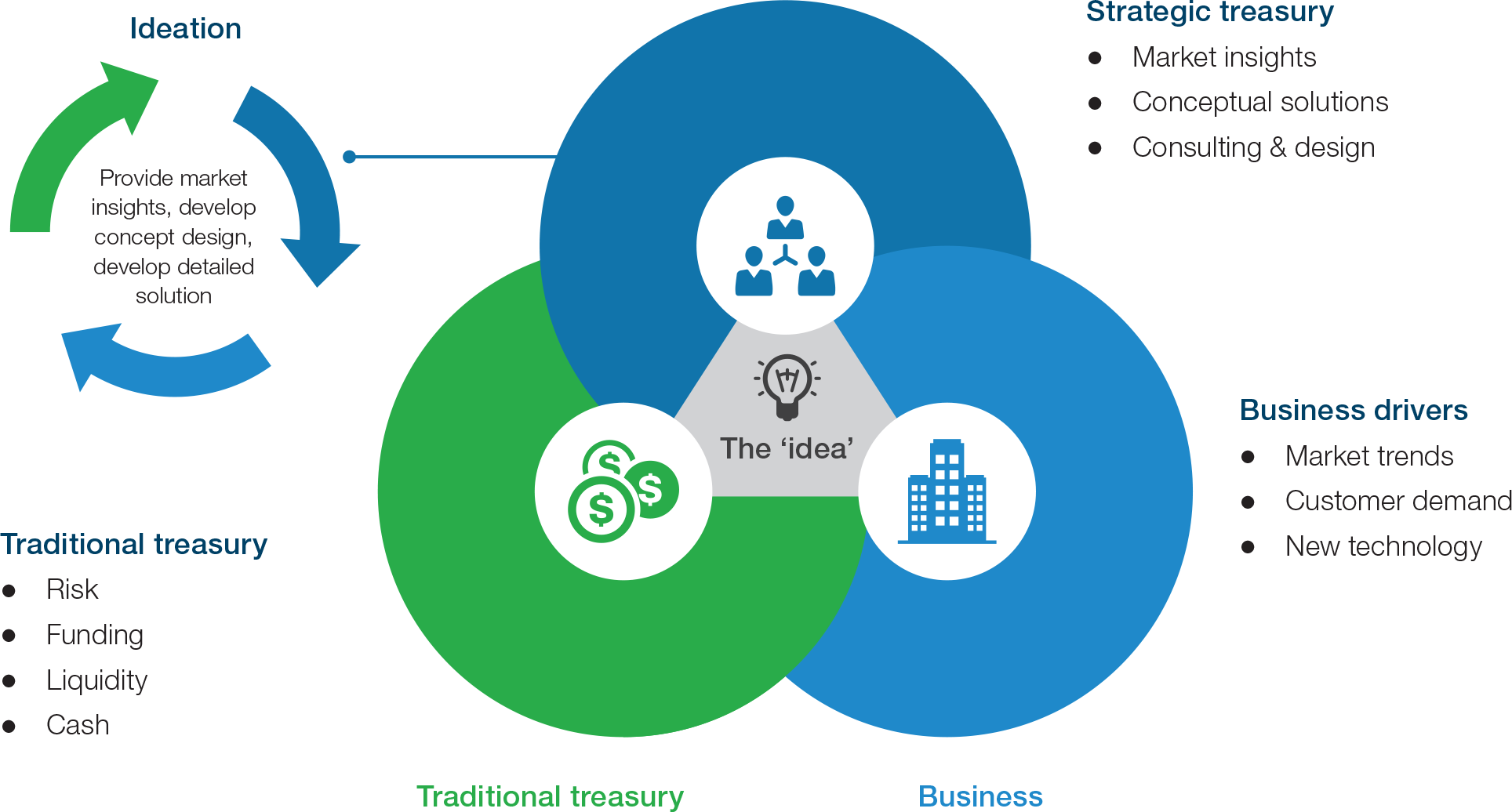

Treasurer’s role

There is a significant part to play for treasurers in the roll-out of these new online and real-time business models. The first port of call is to meet with front-line business colleagues. This should be about exploring and understanding how the business interacts with customers, and how subsequent processes flow internally.

It is vital too for treasurers to step outside of established thinking on cash management, at least as far as invoicing, collections, matching, reconciliations, payments and customer interactions are concerned. Real-time commerce will introduce a completely different toolset. Exploiting it requires re-education; treasurers must understand the applicability of new models and technologies, and firmly grasp how treasury can support and sustain its adoption.

For example, if a large corporate moves to sell online directly to SMEs, it will need payment gateways to process a wide range of payment types used by these customers. This could include instant payments, mobile money or peer to peer payment instruments commonly used by consumers and small businesses alike. Some corporates may also wish to deploy a proprietary business wallet that enables small businesses to buy from them online. Moreover, if these transactions are cross-border and a product is priced in a base currency but sold in a local currency, then real-time FX solutions that enable the dynamic pricing and settlement of these transactions between the base and local currency will also be a requirement.

In building a map of how real-time commerce can be supported, treasury becomes a critical partner for supporting a new way of doing business. Treasurers who do not become closely involved in the roll-out of real-time commerce will eventually have it imposed upon them. The risk for the business – and certainly for treasury – is that systems and processes put in place without consulting with treasury will not function optimally from a risk and liquidity point of view.

Next steps

Shifting towards a real-time operating environment is a huge undertaking. Treasurers should begin by sharing insights with their colleagues about the different models and tools available. This should be about exploring the strengths and weaknesses of the options, and how each might best serve the business.

Historically, new systems and services have been acquired through a standard RFP. Whilst this might contain a request for ‘innovation’, its delivery is typically stilted, failing to take into account the developing needs of the wider business. However, the idea of ‘co-creation’ in this space can facilitate creativity and the most beneficial outcomes for the corporate.

Prototyping and piloting concepts with technology vendors and banks, using agile development techniques, can enable a business to build solutions that meet the changing market dynamics. This process is based on a true partnership and understanding between the provider, the treasury, and the rest of the business.

Having engaged with and understood the needs of the business, treasury should start a conversation with its proposed external banking or technology partners. Asking each to meet and take part in an innovation workshop should reveal levels of awareness and understanding of new technologies and appropriate business models. The process should also expose the individual bank or vendor’s commitment, capability and readiness to helping the business reach the right outcome.

This often becomes a self-selecting exercise as the banks or vendors that really understand the issues become quickly apparent. It’s then a matter of how well teams on each side gel; co-creation is a close partnership that requires honesty, integrity and flexibility.

Of course, if the best outcome requires more than one partner, so be it. After all, thriving in the real-time world is all about making the right connections, both digital and human.

Source: Standard Chartered