As part of their core business, a large number of companies are exposed to commodity prices over which they have no control, just as they have no control over exchange rates or interest rates.

“Commodity risk matters to treasurers for the same reason that most financial risks matter – it impacts the valuation and the underlying financial performance of the business. Indeed, commodity risk can have more of an impact as the price of some commodities can be much more volatile than foreign exchange movements,” explains Kevin Lester, co-CEO at Validus Risk Management.

Impact on operations

“The overall impact of commodity prices on companies’ cost bases has increased as a general trend over the last decade or so. Commodities are now a much more noticeable line item on the financial statements compared with other constituent costs, and the proportional impact of commodity inputs has attracted attention to the importance of managing this risk effectively,” adds Lester.

If, for example, an airline has a quarter of its cost base in jet fuel, and the jet fuel market is subject to a volatility of 20%, the company’s bottom line is de facto exposed to 5% of uncertainty deriving from the cost base. And if the airline is only making a profit margin of between 1% and 3% (US airlines achieved a 2% profit margin on average during the first half of 2013, according to the trade organisation Airlines for America), this 5% exposure to the price of jet fuel could have a significant bearing on whether they make a profit or a loss.

So what can companies do to help minimise this risk? “Treasurers need to focus on the big items – the big commodity risks to their business. After looking at their exposure on a commodity-by-commodity basis, corporates should identify the risks, understand the risk dynamics, seek out the solutions that are out there, and, if necessary, address those risks. This can be a painstaking process,” says Dimitris Papathanasiou, Financial Risk Manager at Coca-Cola HBC.

Hedging your bets

Using hedging instruments to mitigate commodity risk is one such solution. The commodity markets allow both producers and consumers to hedge their commodity risks. For corporates with significant exposure to commodity prices, this is often a more effective approach than simply self-insuring using the company’s working capital.

Getting the right hedge is all about finding a derivative product which is highly correlated to the underlying price of the raw material that is required for the business. In general terms, the more liquid the market for a commodity, the easier it is to hedge. Oil, for example, is traded on many exchanges around the world and myriad derivatives are available on it. Crude oil – oil in its natural state – is traded in the form of a number of trading classifications: two of the most widely used benchmarks are Western Texas Intermediate (WTI) and Brent. Refined oil, in the form of diesel fuel, heating oil, gasoline, jet fuel and kerosene, is also widely traded and hedged.

In less liquid markets, where there are fewer derivatives available for a corporate to hedge against the commodity risk to which it is exposed, basis risk increases. Basis risk is the risk of divergence between the price of a future and the price of the underlying instrument.

As a result of the relatively limited liquidity in the commodities markets, banks often avoid presenting sophisticated hedging structures to their clients. Many corporates therefore end up using quite basic instruments in hedging their commodity risk. “The derivative instruments used are very vanilla. The majority of what corporates do to hedge their commodity risk is plain, such as swaps on whichever index they’re really exposed to,” says Andy Hartree, Head of Commodity Solutions at Lloyds Bank. For example, one-, two- or three-year diesel swaps would be included in Hartree’s definition of a plain commodity hedge. “Even the corporates with reasonably sophisticated execution strategies often use straightforward instruments,” he adds.

Instruments

Derivatives represent a promise to buy or a right to sell an underlying commodity as opposed to outright ownership. Some of the instruments available include:

Forwards

– an agreement to exchange a commodity at a specified future time and price.

Futures

– an obligation to buy a commodity if the future is not liquidated before maturity.

Options

– the choice, rather than the obligation, to buy the underlying commodity.

Swaps

– an agreement whereby exchanged cash flows are dependent on the price of the commodity.

Exchange of futures for physicals (EFP)

– an agreement whereby a futures contract is traded for the actual commodity.

Commodity derivatives are typically priced by comparing prices for the same commodity over different times, geographies and quality differentials (such as one grade of oil against another).

Thinking outside the box

In extreme cases, corporates with high exposure to commodity risk can take matters into their own hands if they can’t find suitable hedging instruments. In 2012, Delta Airlines bought its own oil refinery in an effort to address high fuel costs. Delta said the refinery in Pennsylvania, for which it paid $150m, could ultimately save the company $300m a year in fuel costs. The problem for most corporates with fuel price risk exposure is they do not have the resources to purchase their own oil refinery!

Thankfully, even with esoteric commodities for which there are no direct derivatives, hedging can often be achieved through proxy hedges. These ‘derivatives through substitution’ enable corporates to partially hedge their risk in less liquid commodities by using derivatives in more liquid commodities that bear a positive correlation to the one they want to hedge. For example, a technology company with an exposure to the price of ruthenium could hedge this risk using, for instance, platinum or palladium derivatives, if the company were confident in the correlation between the price of ruthenium and the hedged commodity.

However, hedging these rarer commodities is not always an exact science. “When you buy in certain metals which are related to – but not perfectly correlated to – the price movement in underlying metals like copper, platinum or palladium, movements in the price you’re charged by your supplier may not fully reflect price movements in the market. Hedging these less liquid commodities can definitely take away a large portion of the risk, but it’s difficult to hedge out all of the risk,” says David Madden, an analyst at financial derivatives trading firm IG Group.

Of course, if corporates hedge against the risk of commodity prices going up, and prices go down, they can potentially lose out on their hedges. In 2008, United Airlines lost $544m in a single quarter on fuel hedges. However, even though United Airlines was hit by the hedging cost, it saved money from the fuel itself being cheaper.

IFRS 9, Chapter 6

Evolutions in hedge accounting have also changed the landscape for those looking to manage their commodity risk exposure. The IFRS 9 Chapter 6 standard on hedge accounting, among other changes, allows corporates to hedge individual component inputs that were previously impossible, or at least extremely complicated, to hedge.

Under the old rules, it was not possible to individually hedge the components of non-financial items – such as the oil component of diesel fuel purchases. Under the new rules, these components can be hedged, provided the risk component is separately identifiable. Chart 1 shows some of the industries which stand to benefit from the new standard.

Chart 1: Industries impacted by changes in hedge accounting standards

Industry

Example of a possible hedging strategy under the proposed standard

Transportation and logistics

Hedging the oil component of diesel fuel purchases.

Consumer and industrial products

Hedging the aluminium/tin component of a container.

Engineering and construction

Hedging the single metal component of a metal alloy product.

Mining

Hedging the copper component of copper concentrate.

Automotive

Hedging the copper component of a copper harness.

Agricultural

Hedging the maize component of compound animal feed.

Source: PwC

As we explain in this issue’s Back to Basics article on page 41, the previous IAS 39 hedge accounting rules had been the subject of criticism for not accurately representing corporates’ risk management practices, as well as for being overly complex and difficult to apply. Many believe the new rules will free up companies that previously wanted to do hedges that were sensible from an economic perspective, but prohibitively complicated from an accounting perspective.

Jeff Wallace, Managing Partner at Greenwich Treasury Advisors LLC thinks the new rules on hedge accounting will make things better for corporates looking to hedge commodity risk. “This is a sea change. More companies should now be seriously looking at hedging some of their smaller commodity risks that they couldn’t hedge under the old rules. With hedge accounting under IFRS 9 Chapter 6 corporates can get more effective hedges – and proving that they have an effective hedge is much simpler than before,” he says. “After years and years of complaints that hedge accounting was too difficult, didn’t meet corporates’ needs or hedge the legitimate risks of the business, the IASB has made a complete turnaround. Now corporates need to take advantage of this change and have another look at their commodity risk,” he adds.

However, others fear that any positives the new standard may deliver will be outweighed by other changes in regulatory conditions that have the opposite effect. “While the evolution of hedge accounting standards has undoubtedly helped relax previously over-rigid restraints, other regulatory changes such as Dodd-Frank and EMIR could put up further barriers to commodity hedging, discouraging a considerable amount more hedging than IFRS 9 Chapter 6 could ever encourage,” says Andy Hartree, Head of Commodity Solutions at Lloyds Bank.

Quotas

An interesting quirk in the world of commodities hedging is quota management – in particular in the agricultural space. These quotas often regulate supply and price, which can make planning ahead much more predictable for corporates exposed to fluctuations in the prices of those commodities – they do not need to (and in some cases cannot) go to the financial markets for these commodities.

The EU is the world’s biggest producer of beet sugar, producing around half of the total. As part of its Single Common Market Organisation, the EU regulates its sugar market in terms of a quota, reference price and a minimum guaranteed price to growers. While the world market price of sugar has fluctuated significantly in recent years, the EU reference price has remained constant since October 2009.

Awareness

As simple as it may seem, raising awareness of the impact of commodity risk is another fantastic tool in ensuring it is appropriately managed. Some corporates already have significant resources devoted to handling their commodity risk exposure.

”Many of the big household name companies often have teams of people focused on the full range of treasury requirements. They are experts in commodity risks, not to mention the other risks they are exposed to, so they have sophisticated, well thought-out strategies and a very good idea of what’s going on in the fundamental markets. They are almost like small trading operations in their own right,” says Hartree.

However, others, particularly in the mid-market space, are less aware of how to manage their commodity risk exposure. “They might not know how the fuel price they’re actually paying is generated, how it relates to an external benchmark market from which they can then get derivatives, and what their alternatives are in terms of fixed prices from their physical suppliers,” adds Hartree.

Lester believes that treasurers sometimes give commodity risk exposure less consideration than other risks. “Even in large Fortune 500 or FTSE 100 companies, in a lot of cases there is a much higher level of expertise in other financial risks, like currency and rates than the level of expertise in commodity risk. One of the main reasons for this is that the management of that risk is a lot less clear in terms of where it gets managed. So typically if you look at currencies and interest rates and most pure financial risks, they’re clearly managed within the treasury organisation,” says Lester.

One reason for this is that these financial risks can be extracted to a greater degree from a company’s underlying business processes.

Holistic approach

It is also important to no longer view commodity risk management as an isolated discipline. Indeed, Yuri Polyakov, Head of Financial Risk Advisory at Lloyds Bank, believes commodity risk must be viewed as part of a corporate’s risk landscape as a whole. “Treasurers would also do well to take a more holistic view when looking at commodity risk. Commodity risk is not the only risk exposure they’ve got – they need to compare this with their FX and inflation risks,” he says. Think about a sterling-based company with exposure to the price of dollar-denominated fuel, for example.

“Looking at commodity risk as part of their wider risk picture, they need to play the integration game, and understand that ultimately the goal is to reduce earnings volatility,” adds Polyakov.

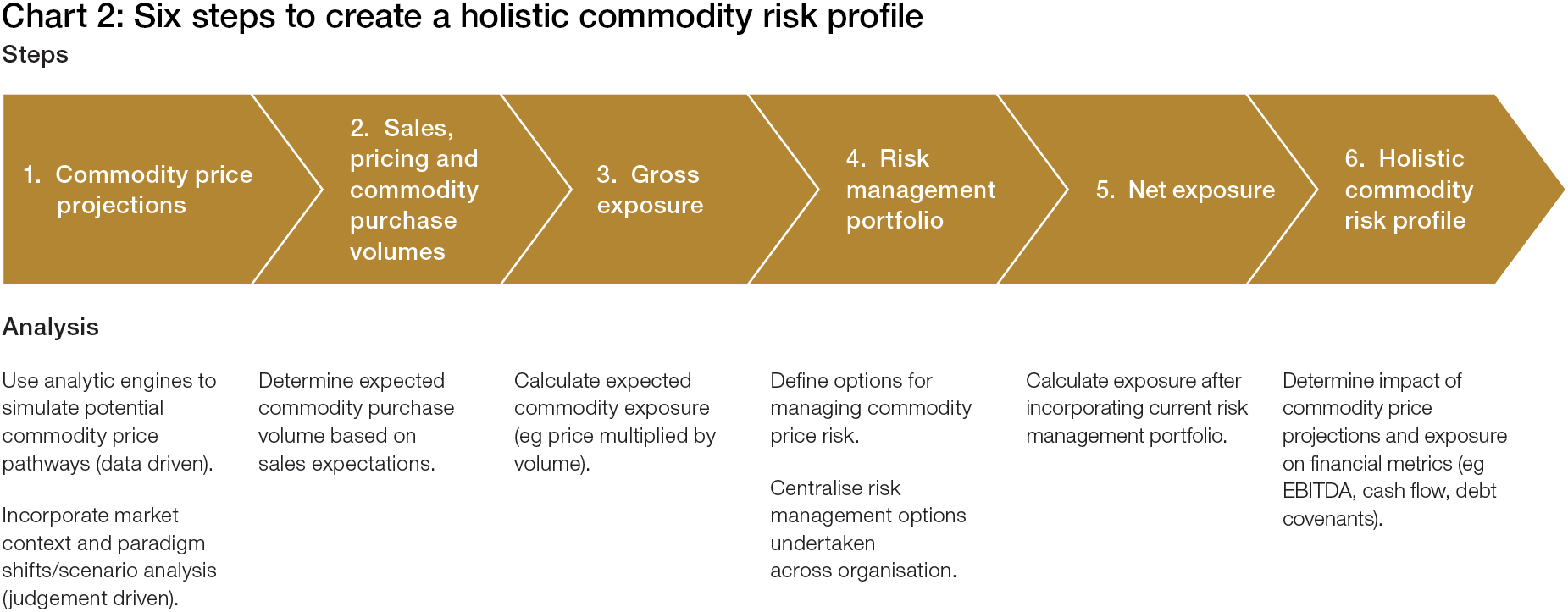

In 2012, management consulting firm Oliver Wyman set out a six-step approach to assessing commodity risk exposure, starting with commodity price projections and resulting in a holistic commodity risk profile (see Chart 2).

This should provide a good starting point for any treasurer looking to better manage their commodity exposures. But professional advice from strategic business partners, such as specialist risk advisory firms, or relationship banks, should also be sought.

Chart 2: Six steps to create a holistic commodity risk profile

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.