What burning issue is keeping corporate treasurers awake at night? Seven years ago, the health of banking partners would probably have topped the list, while two years ago many would have cited the mounting compliance burden. But ask that question to a corporate CFO or treasurer today, and many will tell you it is the geopolitical environment that they are losing the most sleep over.

Growing business concern about geopolitical risk is quite apparent in recent surveys of senior financial executives. Take the McKinsey Global Survey 2014, for example. In this study, 80% of the executives surveyed highlighted geopolitical issues as their top threat to global growth in the year ahead. Moreover, the survey appears to indicate that people expect things to get a lot worse before they get better. Only 39% of those surveyed said they anticipated global economic conditions to improve over the course of the next six months – nearly a quarter less than the 59% who said they expected improvements when asked three months prior.

Growing dangers

Financial executives are exhibiting growing concern because the geopolitical environment is becoming ever more unstable. Over the past several decades, globalisation has been the dominant force in both economics and politics. The world, we have been told, is becoming smaller with the development of a global marketplace indifferent to national borders. According to a recent report, however, we may now be entering into a new phase.

Disillusionment with globalisation is mounting, according to the “Global Risks 2015” report published by the World Economic Forum (WEF) in late 2014; and this change is driving nation states to pursue ever more protectionist, beggar-thy-neighbour policies (see box opposite). “Growing nationalism is evident around the world: in Russia, as seen in the Crimea crisis; in India with the rising popularity of nationalist politicians; and in Europe, with the rise of the far-right, nationalistic and Eurosceptic parties in a number of countries.”

That is not all. Corporates are finding themselves more exposed than ever to developments in the geopolitical sphere. The interplay between geopolitics and financial markets is one reason. When a crisis occurs, such as the outbreak of conflict in Ukraine last year, it doesn’t usually take long for financial corollaries to manifest in data rolling down the screen of the treasurer’s terminal. And when the news is particularly bad, it can mean sizeable FX losses, rating downgrades, credit difficulties or disruption to the supply chain.

Today, financial markets are more interconnected than ever before. The ripples from such incidents tend to travel further, and at much greater speed, than witnessed in the past. “Since 2011, there has been a huge increase in political risk,” says Dr Tazeeb Rajwani, Senior Lecturer in Strategic Management at Cranfield University School of Management. “There is this classic interconnection of financial markets. For example, if something happens in Hong Kong and China begins to intervene, it can have implications in another country like the UK. We are seeing these interdependencies more and more, and it’s going to continue to increase.”

Given the region’s prevailing economic troubles, for European companies in particular, global interdependencies are almost certainly set to continue strengthening even more quickly in the years ahead. Since the financial crisis and ensuing downturn we have seen export-led growth strategies become the priority for many multinationals grappling with deflationary pressures on their doorstep. But by growing the business abroad, especially in some emerging markets, companies are likely to find themselves facing heightened political threats to their operations.

This, Rajwani believes, could be a second factor explaining the growing focus on political risk. “China is obviously very attractive,” Rajwani offers as an example. “But if you are a manufacturer going into China today, for example, then you are going to have to learn to deal with varying degrees of interference from the government. This is something we have seen recently with some car manufacturers and, of course, Google. Companies who go abroad obviously need to consider these tensions.”

There is also a third factor that helps explain the heightened political risk environment: the past year’s dramatic collapse in energy prices. From the Middle East to Russia, energy price volatility is, without a shadow of a doubt, exacerbating much of the political instability seen in the world at the present time. In fact, a 2015 report by political risk specialists Aon identified heavily oil dependent countries such as Russia, Iran, Iraq, Libya and Venezuela as those facing the greatest political risks in the year ahead. The trend means that any business operating in or thinking about moving into energy export dependent economies needs to develop a greater understanding of the different policy directions in these countries and how these might, in turn, lead to significant financial consequences for their organisation.

Beyond the four T’s

The McKinsey study would suggest that the volatile geopolitical outlook highlighted by the WEF has not gone unnoticed by corporate executives. However, a growing awareness of geopolitical threats in some foreign markets does not necessarily translate into optimal risk management practices. Dr Rajwani has conducted numerous studies in recent years into market entry strategies and, in light of all the attention political risks are receiving from financial professionals, what was discovered was quite surprising to him. “What we found was that while companies are getting better at looking at political risk, many are still struggling in some ways to understand how to develop methodologies that utilise in-house knowledge or external knowledge to reduce those risks,” he explains.

Most corporate executives are well versed in the basic tenets of political risk mitigation; that is the “Four T’s” (tolerate, transfer, treat, terminate). This framework dictates that one either tolerates the risk, purchases insurance to transfer the risk and lobbies government for more favourable treatment, or avoids the risk entirely by terminating a certain activity or presence in a problematic area.

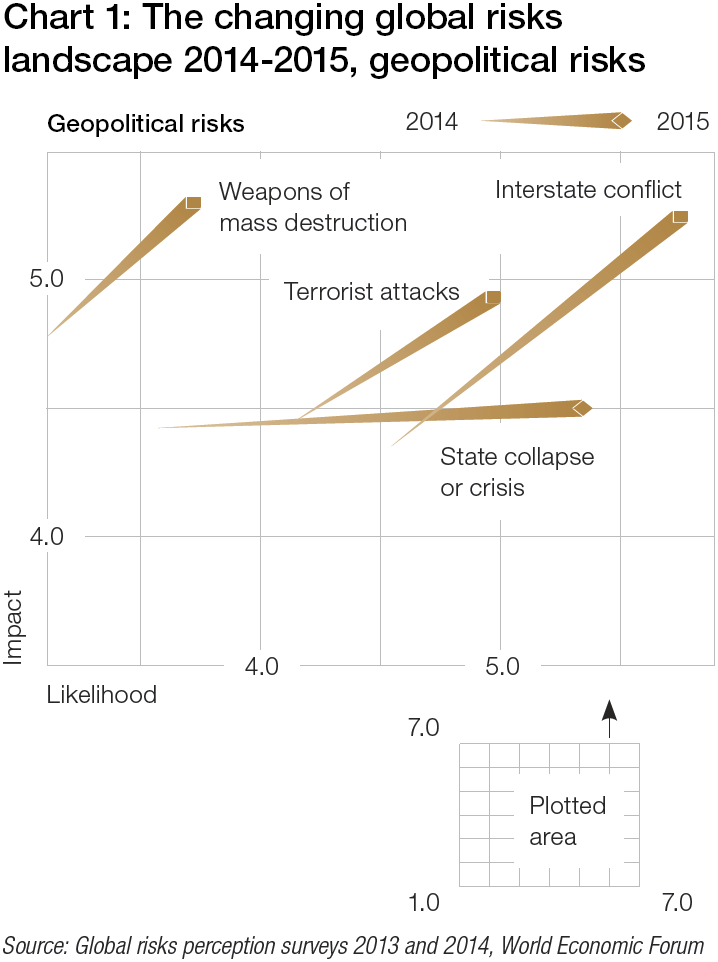

Chart 1: The changing global risks landscape 2014-2015, geopolitical risks

Source: Global risks perception surveys 2013 and 2014, World Economic Forum

Deciding on which of these steps represents the best course of action to mitigate a particular political risk a business may face is rarely straightforward, however. Take, for instance, the concept of ‘treatment’ in which companies seek to influence, through one method or another, the direction of government policy on matters that impact their interests. In some circumstances this strategy might be effective. But not in every instance. Research conducted by Rajwani on multinationals in Latin America found that in some cases, counterintuitive as it may initially sound, the best strategy is often to stay under the radar.

“If you are going into Venezuela, for example, where there is a lot of political risk, it might not be a good idea to attract attention to your firm by bargaining with officials,” he says. “There is often a high cost associated with networking and sometimes it can be counterproductive.” That is often because attempts to proactively engage with officials, explaining how much interference is going to cost the firm, the government will see it as an opportunity to extract more from the company in tax or other charges. “It’s a bit like shooting yourself in the foot,” he adds. “Sometimes the safest option is non-bargaining.”

Too little, too late

Another problem, say the experts, is that companies are exhibiting complacency before they have entered into a particular country and been confronted by a political threat. According to Henry Wilkinson, Director of the Risk Advisory, some companies have yet to fully appreciate the value of a preventative approach when it comes to political risk matters. These are companies that will turn to markets without undertaking any kind of formal risk assessment beforehand. Only then, once the company is committed and its operations are up and running, will executives begin to become conscious of the political environment. At this point, the risk manager will no doubt initiate a retroactive risk assessment – which is better than no assessment at all, of course – but by this time much of the damage may already be done.

“Companies are not always taking steps to assess political risks before they begin a particular venture,” Wilkinson explains. “This is not so much a problem for larger organisations who have teams of dedicated staff looking at these things. However, in smaller or mid-sized enterprises they might think that kind of expense is too much for them. Later on, they often wish they had looked at it sooner.”

Sven Roeleven, Vice President of enterprise platform company Software AG, agrees that corporates need to be less reactive in their management of political risks, identifying risks before they enter new jurisdictions and on an ongoing basis thereafter. In the past this would have been a very challenging task, to say the least. But the advent of sophisticated technologies, such as big data streaming analytics software, makes this task a whole lot more manageable for the modern corporate. “Instead of taking a reactive approach to risk, [companies] must take advantage of real-time data analysis tools to identify emerging and impending risks – in time to do something proactive to mitigate or avoid these risks,” says Roeleven. “Instead of acting retrospectively and executing controls at set intervals, organisations need to shift to control systems that operate continuously and that can facilitate business decisions on predictive analytics.”

Justified anxieties

At the beginning of this article, we noted an apparent increase in concern amongst financial executives around geopolitical risks. These anxieties, it would be reasonable to conclude, are nothing more than an understandable reaction to everything that has been going on in the geopolitical sphere over the past several years. On the one hand, disillusionment in globalisation and rising nationalist sentiment is unsettling both emerging and developed economies. But the interconnectivity of today’s markets, coupled with the need to look beyond domestic borders for growth opportunities means, for many multinationals, greater exposure to geopolitical turmoil.

That the financial executives of companies are showing signs that concerns are stirring and, as a result, actively demonstrating the wish to take some kind of action is undoubtedly a positive change. In the past, political risk analysis has sometimes been treated as something of an afterthought for companies when foreign expansion is on the agenda. Not any more. Now, corporate executives appear to be recognising that they need to fully understand the political environments of the markets that they want to do business in and have plans in place should events take a turn for the worse. That may not be enough to insulate the business fully from geopolitical shocks, but everybody concerned should sleep a little easier knowing those steps have been made.

In focus: political risks in Russia and CIS

It would be fair to say that the political events that unfolded in Eastern Europe last spring took nearly everybody by surprise – corporate treasurers being no exception.

The Russian economy has paid a very heavy price for its government’s aggressive foreign policies. Since President Putin began his military incursion in Ukraine, the deteriorating business environment, exacerbated by declining energy prices, has been reflected across almost every economic indicator. Sovereign, and by extension, corporate debts were downgraded to junk while Western sanctions prevent Russian corporates from raising US and European capital. And the Russian rouble, of course, entered into a tailspin, losing nearly half of its value against the dollar over the course of 2014.

Looking ahead, the Russian economy is expected to shrink by 6% in 2015 according to AXA Investment Managers. Meanwhile, although the rouble has somewhat recovered recently as a result of stabilising oil prices, analysts do not believe implied volatility (which increased by a factor of seven in 2014) is to return to levels seen prior to the annexation of Crimea anytime soon.

Treasurers preparing hedging strategies for Russia in the year ahead would be advised to keep a close eye on political developments; these will continue to be the most crucial factors in determining the risk environment in the region moving forward. But help may be required, such is the complexity of the geopolitical environment in the region at the present time. “Businesses should seek out advice from people who can very quickly grasp an unfolding situation and see order in the chaos,” says Dr Daragh McDowell, Senior Russia Analyst. This is an essential step for multinationals with an interest in the region because, whether or not the new ceasefire agreed in Minsk back in February holds (and there are serious doubts around whether it will), Dr McDowell does not foresee any let-up from Putin in the near future. “If that happens then I think Russia will retrench and look for a new target,” he says. “I don’t think this aggressive foreign policy is going away.”

But Putin has not negotiated in good faith so far and, as such, there is no reason to believe he is now. What is perhaps more likely is that Russia will attempt to use the ceasefire to sow confusion in the western ranks insisting that Ukrainian forces keep withdrawing while separatists keep advancing. If this happens we could well see another, more severe, round of sanctions imposed on Russia. Evidently the conflict in Eastern Europe – and the region’s economic woes – are still far from over.