Keeping an open mind: successful treasury operations in Africa

Published: May 2018

It’s a long game for Asian corporates moving into Africa; is it worth it? Treasury Today Asia hears some real insights and country-specific textures from treasurers already operating in the region.

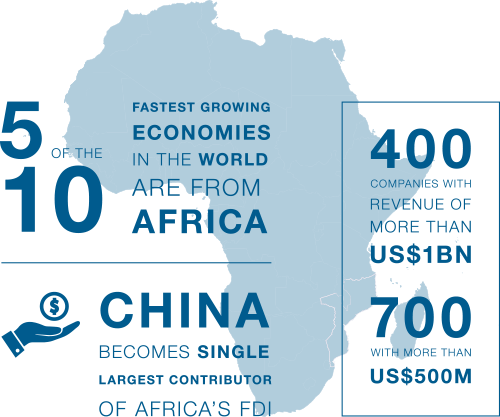

African economies are picking up. Some countries exhibit the kind of growth that seem a distant memory for European corporates, if not for Asian players. But it has not been an easy path to follow. Commodity prices have been on a roller-coaster ride, debt levels have risen, currency volatility (especially the South African rand) and the increasing costs of international capital have all burdened this continent in recent years.

There is optimism though. Investment in infrastructure is increasing – notably from China, keen to develop its Belt and Road initiative into East Africa, with Kenya a major beneficiary. In fact, Kenya is a hive of activity, having gone live with KITS (Kenya Interparticipant Transaction Switch) payments platform, offering real-time transfers.

Something similar is on its way in Zambia and Nigeria has also joined the global ‘immediate payments’ club with its NIBSS (Nigeria Interbank Settlement System). Indeed, Nigeria is moving from recession to growth and its leaders are beginning to loosen exchange controls. Meanwhile, oil exporters in sub-Saharan Africa (including Angola, Cameroon and Gabon) have seen encouraging real GDP growth of about 4%.

For corporates looking for a continental hub, it is no longer a case of South Africa or not at all. Other options have opened up, in countries such as Senegal, Kenya and Morocco, Côte d’Ivoire and Cameroon. The creation of unifying monetary zones too is adding momentum to corporate interest. The West African Economic and Monetary Union and the Central African Economic and Monetary Community are both delivering borderless banking and single payments within their zones for corporate treasuries.

Centralisation rules

But Africa is far from unified. With the markets being so different from one country to the next, the treasury decision to centralise or de-centralise is rarely clear cut, says Foluso Ayo-Olaiya, Head of Corporate and Public-Sector Product Sales, Treasury & Trade Solutions at Citi Nigeria. Speaking at a recent EuroFinance event, she said even for a major bank operating in the region, it is necessary to consider the industry, sector and appetite for concentration of each business in detail before developing what is essentially a bespoke structure.

Whilst some local entities will be precisely directed on strategy and execution from a centralised position, others are granted full power to take decisions. There is no right nor wrong way, says Ayo-Olaiya. However, where decisions are made out of headquarters in other regions, sometimes escalating through multiple layers, it is possible that swift action is not possible on financial opportunities (such as the Nigerian central bank’s snap decisions to offer ‘bargain’ FX and FX forward deals). “It is matter of deciding what aspects of the business require agile decisions, leaving them to skilled locals, then centralising key decision making and strategic thinking,” she says.

If centralisation is a natural corporate inclination, Tracy Cooper, Assistant Regional Treasurer, EMEA at Cargill says “we’re driven to it from a cost and scale perspective”. With this comes the need to be sympathetic to the needs of the regions in which the company operates. This means putting the decisions about local activities “as close as is locally possible”.

Cargill is a privately-held company operating across food and beverage, agricultural, financial risk, and industrial products in 70 countries. Its treasury is focused on centralisation, building expertise in regional hubs. It has a treasury hub in Singapore handling Asia, with another in the UK for Europe and Africa. North America has its own operations and Latin America, whilst more of a co-operation of different country operations, is effectively another treasury hub.

Cargill is currently present in seven African countries, employing around 2,000 people. Although it has a multi-business approach in most other locations, here it is usually a ‘one business-one country’ model. It operates with what it calls ‘country tags’, giving the local business in each country a direct line into centralised treasury.

Understandably, centralisation is a key topic for GE too. However, adopting this structure is dependent upon whether the market permits it, says Vasu Reddy, Treasury Leader, Sub-Saharan Africa at GE. “In Angola, it is not possible to do offshore trading or hedging so companies need to have authorised local personnel,” he notes. For GE, although even its bank approvals are done at a central level, Angola does not allow this.

FX complexity

GE itself is a combination of nine industrial businesses (covering power, water, oil and gas), and GE Capital, where the centralised treasury function resides. Its sub-Saharan Africa (SSA) operations are located in 25 countries, 19 of which are subject to cash restrictions requiring approvals for movement. A shared services centre (one has recently been established in Egypt) manages back office duties including accounts receivable, payments, bank account opening, trade execution and reporting.

In terms of its FX trading, below a certain trade-size this is standardised and automated for most GE entities. It uses an in-house platform connected to its banks through which entities request deals. However, with Angolan participation not possible, treasury must be flexible in order to discover the best possible solution that sits astride both global policy and local regulation, says Reddy.

In meeting its own FX needs, Cargill prefers multi-bank FX portals, says Cooper. Indeed, the scale and volumes of trade undertaken by the company means this technology is essential to facilitate straight through processing, from the point where the local business requests the trade, right through to execution.

“We can’t do this for many African currencies, but by streamlining and centralising the other geographies, it helps us to use our time and effort where it’s more complex,” she explains. That said, she adds that Cargill’s “technology driver” will still see the company rolling out the platform in Africa as far as it can.

Technology the saviour

The adoption of such technologies will be a key means of supporting centralisation, says Ayo-Olaiya. With banks and other financial institutions and service providers distributing real-time information, and the use of multi-banking solutions, treasurers are able to take informed decisions despite the diversity of the African trading environment, she notes.

However, unless it is mandated, the real discussion for her is always whether centralisation adds value or not. For Cooper, technology and the information exchange it allows, offers the centralised treasury the agility it needs “without feeling too far away”, so the benefits are clear.

Locally aware

Within this structure, the message is that streamlining and consistency of processes is advisable, even if the final execution with the local banks has to be manual. Not that centralising is without issue. Moving functions to a different region draws concerns, for example about local job security, lower volumes of trade and less local visibility, warns Reddy.

But then these issues have to be looked at in the context of a global business. “It’s nothing personal,” he says, “but when changes are made it’s all about cost-containment for us, operating in a much more streamlined environment in challenging times.” As such, he feels technology is going to play an increasingly important role in African treasury.

For Cooper, there is concern for local reaction too. Certain business managers in-country like to meet and talk directly with their banks, she notes. This allows them to feel in control of the relationship. Centralised intervention can, she admits, be seen as “controlling”.

But often the outcome of central intervention is that the local operation is steered in the direction of the right tools and even the right banking partner, she explains. “I think we allow them to focus on the business and take that workload off them; eventually they see the benefit.” As Reddy has said, ultimately it is about getting the best pricing and the best terms that local entities could not achieve on their own because they don’t necessarily have that insight and oversight. To a degree then an education process is necessary, Cooper describing this as an “ongoing partnership discussion”.

This constant communication and exchange of knowledge is important around a key topic such as FX because agility in responding to regulation and in accessing FX requires in-country expertise, even if the actual execution and internal processing is centralised.

Funding options

The nature of funding in Africa can prove challenging too. This has led GE to undertake occasional capital injections. For Cargill this means promoting inter-company lending as far as possible. But if a local business needs local currency, Cooper says that treasury’s ability to inter-company fund can be more limited. If there is no access to currency, treasury may not be able to execute in a way that gives the local business its funding tool other than as an FX trade. “We will try to bring in as much capital as inter-company debt as we can, versus local bank debt, and then manage that relationship,” she says. In the majority of countries in Africa, it has been possible to manage inter-company loans although in some, such as Mozambique, other methods are required.

As a means of assisting its access to currency, treasury will often extend a corporate (parental) guarantee to its banks in-country covering the local subsidiary. Success here is of course contingent upon picking the right banking partner: “one that can respect and value the guarantee” which, Cooper adds, “is not always the case with local banks”.

GE’s method, depending on the cash structure and the jurisdiction in question, is to establish centralised offshore cash pools. It will also seek to issue commercial paper in the US. As such, much of what it does around funding is centralised. If the funded entity can pay back, then an inter-company loan will be made, otherwise it will be by capital injection. “We don’t take any debt from the local banks,” states Reddy.

Banking partners

Seeing a combination of both funding models in the field, Ayo-Olaiya promotes the case for working with the right partner. “Having a bank that understands the culture of the corporate headquarters, and then knowing local personnel who can understand the dynamics and grasp the importance of flexibility, helps ensure success with the chosen structure,” she says.

Indeed, says Cooper, Cargill chooses to approach its banks on a ‘pari-passu’ basis. “With the banks knowing how we operate, it means we are able to get things done a lot quicker; we can be more agile when entering into a country.” Going to a new country and choosing a banking partner outside of the regular panel would, she notes, extend the lead time considerably.

With around 15 banking partners across Africa, and cash within those banks, GE has developed a robust risk team, says Reddy. Taking on a new partner requires extensive risk analysis on a global and country basis (considering credit ratings, balance sheets and so on). At times, banking group diversifications have necessarily been undertaken (in Angola, for example), on-boarding other banks to try to diminish risk.

The assessment of counterparty risk is a key part of GE’s global policy, this being reflected by its in-country activity. For Cooper, most of the countries Cargill operates in allows it to go with regional or global bank relationships, this making the assessment of the counterparty risk “a lot easier”.

Banking partners with muscle are closely bound with the corporate’s maintenance of relationships with local authorities too, especially with the central banks of Africa. Cargill’s team has met the authorities directly; in Zimbabwe, for example, the need for direct talk stems from the company’s status as a major exporter with deep historical roots. However, says Cooper, “normally our first port of call would be to our banks, to ask for their advice and support in going to the central banks”.

“We have a close relationship, but we don’t sleep in the same bed,” says Reddy of GE’s connection with the central banks of Africa. It too normally goes through its main banks, as a matter of policy. Indeed, he says, it is important to maintain a strong relationship with its banks, partnering with them to work with the central banks, not cutting them out of the loop in any way.

Open mind

Whatever the corporate undertaking in Africa, its sheer diversity, for Reddy, means “there is no ‘one-size fits-all’ solution”. Indeed, the only constant for GE is change, he states. “We try to be flexible, we try to gain scale, and try to maximise local resources, and we always look to our banks as partners.”

It is the same for all companies entering Africa: no matter where they are from, there will be a steep learning curve. “But only when you go through it can you figure out if what you want to do works or not,” says Reddy. “Then you can look back and know that next time you can be better prepared.”

But, he warns, even what has been learnt can quickly become obsolete. “Structures and economies change so you have to keep abreast it. This is where local expertise can help.”

For Cargill, Cooper says it is vital to keep listening to what is happening in the markets. “I think we will move towards a more service-based approach to Africa, but it really depends on what countries we will be in, and what business lines we are going to be in.” The answers to such questions, she is certain, will in every case change the dynamics of the company’s approach. Indeed, Cooper is clear that treasurers should resist holding a set view of Africa.

Top tips for establishing an African treasury

Standard solutions for Africa are rare; a case-by-case approach will usually be required.

Centralisation seems to be the preferred model.

Before entering a new market, always involve treasury in planning.

Accept and plan for trapped cash.

Seek the advice of partners in banking, legal and tax to ensure full familiarisation with local rules and expectations, especially around repatriation of funds.

Build a strong relationship with the most appropriate banks to cover both current and future needs, especially for accessing FX liquidity and keeping up regulatory changes.

Adhere closely to central bank regulations; build trust from the start.

Leverage technology to gain visibility.

Talk to those who are already there.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.