Catchy acronyms have long been used to indicate groupings of emerging markets. TICKs – incorporating Taiwan, India, China and South Korea – is one of the more recent. But what do the TICKs economies really have in common? And which other markets in the region may offer growth potential in the coming years?

The practice of using pithy acronyms to group together emerging economies with shared characteristics goes back many years. The term BRIC was coined in 2001 by Jim O’Neill, former Chief Economist of Goldman Sachs, and initially encompassed Brazil, Russia, India and China. While geographically and culturally disparate, the four countries included under the BRICs umbrella were deemed to have something important in common: their potential to grow rapidly and play an increasingly important role in the global economy in the coming years.

As well as indicating these nations’ common ground from an economics point of view, the acronym was enthusiastically adopted by fund managers – and it also led to a political alignment, with the first formal BRICs summit held in June 2009. The following year, the grouping was expanded to include South Africa, thereby turning BRICs into BRICS, although O’Neill himself argued that South Africa’s economy wasn’t large enough to warrant the inclusion. Nevertheless, cooperation between the BRICS continued and in 2014, the five states created the New Development Bank (formerly the BRICS Development Bank).

In the meantime, numerous other acronyms have been coined to describe other groupings of emerging markets, including the CIVETs (Colombia, Indonesia, Vietnam, Egypt and Turkey), MIST (Mexico, Indonesia, South Korea and Turkey) and MINT (Mexico, Indonesia, Nigeria and Turkey).

The appetite for further groupings continues, and in January 2016 the Financial Times published an article announcing ‘The Brics are dead. Long live the Ticks’. Incorporating Taiwan, India, China and South Africa, the TICKs grouping sets aside Brazil and Russia – both heavily reliant on commodity exports – in favour of technology-focused Taiwan and South Korea.

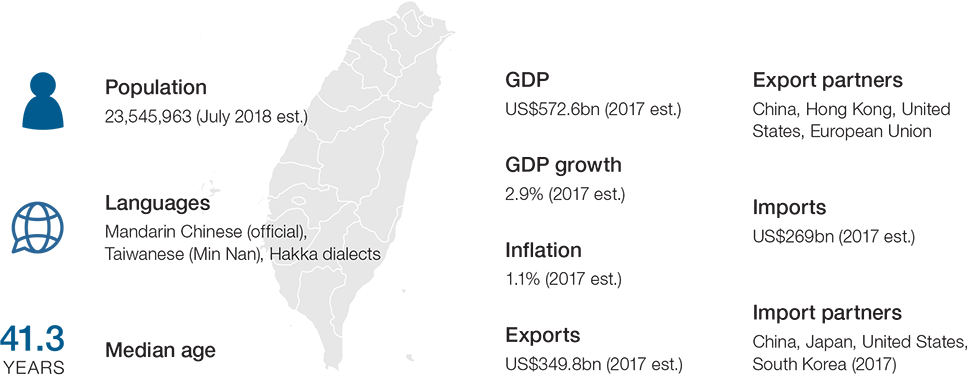

Taiwan

Source: CIA, Statista.com, Santander Trade Portal

Capturing growth

While the acronym may not have captured the level of recognition achieved by BRICS, it nevertheless continues to fulfil a role in highlighting the relevant economies’ potential.

“Over the past decade, the acronym BRICS has received a lot of attention with economies like Brazil, Russia, India, China and South Africa leading the growth in emerging markets,” says Varoon Mandhana, Senior Advisor, APAC Solutions, Treasury Services, J.P. Morgan. “With plummeting commodity prices and a slowdown in Brazil and Russia, TICKs economies came to the focus of many to capture the growth of high tech, entrepreneurial industries in emerging markets.”

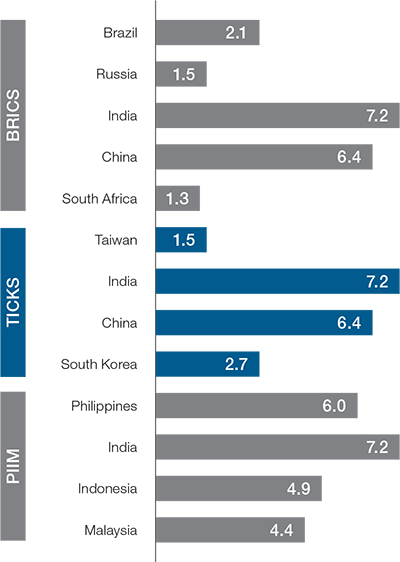

Mandhana says that while BRICS and TICKs are just industry acronyms, “to some extent they capture business and investors’ sentiment towards underlying economic growth outlook of these economies.” He adds that in addition to Asia’s giants – China and India – “we also see significant opportunities in PIMs (Philippines, Indonesia, Malaysia) where the demographics are getting better and potential growth is improving.”

Chart 1: 2019 forecasted real GDP growth (%)

Source: J.P. Morgan Global Data Watch

Aziz Parvez, head of Asia Pacific Corporate Sales, Global Transaction Services, Bank of America Merrill Lynch, explains that when the TICKs acronym was coined, the economies included “reflected the changes in global markets and in global demand shifting from trade in raw materials/commodities and energies to services, especially high technology ones.” He adds, “These changes are still relevant and we continue to see global investment channelling into high-tech industries and TICKs economies.”

According to Parvez, other macro-economic indicators also point to the relevance of these markets. “With a young population increasingly participating in e-commerce and online shopping, these economies are well placed to cater to this category of consumers,” he comments.

Comparing and contrasting the ticks

Some have complained that the groupings invented in recent years are little more than a sales gimmick, and that the countries brought together are often at significantly different stages of development. Indeed, despite enthusiasm for the various groupings, some of the resulting acronym-focused funds have had a limited shelf life: HSBC Global Asset Management closed its CIVETS fund in 2013, and Goldman closed its BRIC fund in 2015. So do the TICKs really have much in common with each other, beyond their inclusion in an appealing acronym?

On one level, the four economies are fairly diverse: the populations of China and India dwarf those of their smaller cousins, for example. But Frederic Neumann, Co-head of Asian Economics Research at HSBC, argues that Taiwan, India, China and South Korea “share as many features as divides them”. For one thing, he points out that both Taiwan and Korea are highly export dependent, with electronics playing a particularly prominent role. “That means their economies are exposed to the vagaries of the global trade and tech cycles,” he says.

Technology

Where technology is concerned, Parvez explains that South Korea and Taiwan “have been significant players in the global hardware production space in the information technology (IT) industry.” He notes that while South Korea specialises in handsets and liquid crystal display (LCD) panels, Taiwan specialises in notebook computers, motherboards, IC foundry and LCDs.

Parvez adds that China – thanks in part to Taiwanese investment – has surpassed Taiwan in hardware production to become the world’s second-largest hardware exporter. He also points out that both China and India have substantial software sectors, with India controlling the largest share of offshore software production worldwide.

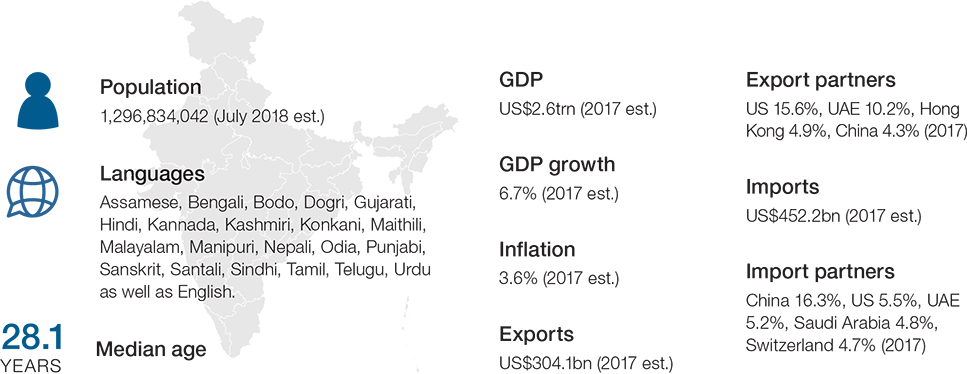

India

Source: CIA

Demand

Neumann notes that India and China are both “continental-sized” economies, as well as being relatively closed. “Here, domestic demand, whether consumption or investment, is the primary growth driver,” he says. “Both are also huge users of imported commodities, with their ups and downs having major consequences for global raw material prices. Taiwan and Korea are also highly exposed to swings in Chinese demand, with a large share of their exports heading to the Mainland.” Meanwhile, he says that India is not very exposed to China’s economy, “importing more from its large neighbour than exporting to it.”

While currently at divergent stages, Neumann says all four economies are important in their own right, with unique development stories. “Korea and Taiwan are some of the most export dependent economies in the world, sharing this feature with places like Singapore, Hong Kong, Malaysia, Thailand, and Vietnam,” he says. “India, Indonesia, and the Philippines, by contrast are currently more domestically driven.”

Other markets to watch

Emerging market acronyms are something of a moving target – so while there may still be life in the idea of TICKs economies, it is also worth asking which other markets might be included in future groupings.

Bank of America Merrill Lynch’s Parvez says that other economies that could belong in this category are Thailand and the Philippines. “Thailand is actively developing high-tech industries and the profile of Thailand economy meets the priorities of the modern global economy,” he says. “While the Philippines is in early stages of its evolution, they have the advantage of human capital. This is also an economy that is tremendous potential for growth.”

Meanwhile, Steven Beck, Head of Trade and Supply Chain Finance at Asian Development Bank (ADB), argues that Vietnam may deserve a place in the latest acronym. “Our trade finance business focuses on the more challenging markets where the private sector has most trouble operating,” he comments. “Vietnam is one of our strongest markets, along with Pakistan, Bangladesh and Sri Lanka. But Vietnam is growing and reforming at such a pace that the private sector requires fewer of ADB’s AAA-rated guarantees and funding to conduct business there.”

Increasingly, Beck says, the private sector is comfortable establishing clean lines for Vietnam’s country and counterparty risk, meaning that fewer guarantees are required from ADB as the country graduates. “This is a good thing,” he comments. “We should sort out how to add ‘V’ into ‘TICK’, because ‘V’ could become the next ‘K’ within the next generation or two.”

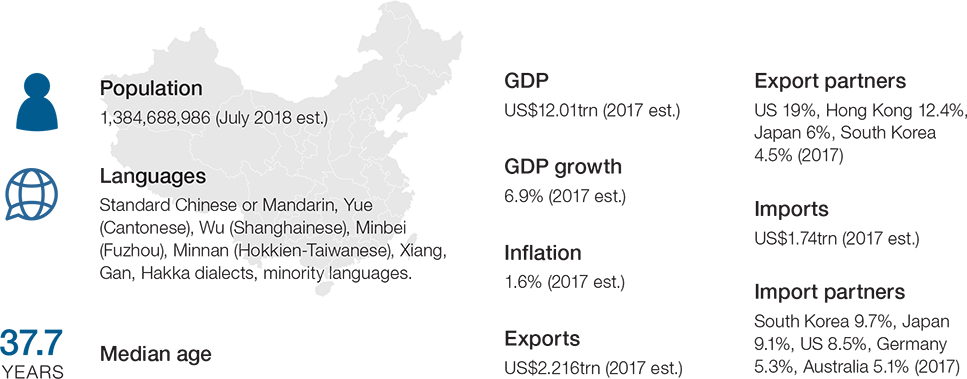

China

Source: CIA

Opportunities in emerging markets

With TICKs economies continuing to drive the region’s growth, Parvez says that a large number of global corporates are actively looking at entering these markets and setting up manufacturing units to cater to domestic demands and exports opportunities. “These countries have become key suppliers to the global market,” he says. “They not only provide the intellect and relatively cheaper labour, but also a large consumer base for the end products.”

With Asia being the fastest growing region in the world – and accounting for over 60% of global growth – it’s no surprise that MNCs are investing in APAC emerging markets as a longer-term strategy, argues Mandhana. He highlights some of the opportunities that corporates are focusing on across the region:

- China and India continue to be the key markets in which MNCs are investing, where real GDP growth is forecasted to grow at 6.4% and 7.2% respectively in 2019, compared to developed markets at 1.7% (source: J.P. Morgan Global Data Watch, 5th April 2019).

- Malaysia and Vietnam are set to benefit from the US-China trade debate, particularly in low end manufacturing of ICT (information and communications technology) products, such as intermediate components and manufacturing of consumer goods like mobile phones and laptops (source: EIU). Malaysia and also the Philippines continue to be attractive locations for MNCs looking to set up shared services with increased investments going into both captives SSCs and BPOs (source: SSON).

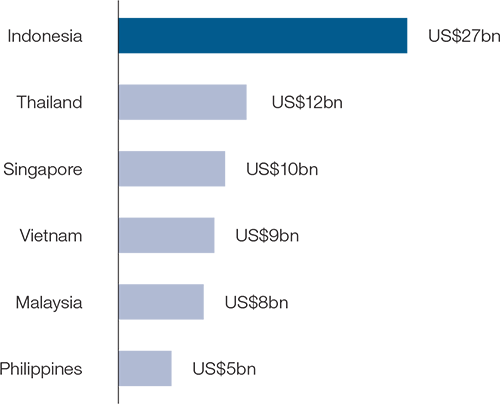

- Indonesia, the largest economy in Southeast Asia, with a large and growing digital population, is providing fertile ground for e-commerce businesses growth.

- Indonesia’s internet economy, the largest and fastest growing in the region, reached US$27bn in 2018 and is poised to grow by US$100bn by 2025 (source: Bloomberg)

Chart 2: Southeast Asia’s internet economy

Indonesia, the largest in the region, reached US$27bn in 2018

Source: Google, Temasek report

Mandhana also notes that the evolution of payments infrastructure across emerging markets, and the rise of real-time payments, “will further help to increase B2C flows by improving the customer payment experience.”

Overcoming challenges in emerging markets

While the opportunities may be considerable, Asia’s emerging markets also present significant challenges from a treasury point of view. As Mandhana points out, these include the combination of multiple currencies, currency controls, complicated tax regimes and varied legal frameworks. “Another significant issue often faced by treasurers operating in APAC is how often regulatory changes can be introduced with little advance notice, or without any formal process for widespread notification,” says Mandhana, citing the example of India’s demonetisation, which “occurred overnight”.

Parvez, likewise, emphasises the challenges presented by these economies’ regulatory controls and currency restrictions, noting that corporates need to understand the relevant regulations and remain abreast with continuous changes. “They would also need to understand that the funds could get trapped and accordingly look at the right financing structure to support their offices in these markets,” he says.

At the same time, Mandhana notes that the region’s geopolitical landscape continues to evolve, with India, South Korea, Indonesia and Thailand all set to hold elections this year – and, of course, the ongoing trade disputes between the US and China.

In this dynamic and complex regulatory and political landscape, treasurers need to keep their processes agile in order to be able to adapt to changes at short notice. “Establishing a treasury centre, or having a person based in the region in charge of treasury and tax that understands local nuances – alongside good two-way communication with head office – makes the region’s complexity more manageable,” says Mandhana. “Maintaining close relationships with regulators and banking partners is also imperative in order to gain insights into new regulatory changes as soon as they happen and be able to seek clarification on how the regulation applies in practice.”

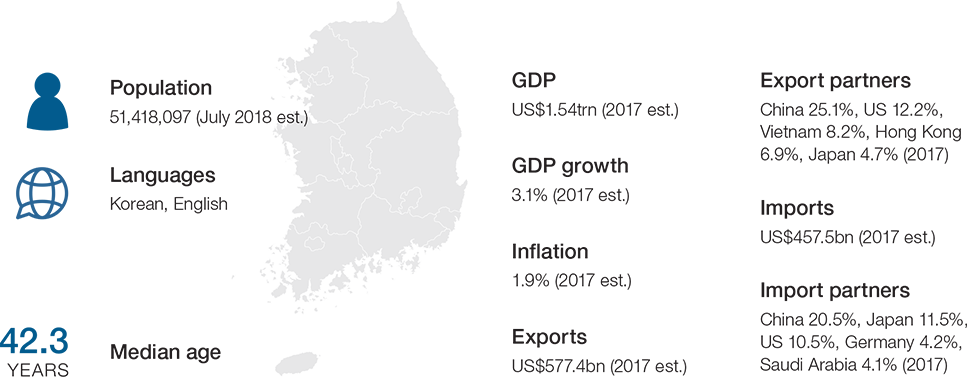

South Korea

Source: CIA