China’s emergence as a global business hub is reflected in the rapid expansion and deepening of its bond markets over the past decade. Growing ranks of investors are drawn to China’s securities markets to put their surplus liquidity to work, as an alternative to local bank deposits. Yet even as China’s debt markets join the global investment mainstream, relatively little is understood about the institution with the biggest impact on their market interest rates. Insights into the role and activities of the People’s Bank of China (PBoC) are critical to successfully navigating China’s markets, and maximizing the opportunities in this relatively new investment landscape.

Sponsor article published: 15th October 2014

Unpacking the PBoC’s Monetary Policy Toolbox

China’s emergence as a global business hub has been reflected in the rapid expansion and deepening of its bond markets over the past decade. Growing ranks of investors are drawn to China’s securities markets to put their surplus liquidity to work, as an alternative to local bank deposits. Yet even as China’s debt markets join the global investment mainstream, relatively little is understood about the institution with the biggest impact on their interest rates. Insights into the role and activities of the People’s Bank of China (PBoC or Central Bank) are critical to successfully navigating China’s markets, and maximizing the opportunities in this relatively new investment landscape.

As far as global significance is concerned, central banks do not get much more major than the PBoC. It holds the world’s largest stock of foreign currency reserves at close to USD 4 trillion, much of which is invested in US Treasuries. The PBoC is one of the leading financial authorities in the world’s second-largest economy, to which much of Asia and the broader emerging markets are highly geared. It is charged with supporting growth and maintaining financial stability as China makes a historic transition to a more sustainable economic model, and opens up to global markets. As a result, PBoC policy is not only hugely influential in a global context – it is itself evolving to address the challenges of comprehensive regime change.

As far as global significance is concerned, central banks do not get much more major than the PBoC.

A good starting point for understanding the PBoC is to consider the key differences between the PBoC and other major central banks. First, at the institutional level, the PBoC’s history as an official central bank is relatively short. Established in 1948 as the consolidation of three banks, the PBoC was not mandated to operate as a central bank until 1983. Second, unlike its Western counterparts, the PBoC is not independent from the government as it reports directly to China’s cabinet, the State Council.

Third, the PBoC is operating in an environment of much greater transition than most of its peers in the developed world. Though the PBoC’s mandate is similar, in terms of supporting the economy and preserving financial and price stability, its policy framework is evolving in the midst of accelerated urbanization, industrialization, interest rate and capital account liberalization. Unlike many major central banks, the PBoC is also responsible for operating a managed float exchange rate regime, where domestic money supply can be driven by developments in the current account. In order to manage the balance of payments, the use of capital account regulations is required to control domestic money and credit growth. Fourth and finally, the PBoC’s framework for providing emergency liquidity is less established than that of its counterparts in the developed world and relatively untested.

The last two points of distinction are significant given an unusual feature of China’s markets, whereby volatility is more pronounced at the short end. That is partly because the PBoC does not use a target rate for overnight lending in the interbank market. This also sets the PBoC apart from many central banks where an overnight target rate is the most conventional policy tool, such as the Fed funds rate in the US or the European Central Bank’s refinancing (refi) rate. The lack of an overnight target means that China’s short-term rates are driven to a greater extent by market forces, including supply and demand imbalances stemming from seasonal factors, currency flows or other drivers of liquidity. In May-June of last year, these risks were on display when a particularly strong bout of turbulence drew global attention and ultimately led the PBoC to intervene with additional liquidity.

The PBoC’s policy is evolving in ways that should reduce the risk of volatility spikes, including adding new provisions for lending to banks in times of stress, similar to the ‘discount window’ facilities offered by other major central banks. The Standing Lending Facility (SLF), introduced last year, offers one- to three-month loans to banks on request, while Pledged Supplementary Lending (PSL) can be initiated by the PBoC, offering funds over a three-month to five-year horizon.

The PBoC’s policy is evolving in ways that should reduce the risk of volatility spikes, including adding new provisions for lending to banks in times of stress, similar to the ‘discount window’ facilities offered by other major central banks.

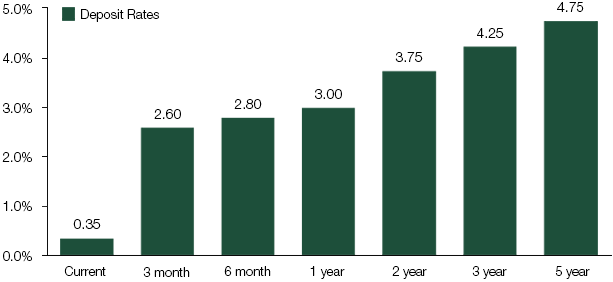

The PBoC’s current benchmark rates are set via strict regulation of interest payable on deposits of various tenors in the commercial and retail banking sector (see Figure 1). Restrictions on competition mean that banks are not permitted to add more than 10% to the regulated deposit rate, so the transmission of PBoC policy to longer-term lending rates is relatively direct.

Figure 1: Current Rates in the Regulated Deposit Market

Source: Wind, as of September 23, 2014

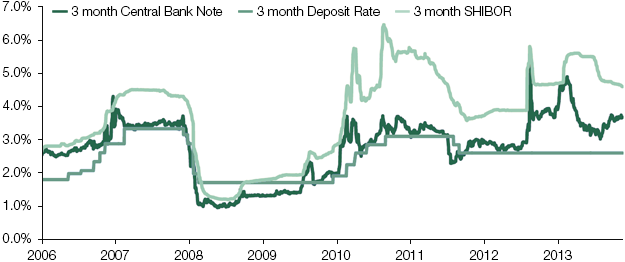

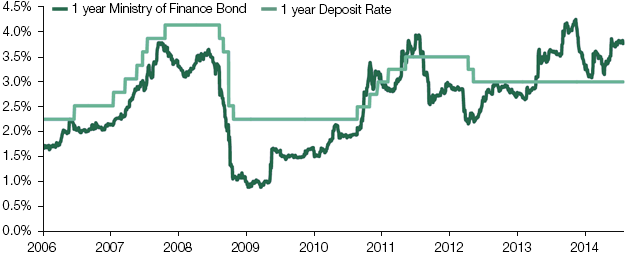

However, interest rates on regulated deposits have an inconsistent relationship with yields on similar maturity benchmark securities traded in the interbank markets. Market rates on very short-dated securities will vary substantially and average at a level that is multiple higher than deposits rates (please see China’s Markets: Interpreting Interest Rate Volatility and Figure 2). Even for tenors of three months and over, though historical experience shows that yields on securities tend to move in line with adjustments to deposit rates, prolonged and/or substantial deviations from deposit levels occur frequently (refer Figures 2 & 3).

Figures 2 & 3: Deposit Rates Versus Short-end Yields

Term rate changes can impact yields for similar maturity benchmark securities, but large movements in benchmark yields can occur without affecting term rates.

Source: Wind, as of September 22, 2014

While deposit rates are important tools for influencing the real economy, they are only part of the policy mix in terms of affecting conditions in the interbank market. In order to have a more direct impact on interest rates in the bond market, the PBoC has traditionally relied on a combination of two policy instruments: the Reserve Ratio Requirement (RRR) and Open Market Operations (OMOs).

In order to have a more direct impact on interest rates in the bond market, the PBoC has traditionally relied on a combination of two policy instruments: the Reserve Ratio Requirement (RRR) and Open Market Operations (OMOs).

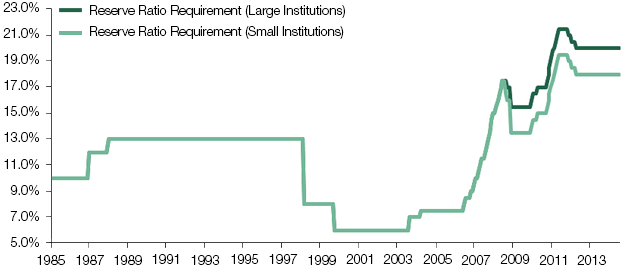

The RRR determines the share of customer deposits banks must set aside as reserves rather than lending. Adjusting this ratio allows the Central Bank to increase or reduce the supply of liquidity available for credit expansion, and generally speaking, each half-point adjustment translates to about RMB 500bn of liquidity, considering the current amount of outstanding deposits. The RRR moves in cycles, but is substantially higher today than it was 15 years ago (see Figure 4). The increase is due partly to higher levels of foreign investment throughout China’s rapid economic expansion, as periodic RRR hikes have been commonly used to reduce surplus liquidity introduced by foreign exchange flows.

Figure 4: The Reserve Ratio Requirement has Risen Partly to Absorb Increased Foreign Exchange Flows

Source: Wind, as of September 2014

The PBoC’s use of the RRR has declined somewhat in recent times, in favor of OMOs. These are common policy tools: in countries where there is an official target policy rate, OMOs are typically used to smooth market-driven variations from the target. China’s central bank uses OMOs in the absence of a target, to push market rates closer to the PBoC’s preferred levels. OMOs consist of issuing Central Bank Notes (CBNs) and increasingly, engaging in repurchase (repo) and reverse repo agreements.

As is the case with central banks globally, the PBoC’s policy has evolved substantially in recent years. The aim is twofold. The first is to establish a solid framework for liquidity provision in times of market stress via the introduction of the SLF and PSL as special lending facilities. The second and equally important aim is to broaden the Central Bank’s options for providing stimulus given the slowdown in the economy, without compromising the government’s public commitment to key reforms as it strives for more sustainable growth. As a result, the PBoC’s preferred policy measures have shifted in favor of more refined policy tools to deliver liquidity to desired parts of the banking system. Unlike its major developed market peers, which have embarked on a trend towards more frequent and more explicit communication with the market, the PBoC is less inclined to broadcast its actions and projections in advance.

As part of the trend towards subtler action, the PBoC has scaled back its use of the RRR as conventional rate adjustments tend to get widespread media attention. Policymakers have recently adopted more targeted RRR policy, focused on small or rural banks that meet certain criteria in terms of the amount of outstanding loans and/or their location. The Bank has also expanded its use of OMOs, with the introduction of Short-term Liquidity Operations (SLOs) to transact in the repo and reverse repo markets as needed at terms of up to seven days.

As part of the trend towards subtler action, the PBoC has scaled back its use of the RRR, as conventional rate adjustments tend to get widespread media attention.

Figure 5: Select PBoC Monetary Policy Tools

Tenor

Form

Interest Rate

Open Market Operations (Conducted regularly)

Repo: 7, 14, 28, 91 days

Central Bank Notes: 3 months/1 or 3 years

Repo/reverse repo/bills

Auction

Short-term Liquidity Operations (Ad-hoc basis)

Maximum 7 days

Repo and reverse repo

Auction

Standing Lending Facility (Ad-hoc basis requested by banks)

1 month to 3 months

Collateralized loan and credit borrowing

Set by the PBoC

Pledged Supplementary Lending (Ad-hoc basis initiated by the PBoC)

3 months to 5 years

Collateralized loan

Unclear (negotiable)

Source: Goldman Sachs Asset Management, as of October 8, 2014

Looking ahead, these new instruments are likely to play a larger role in PBoC policy as the Central Bank hones its toolkit for a maturing market. In the medium term, further easing is likely as economic activity has slowed again and policymakers are keen to defend the official 7.5% growth target. Targeted easing rather than overall rate and RRR cuts is more likely for the remainder of this year, given the PBoC’s recent RMB 500bn injection and the government’s preference for less obtrusive measures. The Central Bank may instead provide further liquidity via targeted cuts, and/or deploy its newer facilities for lending directly to specific banks.

These are all critical elements of the PBoC’s policy response to the historic transitions under way in China’s economy and markets. Given the widespread uncertainty surrounding the range and impact of various policy tools, investors stand to benefit from an understanding of the PBoC’s function. This insight should also better equip investors to navigate the risks and opportunities that may arise from further turbulence at this point in the evolution of China’s markets.

For more information on Goldman Sachs Global Liquidity Management, please contact:

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material is not financial research and was not prepared by Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of GIR or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and GSAM has no obligation to provide any updates..

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by GSAM to buy, sell, or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as investment advice.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

The website links provided are for your convenience only and are not an endorsement or recommendation by GSAM of any of these websites or the products or services offered. GSAM is not responsible for the accuracy and validity of the content of these websites.

United Kingdom and European Economic Area (EEA): In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Asia Pacific: Please note that neither Goldman Sachs Asset Management International nor any other entities involved in the Goldman Sachs Asset Management (GSAM) business maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, Malaysia, and India. This material has been issued for use in or from Hong Kong by Goldman Sachs (Asia) L.L.C, in or from Singapore by Goldman Sachs (Singapore) Pte. (Company Number:198602165W), in or from Malaysia by Goldman Sachs(Malaysia) Sdn Berhad (880767W) and in or from India by Goldman Sachs Asset Management (India) Private Limited (GSAM India).

Australia: This material is distributed in Australia and New Zealand by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (’GSAMA’) and is intended for viewing only by wholesale clients in Australia for the purposes of section 761G of the Corporations Act 2001 (Cth) and to clients who either fall within any or all of the categories of investors set out in section 3(2) or sub-section 5(2CC) of the Securities Act 1978 (NZ) and fall within the definition of a wholesale client for the purposes of the Financial Service Providers (Registration and Dispute Resolution) Act 2008 (FSPA) and the Financial Advisers Act 2008 (FAA) of New Zealand. GSAMA is not a registered financial service provider under the FSPA. GSAMA does not have a place of business in New Zealand. In New Zealand, this document, and any access to it, is intended only for a person who has first satisfied GSAMA that the person falls within the definition of a wholesale client for the purposes of both the FSPA and the FAA. This document is intended for viewing only by the intended recipient. This document may not be reproduced or distributed to any person in whole or in part without the prior written consent of GSAMA. This information discusses general market activity, industry or sector trends, or other broad based economic, market or political conditions and should not be construed as research or investment advice. The material provided herein is for informational purposes only. This presentation does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation.

Canada: This material has been communicated in Canada by Goldman Sachs Asset Management, L.P. (GSAM LP). GSAM LP is registered as a portfolio manager under securities legislation in certain provinces of Canada, as a non-resident commodity trading manager under the commodity futures legislation of Ontario and as a portfolio manager under the derivatives legislation of Quebec. In other provinces, GSAM LP conducts its activities under exemptions from the adviser registration requirements. In certain provinces, GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts and is not offering to provide such investment advisory or portfolio management services in such provinces by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law by Goldman Sachs Asset Management Co., Ltd.

Confidentiality

No part of this material may, without GSAM’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized agent of the recipient.

Please enter the email that you signed up with below. If your email is

connected to a member account, we will send you a reset link.

This website uses cookies and asks for your personal data to enhance your browsing experience. We are committed to protecting your privacy and ensuring your data is handled in compliance with the General Data Protection Regulation (GDPR).