Drawing upon its position as a leading global bank, Bank of America Merrill Lynch (BofAML) has a comprehensive and global view of the issues affecting today’s treasurers. In the first part of Treasury Today and Bank of America Merrill Lynch’s Executive Series experts from the bank joined a roundtable discussion hosted by Treasury Today Chair, Richard Parkinson, to provide their insights into a diverse range of topics, from the rise of artificial intelligence (AI) in treasury management systems to the importance of measuring environmental, social and governance (ESG) factors for companies.

Participants

Matthew Davies

Head of Global Transaction Services EMEA

Stephanie Wolf

Global Head of Financial Institutions & Public Sector Banking for Global Transaction Services

Hubert J.P. Jolly

Global Head of Financing and Channels, Global Transaction Services

Moderator

Richard Parkinson

Chair, Treasury Today Group

Matthew Davies, Head of Global Transaction Services EMEA: Matthew heads up the global transaction services business for BofAML for Europe, Middle East and Africa. We spend a huge amount of time with our US client base, but we also have significant international relationships with our European, Asian and Latin American headquartered clients. Some of those perspectives differ, so I want to try and share some of those today.

Stephanie Wolf, Global Head of Financial Institutions & Public Sector Banking for Global Transaction Services: I run our global financial services franchise from a client-coverage perspective. That includes traditional financial institutions, our correspondent bank clients and non-bank financial institutions, as well as global government entities, around the world.

Hubert J.P. Jolly, Global Head of Financing and Channels, Global Transaction Services: J.P. has responsibility for financing and channels, which includes BofAML’s trade and supply chain business, cards and payables. This is a comprehensive solution set, so pre-paid and commercial cards, digital channels, online mobile direct connectivity and innovation all fall within my domain.

What is going on in corporate treasury today? Are the fundamentals changing and what are the key trends you are seeing?

Matthew Davies: There has been quite a shift since the global financial crisis. Up until that point, the focus was very much on traditional areas of treasury. That focus continues today but what has changed is that the role of the treasurer has become so much broader. Treasurers have had to develop new skillsets to spread the reach of treasury much further across the company.

J.P. Jolly: Corporates are also looking to drive operating efficiency from technology, which includes digitising the treasury function. Digitisation is driving treasurers to review their supply chains, and how they can help their partners in procurement and manufacturing be more efficient. This includes how they should pay their suppliers and how they can get capital to suppliers who may require it. Last but not least, they are exploring how they can help their companies collect payments more efficiently.

Resources in corporate treasury are always limited. So how do you see corporates coping with the need to digitise?

Matthew Davies: Introducing automation through the use of robotics can enable treasury to become much more efficient. This offers a great opportunity for corporate treasuries to gain that efficiency so they can use the resources that they have much more effectively on strategic initiatives.

Matthew Davies

J.P. Jolly: I think there is an opportunity to free up working capital, particularly given rising interest rates in the US and other markets. We are seeing some corporates deploying supply chain finance when they haven’t done so before.

We are also combining supply chain finance with virtual purchasing cards in order to provide clients with a seamless solution. For example, by leveraging the data that we have, we may be able to determine that a company’s smaller suppliers could benefit from a virtual P-Card.

Meanwhile, treasurers are focusing on extending days payables outstanding (DPO) in order to free up working capital for their corporations, drive benefits and, in turn, get more investments into the treasury.

Stephanie Wolf: We have a whole generation of treasurers and treasury departments who have not lived through a rising interest rate environment. So we spend a lot of time with our clients talking about how that environment impacts the deposit rates, the borrowing rates and the working capital cycle as a whole.

J.P. Jolly: I think treasurers also need to look at their inflows and ask how they can leverage technology to reduce outstanding receipts and collect cash faster. So it’s all about maximising your inflows, collecting faster, leveraging bank tools to pay your suppliers later, extending your cash flow and improving your working capital.

Stephanie Wolf: On the inflow side, we have used AI to help when receivables come in. We have a global product used by many of our clients where, as the receipt is confirmed, we use artificial intelligence to determine where those receivables should be applied.

Matthew Davies: We have some clients that previously had automated match rates of 30-35% for their incoming receivables. By deploying this type of technology, they have been able to increase the match rate to 75-80%. That is a major efficiency gain which can free up a significant amount of resources.

Which trends should corporates be watching right now?

Matthew Davies: Corporate treasurers should be focused on the automation opportunities that we are talking about. Beyond that, it is really about how fintechs can help drive change in the broader market place. Stephanie just gave the example around intelligent receivables, where we partnered with a fintech – I think it is interesting to watch how banks are partnering with fintechs and what that is enabling them to bring to market. We are seeing much more collaboration in the bank/fintech space.

J.P. Jolly: Treasurers are looking to their banking partners to innovate to help them work smarter and more efficiently. This could mean propriety bank products or partnering with fintechs.

Staying on top of market trends and priorities is so important to innovation. Last year, we worked with Treasury Today on the Voice of the Corporate Treasury Global Study. The study provided insight on corporate treasurer’s priorities over the next 12-18 months. Truly understanding trends and our clients’ needs is key to delivering the right solutions.

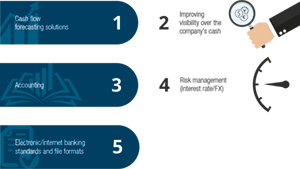

Top five priorities for corporates over the next 12-18 months

Extract from the findings of Treasury Today’s Voice of Corporate Treasury Study 2017

Stephanie Wolf: Of course, cybersecurity is applicable to every single one of our clients and it is applicable to all of us personally. So, we at BofAML have taken a global position that we are here to share information on how we think about cybersecurity – and, where we can, offer advice.

Matthew Davies: You can imagine that as a large global bank, we have to spend a huge amount of time, money and resources protecting the bank every minute of every day. We try to leverage that expertise to give advice to our clients on how we protect ourselves, because it is equally applicable to them.

Stephanie Wolf: And technology helps the ‘knowing your client’ relationship work much better. We have used technology to build databases that give us information on what a particular client or industry of clients or region of clients are doing. What type of receipts are we seeing? What type of payments? What is the gap between a receipt and a payment? What means of executing a payment is being used? We meet with our clients regularly and then we bring that knowledge to achieve more efficient execution.

Almost an element of benchmarking there?

Stephanie Wolf: It is very interesting when you try to find a comparison. Not every company is comparable to the company you might think they would be compared to. I’ll give you an example. One company might simply be a manufacturer of a product. Another might be a global manufacturer of that same product as well as six others. They are very different companies. So we try to look at their behaviour, rather than just the industry sector. That is where you start to find commonality.

Let’s turn to regulation. Obviously, there are enormous regulatory pressures on your industry and, in turn, on your clients.

Stephanie Wolf: I look at regulation as an opportunity for us to evolve. When I think about PSD2, the second payment services directive out of the EU – what did we do when faced with that regulation? We created an entirely new way to connect with our clients via API connectivity.

Stephanie Wolf

Matthew Davies: Regulation is both a challenge and an opportunity. It is a challenge for all banks to be able to fund growth whilst staying compliant. But the opportunity is significant and we have seen many examples of regulation driving positive change.

Faster payments came to the UK and it was driving a better consumer experience. We have now seen this transition towards real-time payments on a global basis. If you have full open banking and you have full real-time payments, you will probably think very differently about which banks you pick to work with in a number of different jurisdictions.

J.P. Jolly: Speaking of real-time payments and APIs, this really is an opportunity for corporates on the collections and receivables end. This enables them to take a real-time approach when it comes to collecting money. They may also be able to leverage APIs to connect to whichever system their clients are using and source the information they need to reconcile invoices.

Matthew Davies: That is a great point. We spend a lot of time talking about the speed of the payment. Actually, one of the biggest benefits from real-time payments is the increased level of information that can be passed alongside the transaction.

Is there an impact on cash flow forecasting here as well?

Stephanie Wolf: Most definitely. Certainty is of great value to corporate treasurers around the world and as J.P. was saying, we are spending our technology dollars on ways to offer our clients better cash flow forecasting tools. Indeed, respondents to the Treasury Today Voice of Corporate Treasury Global Study said that the most valued service their financial services partners provide is greater transparency in the cash flow forecasting process.

Matthew Davies: A number of corporate clients are thinking very differently about how they can use technology for cash flow forecasting. For example, one company has taken its bank statements and open item files from SAP, and all its history from its ERP systems, and loaded them into Watson, the cloud service from IBM. Then Watson uses AI and machine learning to deliver cash flow forecasting for the company.

Now this is early stages, but it is very interesting to see what you can now do with the cloud-based artificial intelligence solutions that are on the market.

On a different note, another business trend is the measurement of ESG factors. How important is this and what should corporate treasury be doing in this space?

Matthew Davies: You can look at this a couple of ways. I think we see it as important because for us it is very much linked with responsible growth. This means making sure we are the best employer for our employees, and using the significant resources that we have around the world to do the right thing for our clients and the communities that we operate in.

Recently we have started to look at our customers and try to build an ESG scorecard. Interestingly, when you look at it, around 50% of corporate treasurers are involved with and engaged in ESG programmes within their organisations. The other 50% really don’t know anything about it. And I really do think for corporate treasurers, it will be increasingly important to focus on this area – firstly because it is the right thing to do, but also because investors are focused on this topic too.

When assessing bank relationships, corporates rate the following factors as the highest priorities

Extract from the findings of Treasury Today’s Voice of Corporate Treasury Study 2017

What do you see as some of the winning factors for modern corporate treasury?

Stephanie Wolf: The key is to stay nimble, look at how your group is organised, review the technology you use and get your processes to change as your systems change – then you will be far more successful.

And a second aspect that I see in the clients who are most successful, is the ability to take in information across the landscape and to have designated experts, both externally and internally.

Matthew Davies: Yes, you need good advisors around you and to make sure you have got the right relationships with the right banks that give you the right level of advice and service. I also think the modern treasurer needs to be both proactive and intellectually curious.

J.P. Jolly: People are very focused on running a proposal process and maybe on selecting the best price – but that is not always the best indicator in terms of how easy it is going to be do business with a particular provider.

What else should corporates be watching?

Stephanie Wolf: Technology is a must in this day and age. If you are a treasury group that is not technologically proficient, you will fail.

Another important industry trend is open banking, which is leading to more cross-border low-value payments. Beyond technology, the biggest change for my clients over the next five or six years is going to be low-value, cross-border, cross-currency payments becoming cost effective and, therefore, more prevalent.

So corporate treasury has to be curious, nimble, but also proactive. How do you help your clients do that?

J.P.Jolly

J.P. Jolly: Well, I think some of our most successful clients in terms of freeing up working capital are the ones who partner with procurement in a collaborative way. Traditional banks look at these three products – supply chain, payments and cards – as three separate silos. We don’t. We take an integrated approach to include all of a company’s suppliers in a single implementation.

Stephanie Wolf: The first time we implemented our Digital Disbursements solution, it came out of a whiteboard session where we spent an entire afternoon sitting with an insurance company’s department head, thinking about the future of paying insurance claims. And that led to the execution of a particular solution – which, in turn, led to a rather dramatic change in the industry as to how claims are paid as well as unearned premiums.

Matthew Davies: In another case, really understanding some of the challenges of the sales organisation was key. The company’s sales organisation had a number of clients that wanted to buy a lot more products – but the sales organisation was unable to sell more products to them because of customer limits which were included in the internal credit policy.

Of course, if you can identify the cash and apply it quicker, you can free up that credit limit quicker and therefore sell more product. But it’s also important to consider what you know about your customers and whether you have the right view and the right limits in place.

By looking at how the company’s clients paid, the company was able to adjust its credit limits and sell more, while still maintaining the same risk profile that it had previously. This is a great example of a treasurer taking a commercial view and helping the organisation be more successful in selling to its clients.

I would like you to summarise. What are the key takeaways that you would like to leave with the reader?

Matthew Davies: I am very much of the view that transaction banking is going to change more in the next five years than it has in the last 35 years.

There will be significant opportunity for efficiency gains, cost reductions, greater transparency and better advice driven by data. We’ll continue to do our part in providing advice on a consistent basis across all of these areas, but I think there has got to be that intellectual curiosity there.

Stephanie Wolf: One thing that is constant is change. Treasurers have to be willing to look at the landscape, take all the information they can and apply it to their specific circumstances.

J.P. Jolly: The right approach is to look at how digitisation helps us improve the client experience that we provide to our clients.

Whenever I meet with my colleagues in operations, service, fulfilments or implementation, they measure themselves based on client delight. So, one major trend that treasurers should look at is what are my banks doing to make it easier for me to do business with them?

This discussion highlights that while customer needs and the client experience remain paramount, recent developments and the evolving landscape are continuing to change the needs and challenges faced by treasurers. It’s clear that corporate treasurers are operating in interesting, not just difficult, times and that the coming years will see the arrival of many more examples of innovation and collaborative solutions.

Top five areas in need of improvement in terms of the use of existing technology

Extract from the findings of Treasury Today’s Voice of Corporate Treasury Study 2017

Treasury Today’s Voice of Corporate Treasury Study 2017 was conducted from February to April and attracted over 600 responses from a broad universe in terms of company size, industry sector and geography.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.