-

It wants to shed the obligation to intervene wherever a conflict or war breaks out. As long as no major US interests are directly at stake, America opts to stay on the sidelines where possible.

-

Washington realises that the world may soon be heading towards the formation of two large power blocs: China together with Russia on one side, and the US on the other. Where India and Western Europe will ultimately end up remains unclear.

Each of the major blocs will seek to gain the greatest possible influence in the rest of the world, particularly when it comes to commodities, water and so on. This could lead to serious conflicts.

The conclusion Washington appears to be drawing from this is that it wants to disengage from the rest of the world as far as possible, except in cases where essential US interests are at stake. The top priorities are national security and independence from the rest of the world.

Import tariffs

At this point, the US remains heavily dependent on (Chinese) imports – goods the US cannot easily do without. The most obvious example are the critical raw materials required for the production of modern technological equipment, over which China holds a near-monopoly. Furthermore, there is a wide array of semi-finished products that require advanced technological knowledge and skills; they are far cheaper to produce in China and cannot simply be relocated from China back to the US. It takes years to build the necessary plants in the US, and production would also become far more expensive. It is also uncertain whether the US has enough workers for this, especially considering that many foreigners are being driven out of the country.

Even so, Trump and the team around him believe this must be done. The world is changing in such a way that it is becoming irresponsible for the US to remain heavily dependent on foreign imports. This is why the US is now resorting to the introduction of tariffs and other trade-restrictive measures.

In our view, the focus tends to be too much on the economic consequences of the tariffs – higher inflation and lower economic growth in the US. Many believe this will ultimately force Trump to proceed relatively cautiously with import tariffs. However, we fear that fairly high tariffs are bound to materialise. Needless to say, this will result in damage to the US economy, but according to the Trump team, this is the price that must be paid to guarantee national security. Moreover, this price may turn out to be modest, if we also consider public finances.

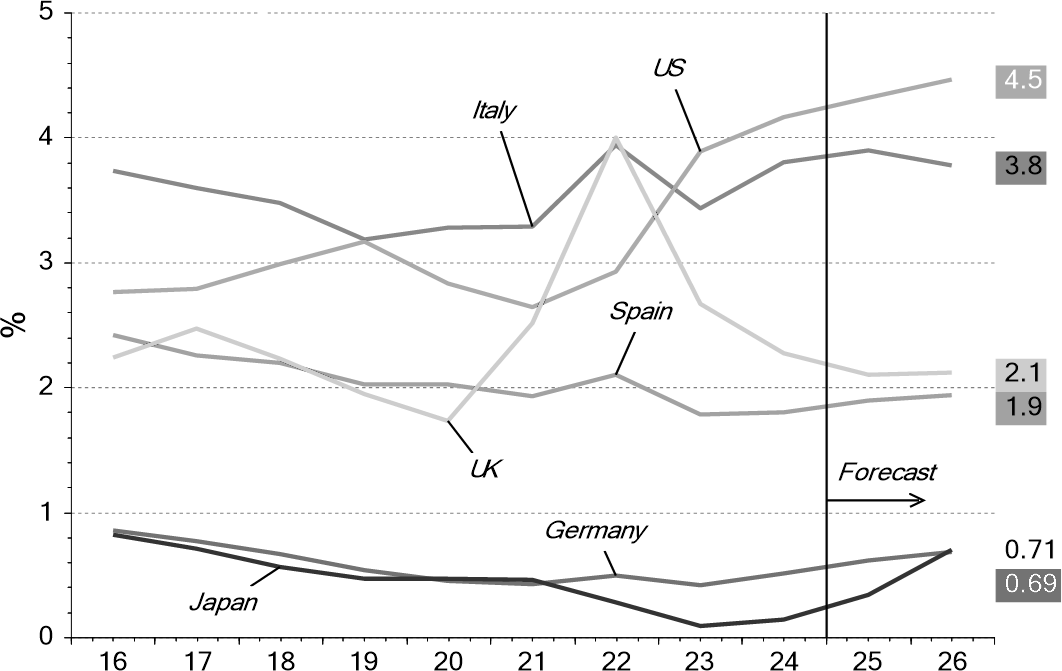

US public finances heading for derailment

If developments indeed head in the direction of fairly high tariffs, this would have two major drawbacks as it will reduce purchasing power of US consumers and will cause a lot of uncertainty for businesses as countries will retaliate.

As the import tariffs also push up inflation, the Fed has very limited scope to stimulate the economy monetarily. This will therefore have to be done through fiscal policy. This is precisely what the Trump administration is working on. Enormous pressure is being put on Congress to cut taxes. The question, of course, is to what extent the public deficit can or should be widened further as it already stands at around 6.5% of GDP and interest payments are rising rapidly due to the high interest rates. In any case, many politicians (want to) believe that the deficit can be contained by:

-

Revenue from import tariffs.

-

Spending cuts in a number of areas, such as healthcare and other social expenditures.

-

Higher growth resulting from tax cuts and deregulation.