Treasury centralisation: is it really the ideal set-up?

Published: Oct 2019

A highly centralised treasury function is often cited as the most efficient and favourable model for the majority of treasury tasks, yet relatively few corporations have achieved it. It may be time to re-assess this view. Treasury and finance consultant, Christian Bartsch, Professor Business Administration (Finance & Accounting) at IUBH University of Applied Sciences, explores the drivers.

Companies used to operate under decentralised treasury management systems in which organisations frequently executed treasury management functions locally. However, changes in the business environment, such as recessions and the deregulation of money markets, led to the centralisation of treasury management.

The first function to be centralised was usually cash management. However, other functions such as risk management and the management of the liquidity and capital of an organisation were also centralised following the introduction of advanced technologies.

“The goal is to achieve excellent access to liquidity and have the most transparent view of potential risks to manage the treasury function of a company effectively,” explains Christian Bartsch, Professor Business Administration (Finance & Accounting) at IUBH University of Applied Sciences, Finance Director of a global IT/software business and an active participant within the Cash & Liquidity working group at the Association of German Treasurers.

The trend has been to centralise treasury functions to accrue benefits such as reduced operating costs and maximised returns on investment. In reality, notes Bartsch, who also has his own financial interim, project management and consulting company, Cavetio, “the degree of treasury function centralisation is still far from the theory.”

Using research based on a survey conducted among non-financial European companies of the STOXX Europe 600 index in the area of corporate treasury management (and used for his own doctoral thesis) Bartsch targets the ‘ideal’.

Definition and responsibilities

The corporate treasury function can be interpreted in many ways. It can range from an essential corporate function which operates as a cost centre, to an active function which has to earn a profit like a regular business and, therefore, operates as a profit centre. In between are service centres for advising the business units. “According to the survey conducted, almost 70% of the companies see their treasury function as a service centre, about 25% as a cost centre, and the remaining 5% as a profit centre,” notes Bartsch.

In terms of the degree of centralisation, it is interesting to see that 60% of the respondents indicated that their treasury is either highly centralised or organised at group level. Surprisingly, none of the respondents had a local corporate treasury management set-up, nor were any operating at the single entity level.

“Almost 3% of respondents had a corporate treasury management set-up organised by country or centralised/group which were also mainly decentralised,” he notes. “Hence, no respondent had a highly decentralised corporate treasury management set-up: rather, they all indicated they had a partially or highly centralised corporate treasury management model.”

As corporate treasury and its tasks are not clearly defined, the respondents were asked to state which tasks are performed by their corporation’s treasury function. From the list of functions provided, nearly all were said to be performed by corporate treasury management to a large extent.

Some functions, namely cash management and pooling, funding (bank loans, funding, credit facilities), foreign exchange risk management, and interest rate risk management, are performed by more than 90% of the respondents’ organisations, and could, therefore, be defined as core corporate treasury tasks.

Introducing the ideal

In 2007 – even before the global financial crisis – academic, Shelly Heiden, emphasised the need for effective financial management. “Today, perhaps more than ever, organisations of all sizes and across all industries face significant pressures as they grow their businesses in a competitive and increasingly global economy,” wrote Heiden. “These organisations are constantly reorganising and restructuring in response to economic conditions, global expansion, an onslaught of new technologies and other factors beyond their control.”

To understand the need for centralisation, the respondents to the STOXX Europe 600 survey were also asked to state their current and their ideal degree of centralisation per task. Bartsch reports that each respondent indicated the organisational level at which all tasks/functions are handled in their ‘current’ set-up and in their ‘ideal world’ set-up.

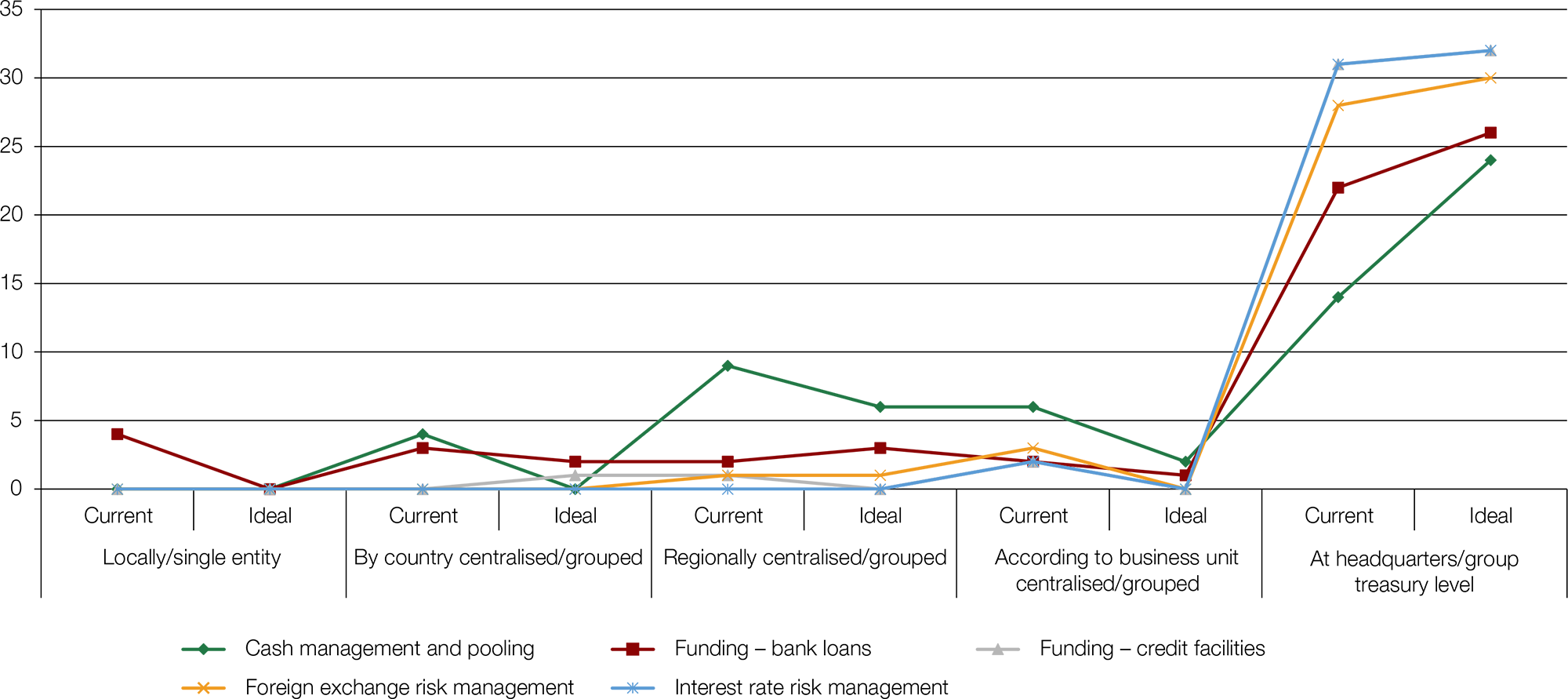

Focusing on the five core corporate treasury tasks, the following comparisons between current and ideal can be drawn:

Figure 1: Comparison of current and ideal set-up for the five core treasury tasks

Figure 1 shows that ‘current’ is very close to ‘ideal’ for three out of the five tasks, but, for two of them, it differs markedly. This becomes clearer in Table 1, which illustrates the factor of centralisation (meaning 1 local, and 5 fully centralised):

Table 1: Degree of centralisation of the five core treasury tasks

Current

Ideal

Delta

Cash management and pooling

3,91

4,56

0,65

Funding – bank loans

4,06

4,59

0,53

Funding – credit facilities

4,88

4,91

0,03

Foreign exchange risk management

4,84

4,94

0,10

Interest rate risk management

4,94

5,00

0,06

“The clear gap between the ideal and the current set-up of around factor 0,5 indicates that the two tasks – cash management and pooling, and funding via bank loans – should be more centralised, but are not as yet,” he notes.

Resisting centralisation

Based on the reviewed literature (Bartsch cites Casey 2008; Clarke & McAleese 2000; Mulligan 2001; Polak 2010; Polak & Roslan 2009a, 2009b; van Alphen & Huiskes 2008; Weiner 2008), the following factors appear to affect the centralisation decisions of corporate treasury functions:

Tax implications.

Legal implications.

Central banking requirements/reporting.

Accounting implications.

Business requirements.

Access to financial markets.

Compliance implications.

Technological infrastructure.

Banking (infra)structure and relationships.

Company culture.

Staffing (costs and qualifications).

Staff training.

Staff motivation.

Cost savings.

Reason to change?

Clearly, a variety of challenges and factors influence a corporate treasury’s decision to become centralised. “In some areas, research has shown the optimal or achievable level of centralisation has already been reached,” notes Bartsch.

While there are benefits to a central approach, the practicality and suitability of various organisational models need to be considered. Many influencing factors and individual company situations surround the possibilities and decisions relating to centralising treasury functions.

“Centralising can improve corporate treasury management. However, the limiting factors need to be understood to support and assist corporations to improve their corporate treasury function,” concludes Bartsch. “Despite the advantages of central management, one must keenly observe local requirements and regulations before making the decision to centralise.”

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.