Considerable uncertainty has arisen in the US and around the world which could have a crippling effect on corporate investment. Elsewhere, this edition’s Market View finds several forces at play that are exerting upward pressure on US interest rates.

Trump II has taken Washington by storm and altered US foreign policy relations to a great extent. The number and speed of executive orders from Trump has been breathtaking, but the ones relevant for the economy can be grouped as follows:

Trade policy (import tariffs).

Cutbacks in government spending and bureaucracy.

Migration policy.

Deregulation.

Economic implications

We are well aware that there are widely differing views on these topics. In any event, it is clear that they are fuelling uncertainty. For example, every business in the West will wonder if a trade war will still break out, and if so, how long it will last. And even if the damage remains limited to a modest number of import tariffs, there is no way to know if they will be expanded or quickly repealed. This is compounded by a great deal of other political uncertainty, such as whether Europe will fall apart or act more collectively and whether the US government will continue to function and how it will function in view of the DOGE operations, for example.

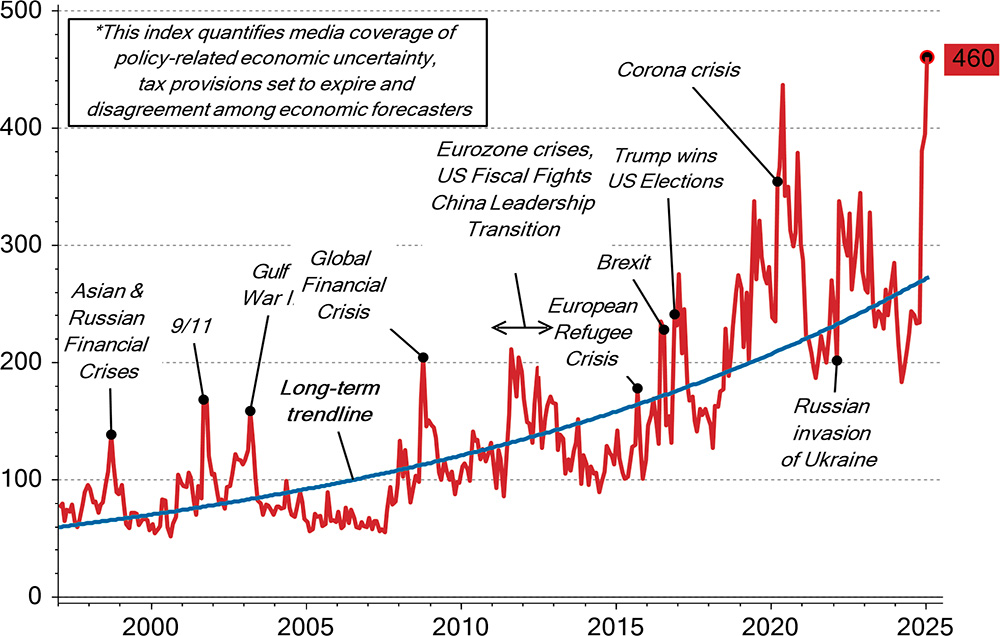

Chart 1: World Economic Policy Uncertainty Index

Source: LSEG Datastream/ECR Research

In short, considerable uncertainty has arisen in the US and around the world. We believe this has a crippling effect on corporate investment – our consulting arm also hears this from companies – and consumers.

This uncertainty, tax cuts that will not materialise for now and a Fed that is unable to cut interest rates aggressively (due to upward inflationary pressures owing to tighter migration policies and protectionism) are factors that will probably lead to a – possibly significant – scaling back of growth expectations for the US economy.

Prospects for the European economy do not seem great either, but Europe is coming under enormous pressure to ramp up defence spending at a very rapid pace. To finance this, European countries will have to significantly step up borrowing. It is therefore possible that current developments will lead to more co-operation and fiscal stimulus in Europe. To some extent, this could also offset the negative impact of any US tariffs on European imports.

A warning

If the US and European economies indeed slow down due to uncertainties, this may have far-reaching consequences.

As it looks now, the US public deficit-to-GDP ratio will not change much. This is assuming the economy continues to grow at about 2.5%. If this growth rate declines sharply, the deficit will shoot up further. This means that the so-called twin deficits – public sector and current account deficits – will become even larger. This, in turn, means the US will have to attract even more money from abroad to finance its deficits. However, it is highly doubtful whether this will succeed amid ongoing uncertainty and lower growth. This will result in a weaker dollar – which will further slow capital inflows into the US – and/or higher US longer-term interest rates (the latter despite the fact that the Fed will cut short-term interest rates in this case).

If US long-term interest rates rise, the markets will begin to price in an even larger and faster rising public deficit, causing interest rates to rise even higher and so on – until everything grinds to a halt. It will not come to this, however, as it is far more likely that the Fed will finance the deficits by creating more money, resulting in (sharply) rising inflation.

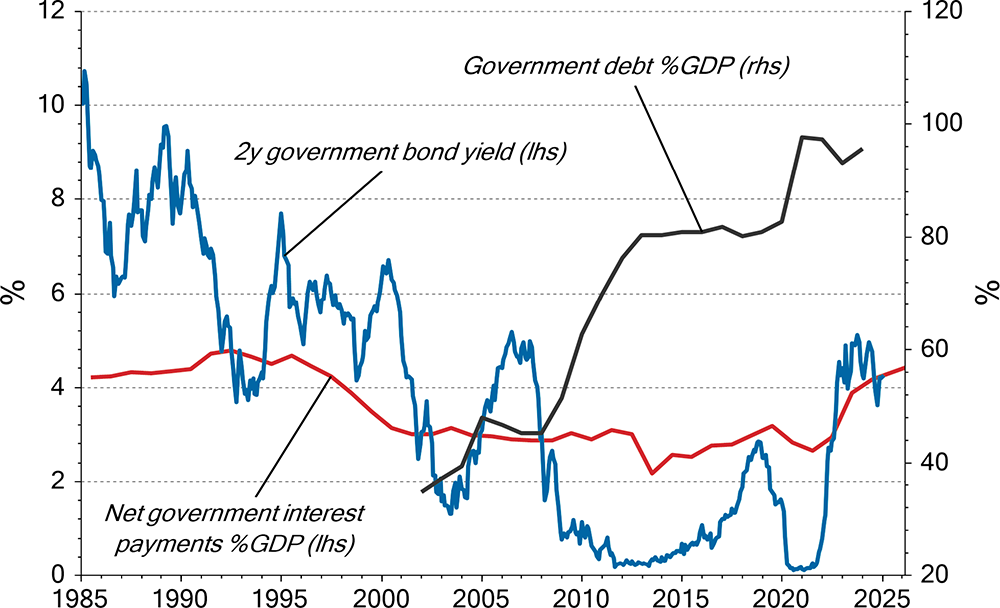

Chart 2: The fast growing US debt pile could become unsustainable if bond yields remain at, or rise from current levels

Source: LSEG Datastream/ECR Research

Another negative implication in this scenario is that European public finances will also start to deteriorate. This will make it even more challenging for Europe to quickly build a military force. Putin could take advantage of Europe’s weakness in this case. Many experts warn that he will then seek to further weaken Europe, particularly through cyber war, fake news, etc. This could unite Europe, but it could also divide the continent.

We wish to explicitly emphasise that it is by no means certain that developments will head in this direction. However, we want to warn that there is a scenario with a negative outcome, and that the likelihood of this negative scenario is increasing. Next, we explain what this all means for US interest rates.

US Interest rates

At this point, there are several forces at play that are exerting upward pressure on US interest rates:

Import tariffs drive inflation higher.

There are no indications that the public deficit will be curbed significantly. Musk is trying to cut government spending as far as possible. However, even if the revenue from import tariffs is included, this will not be enough to fully fund the tax cuts Trump wants to implement; especially if economic growth falls back due to the many uncertainties.

The ease with which Trump has turned away from the Ukraine overnight is plain for all to see. In addition, Trump’s import tariffs harm allies. Especially in the event of a trade war, Trump will probably not shy away from blocking or confiscating foreign assets. All this probably means that foreign countries will want to scale back investment in the US, resulting in less overseas demand for US bonds. This sentiment will be reinforced if it turns out that the rapprochement with Putin has nothing to do with a larger plan to weaken China.

It is possible that said upward forces on interest rates will be offset by a strong downward force: declining economic growth. If the latter is the case – a scenario we currently consider to be the most likely – the Fed will likely provide roughly four rate cuts of 0.25 percentage points this year and US long-term interest rates will decline further. If, on the other hand, growth shows only a modest decline, we expect a maximum of one rate cut of 0.25 percentage points by the end of this year, after which interest rates will likely be raised again in 2026. In this scenario, the ten-year US government bond yield will likely start an uptrend to 5% or higher.