The combination of political uncertainty, trade tensions, and data loss makes it almost impossible to predict the economic direction.

Two possible directions

Broadly speaking, two scenarios are emerging for the coming months. First, the growth scenario: the AI boom and wealth effects continue, consumption remains reasonably stable, and job growth picks up slightly again. In that case, inflation will rise gradually, and the Federal Reserve will only moderately expand or even stabilise its policy.

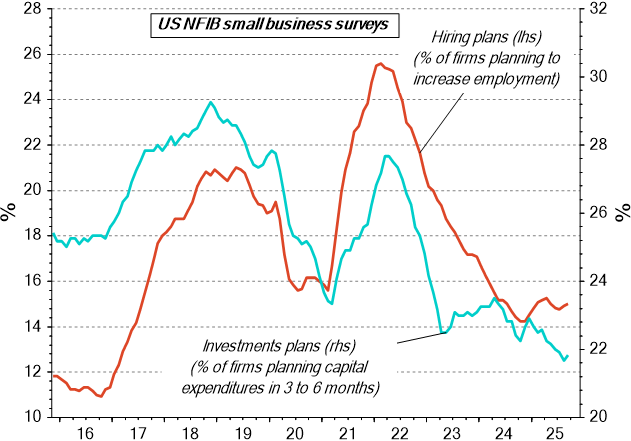

Secondly, the recession scenario: job growth remains weak, purchasing power declines, and consumer spending falls. Companies invest less and no longer hire permanent staff. This can cause a downward spiral in which unemployment rises, and the economy slides into recession.

The Fed will try to avoid this latter scenario at all costs. High debt levels mean a recession could quickly degenerate into a credit crisis, while the scope for new stimulus measures is limited. The central bank therefore must strike a delicate balance: too little easing could tip growth into decline, while too much easing could reignite inflation.

The Fed’s position

The lack of reliable figures puts the Fed in a difficult position. Policy must be determined on the basis of partial information and trends that may already be outdated. The central bank is therefore likely to err on the side of caution: it is better to have too much stimulus than to put the brakes on too soon.

There is a good chance that the Fed will implement a few more interest rate cuts in the coming quarters to support the economy, but the pace of these cuts will depend on the direction in which the labour market develops. Once there is more clarity and growth stabilises, the bank will gradually make its policy more neutral.

It is important to note that the Fed responds not only to current figures, but also to market expectations. As uncertainty decreases, investors will adjust their scenarios – and that could tighten financial conditions even before the Fed itself takes action.

Politics and market sentiment

The ongoing lawsuit over import tariffs could have major consequences. A ruling requiring refunds would not only blow a hole in the budget but also put further pressure on trade relations. At the same time, the government will try to develop a plan B to maintain tariffs in a different way. That process will take time and is likely to cause new tensions.

When greater clarity finally emerges – for example, when the shutdown ends and data publication resumes – attention will shift back to the underlying fundamentals of the economy: moderate structural growth and limited policy scope to sustain that growth.

In light of the above, the Fed is likely to ease less than is currently priced in. It may even have to raise rates again in the course of 2026. This also means that ECR Research do not expect long-term interest rates to fall much further and see them gradually entering an uptrend.

Structural constraints

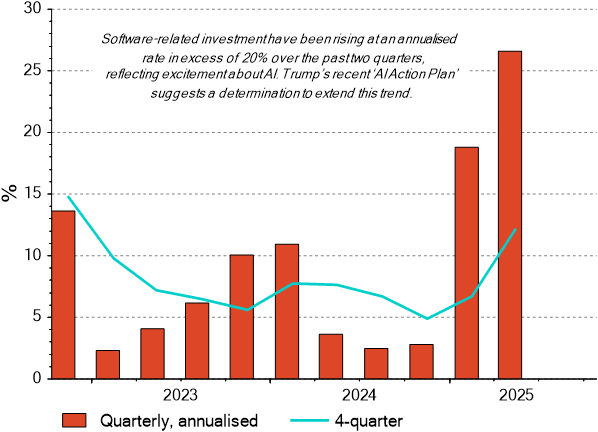

In the longer term, the potential growth of the US economy remains low. Due to an ageing population, stagnating labour participation and declining immigration, the working population is barely growing. Productivity gains must make up the difference, but it is uncertain whether recent investments in artificial intelligence can deliver on that promise.

Even if AI does increase productivity in the long term, it could take years before this is reflected in the macroeconomic figures. Until then, the economy will remain vulnerable to shocks, and fiscal policy will be the main source of stimulus. However, fiscal space is shrinking due to rising interest expenditure and a deficit of around 6% of GDP.

This means that the government is structurally spending more than it is taking in, while interest costs are consuming an increasingly large portion of the budget. As long as real interest rates remain above economic growth, the debt ratio will automatically rise. As a result, the US is at risk of ending up in a structural dilemma: stimulating the economy to maintain growth will eventually lead to higher inflation and interest rates, while austerity measures to reduce debt may actually slow down growth.