How treasurers can unlock opportunities in the API economy

Published: Oct 2018

How can corporates prosper on the journey from PSD2 to Open Banking? A prominent banker offers his take on this eagerly awaited development.

By extracting value from data pools and delivering it instantly, Application Programming Interfaces (APIs) have the potential to upscale corporate treasurers’ experience and improve their business processes markedly. So says, Christian Schaefer, Deutsche Bank’s Head of Payments, Corporate Cash Management.

In Europe, APIs have become particularly relevant due to PSD2. While this directive came into force on 13th January 2018, the regulation’s most transformational provisions – which mandate banks to provide third-party payment service providers (TPPs) access to client bank accounts – only come into effect in September 2019. Most banks will enable this through the use of APIs.

However, despite abundant media attention, Schaefer says many corporate treasurers are yet to realise the opportunities that access to accounts can open up. “Not only can TPP services streamline and reduce payment costs, but corporates can ultimately upscale the quality of their service by providing value-added services to their own customers.”

As such, corporates need to understand the various opportunities that are emerging off the back of PSD2, and how they can seize these to reshape their payment models. Schaefer offers the following:

What practical steps can treasurers take now?

For corporate treasurers, PSD2 will mean more choice as to how they make payments, creating clear opportunities for cost reductions, better information flows and more user-friendly experiences. And, what’s more, corporates will not have to make any substantial changes in order to enjoy these benefits.

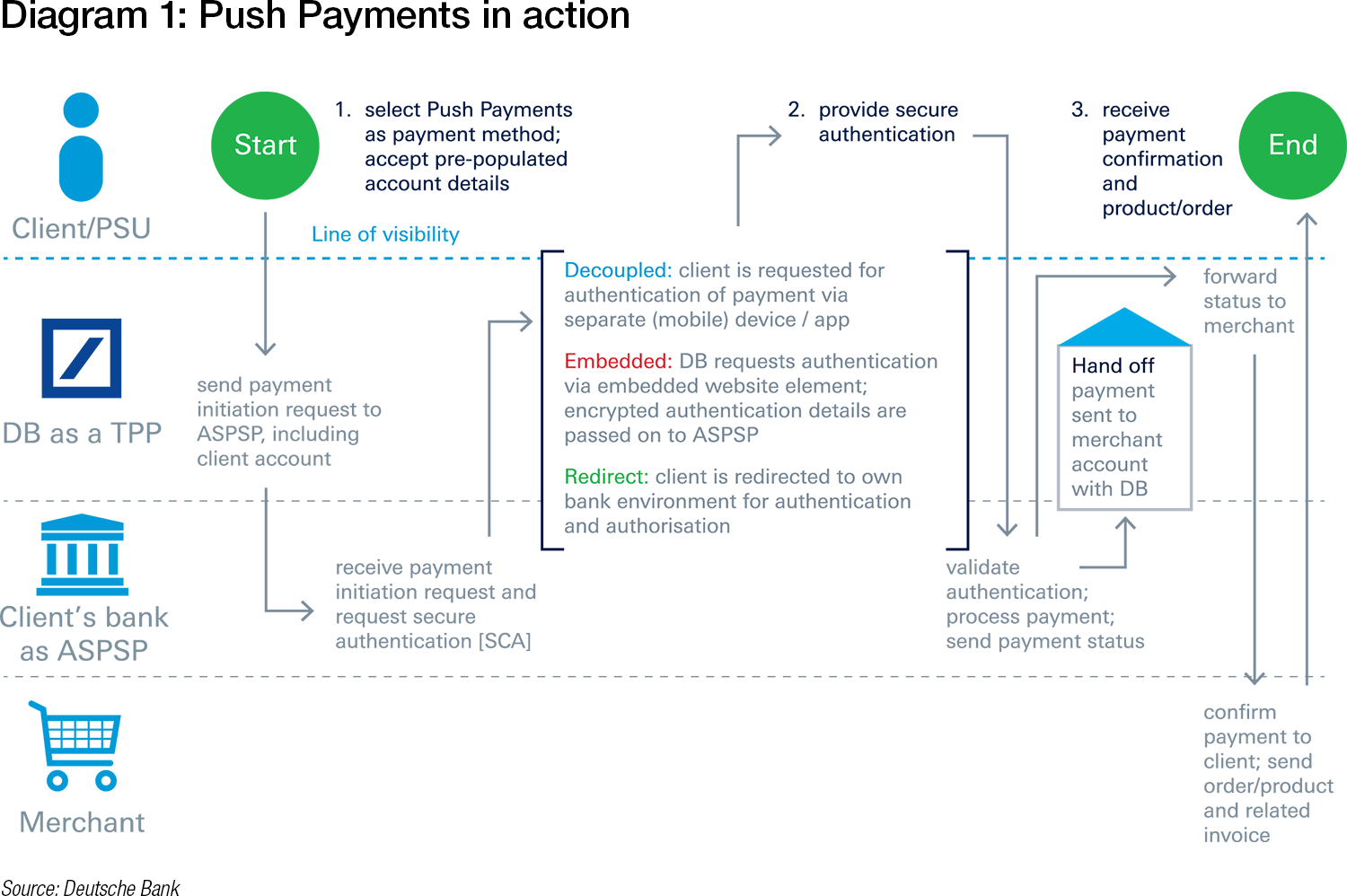

Corporates – in particular those involved in ecommerce or the internet of things – may consider introducing a payment initiation service offering push payments (see the image for how this works in practice).

This could reduce the cost of payment instruments (such as cards or e-money), reduce default risk for direct debits, and in some instances, speed-up settlement times. Since it is mandatory for TPP payment initiation services to use two factor customer authentication – a security measure whereby two types of information are required from the user – these payments are expected to be less susceptible to fraudulent behaviour.

Diagram 1: Push Payments in action

Source: Deutsche Bank

By opting to receive TPP account information services, corporates can also work with better and more actionable information. This might include real-time balances on their various accounts with different banks – opening up the possibility of more proactive management of liquidity, using convenient payment initiation services to move funds flexibly to fund major outgoings or earn higher interest.

Making the most of push payments

Many banks have API projects underway. Deutsche Bank’s push payments pilot solution – set to go live with the International Air Transport Association (IATA) – is a practical example of how corporates can adapt their payment models in a PSD2 world.

By implementing a new and improved solution for internet-based ticket sales, Deutsche Bank will collect payments for tickets directly from individual customer accounts, removing the need for them to make credit and debit card transactions to the airlines.

This initiative evades the standard card-network process – with a three- to five-day settlement wait – and, by using instant payments supported by SCT Inst, means payments can be processed and received in near real-time. The result: the airline receives funds faster, generating significant working capital and liquidity benefits. By removing the costly interchange and credit card fees, IATA can also significantly reduce its costs.

Such solutions could be replicated in a business-to-consumer (B2C) context, especially for corporates with complex refund and reconciliation processes for B2C sales, ecommerce providers who pay high interchange fees yet have slow collections, and business-to-business (B2B) corporates that may, in the future, move into the B2C space.

Yet, all of this is only the first stage in a broader development towards Open Banking – the global effort among regulators to use data sharing to increase competition among financial institutions. As Schaefer notes: “Successful navigation of PSD2 will bring further opportunities for those treasurers that move first”.

Please enter the email that you signed up with below. If your email is

connected to a member account, we will send you a reset link.

This website uses cookies and asks for your personal data to enhance your browsing experience. We are committed to protecting your privacy and ensuring your data is handled in compliance with the General Data Protection Regulation (GDPR).