Cash flow issues on the import horizon post-Brexit

Published: Feb 2018

Government plans for UK businesses to pay VAT upfront on post-Brexit EU imports will damage cash flow warns the country’s largest retail body.

UK businesses could face paying VAT upfront on imports from EU countries once the UK’s divorce from the European Union (EU) is finalised in little over a year. This could create cash flow challenges for as many as 130,000 UK business.

“Following Brexit, an international customs border will come into force between the UK and the EU,” explains Jo Bello, Global Indirect Tax Leader at PwC. “As a result, taxes applied to imports will change to customs duty and import VAT – which is treated as a duty of customs – both of which are collected at the UK border by HMRC.”

Big changes

If the law is passed as it currently stands it will mark a significant change for UK businesses. Currently, goods sent between the UK and the EU member states are within the EU Customs Union. As such, they are treated as ‘EU intra-community supplies’ and the equivalent of import VAT is accounted for and, provided the VAT is reclaimable by the business, reclaimed on the same VAT return when goods arrive in the UK.

Because of this arrangement, UK businesses do not have to pay VAT on imported goods until the products are paid for by the end customer.

However, this will change if the UK does not remain in the Customs Union after Brexit, something that Downing Street has stressed the UK will not be part of after Brexit. Imports from EU countries will then be treated in the same way as imports from non-EU countries. This will require UK businesses to pay VAT up-front on these imports.

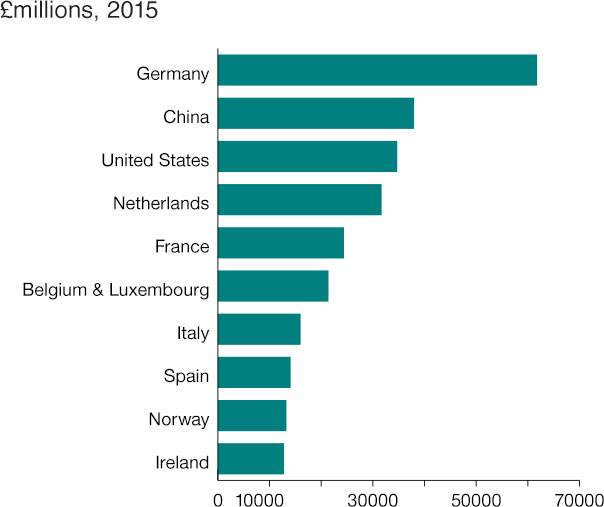

Diagram 1: UK’s top 10 trading partners: goods imports

Source: Pink Book, ONS

Given that seven of the UK’s top ten trading partners for imports are EU countries, the cash flow challenges this might create for UK businesses could be significant. Indeed, a survey towards the end of last year by Barclaycard found that many UK businesses, especially SMEs, are increasingly worried about cash flow. The need to pay VAT upfront on EU imports will only add to this anxiety.

The British Retail Consortium, which represents 70% of the UK retail industry, recently highlighted this concern in a briefing sent to MPs. It said: “Liability for upfront import VAT will create additional cash flow burdens for companies, as well as additional processing time at ports and border entry points attached to the customs process. Mitigation measures could include companies instituting a revolving credit facility, or utilising import VAT deferment reliefs.”

“Both measures require companies having to take out costly bank or insurance-backed guarantees, so would increase the costs of importing goods from the EU.”

The threat of additional processing times at ports and border entry points should not be underplayed. Supply chain processes, including logistics, warehousing and inventory management, may need to be re-engineered to allow for customs delays.

Indeed, Oxford Economics have suggested that the impact of a hard Brexit on Europe’s non-UK supply chains could amount to as much as €62bn in gross output lost in 2020.

Potential respite

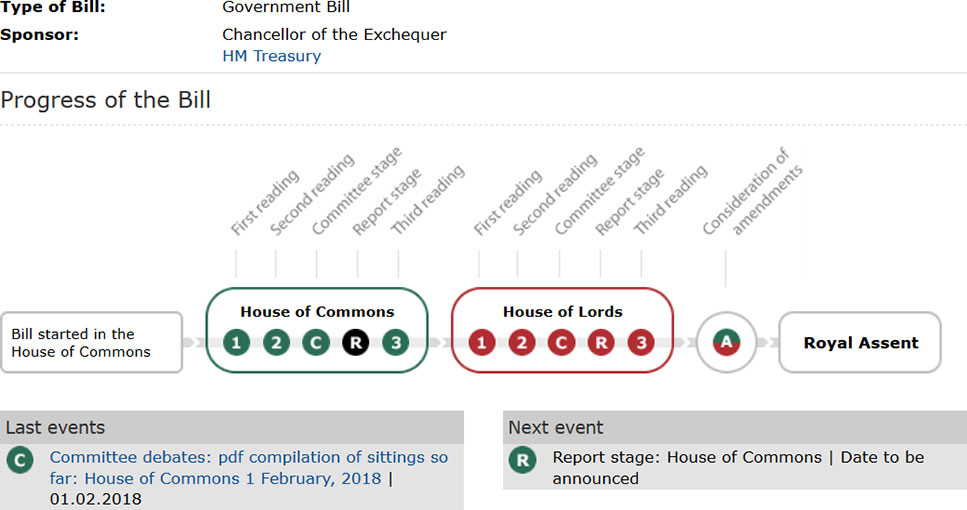

As is the case with many aspects of Brexit, the requirement for businesses to pay VAT upfront on EU-imports after 29th March 2019 is not set in stone. Indeed, with the Taxation Bill only entering the Committee Stage in Parliament, the text may yet be amended.

Diagram 2: Taxation (cross-border trade) bill 2017-19

“The UK Government has advised that it is looking at methods by which the import VAT will not physically have to be paid over to HMRC but simply accounted for,” explains Bello. “There is a precedent in the EU as the Netherlands had adopted such a method and HMRC would have the ability to implement this as part of UK law without a deal with the EU.”

Should such an arrangement not be put in place, then it is possible for a business to apply for a deferment account with HMRC. “This enables a business to defer payment of the customs duty and import VAT until after the goods have physically moved across the border,” says Bello.

To operate a deferment account, a business must provide a financial guarantee for the customs duty and import VAT. However, subject to a good trading history, HMRC can waive the need to guarantee the import VAT.

This method does not solve all cash flow issues though. “This arrangement only defers import VAT to the 15th of the month after month-end,” explains Bello. “It therefore only reduces the cashflow cost of payment at the order, even though it reduces the at-border administration of payment.”

Be prepared

With much uncertainty remaining around import tax regimes post Brexit, it would be prudent for UK businesses to begin preparing for the future.

“If a business has never moved goods internationally across a customs border before, then it will not be familiar with the various HMRC processes and approvals required to do so,” says Bello. “We would recommend businesses start getting to know the processes, approvals and data requirements now, to ensure their businesses can smoothly transition through the Brexit changes.”

Businesses that trade internationally across the EU and non-EU customs border can expect to have to change the way they account for their UK – EU movements. “Businesses will be required to treat them as an import and export movement,” says Bello. This will require customs declarations to be submitted to customs authorities at both ends of the supply chain.”

All our content is free,

just register below

As we move to a new and improved digital platform all users need to create a new account. This is very simple and should only take a moment.

Please enter the email that you signed up with below. If your email is

connected to a member account, we will send you a reset link.

This website uses cookies and asks for your personal data to enhance your browsing experience. We are committed to protecting your privacy and ensuring your data is handled in compliance with the General Data Protection Regulation (GDPR).