Treasurers are taking advantage of favourable market conditions for debt financing – but which funding routes are most attractive in the current market? And with the ECB beginning to wind down its quantitative easing programme, how long will the current window of opportunity remain open?

Raising finance is a key part of the treasurer’s job – and the good news is that despite potential headwinds such as the ongoing Brexit negotiations, funding conditions continue to be favourable. Published in October, the Q317 Deloitte CFO Survey found that large corporates have easy access to credit, with 80% stating that new credit is somewhat available or easily available and 90% saying that new credit is cheap.

“Markets are extremely strong,” comments Richard King, head of UK&I, Nordic, and Benelux Corporate Banking at Bank of America Merrill Lynch, who focuses primarily on investment grade and implied investment grade businesses. “So our clients currently have an enormous amount of choice when it comes to raising finance.”

Why are markets favourable?

There are a number of reasons for these robust conditions – not least of all the continuing low interest rate environment, despite recent rate increases in the US and the UK. “The expectation is that interest rates will go up over the next 12 to 18 months,” comments King. “But obviously that is against a backdrop of very low levels – so the absolute rates that clients can raise money at are still incredibly competitive.”

Likewise, news that quantitative easing is drawing to a close in Europe has not had a negative impact on the credit environment, says Fenton Burgin, Head of Deloitte’s UK Debt Advisory team. “The ECB is saying that it will gradually unwind quantitative easing this year,” he explains. “But the pace of that unwind is going to be relatively slow, and the ECB will be very focused on making sure it doesn’t stave off the current recovery in GDP in continental Europe.”

Taking advantage of positive conditions

Corporates are making the most of these favourable conditions. King notes that bond issuance in the UK has been “very strong” in the last year, with many large UK corporates taking advantage of benign markets and strong conditions to raise funds from the debt capital markets at competitive levels.

As of mid-December, UK/Ireland debt capital markets volumes across all currencies were US$93.6bn, compared to US$81.4bn in the same period in 2016, according to Dealogic figures. “This speaks to the desire for UK corporates to take advantage of current market conditions and issue early and ahead of potential Brexit uncertainty in 2018/19,” notes King. European corporate bond issuance, meanwhile, was on track for a record year, boosted by the ECB’s decision to begin purchasing corporate bonds directly in March 2016 as part of its quantitative easing programme.

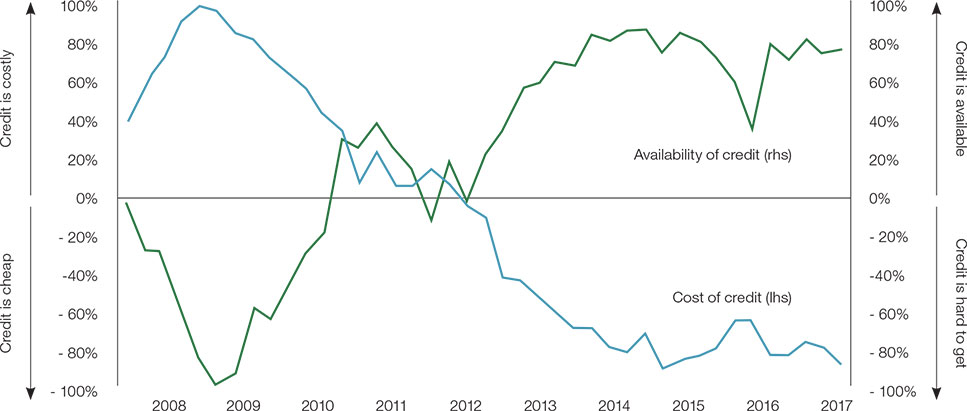

Chart 1: Cost and availability of credit

Net % of CFOs reporting credit is costly and credit is easily available

Source: Deloitte Q317 CFO Survey

Impact of M&A

In some cases, issuance has been driven by M&A activity: high profile deals in 2017 included Reckitt Benckiser’s US$18bn acquisition of Mead Johnson and BAT’s US$49bn purchase of Reynolds American.

Burgin says that conditions are set for corporates to look seriously at M&A this year. “With very high cash balances sitting on corporate balance sheets, there is going to be a lot of pressure from shareholders to grow – and growing organically, when compared to M&A, looks quite a slow proposition,” he notes.

At the same time, Burgin predicts that larger corporates will expand the range of M&A that they are looking at in order to drive shareholder return. This is leading to a growing focus on corporate venturing, whereby corporates invest directly into startup companies. “Essentially, when large corporates are sitting on cash in a low interest rate environment, the return on that cash is low,” says Burgin. “We think there will be an increase in corporates participating in M&A processes where they are essentially looking at investments in the same way that a private equity firm would.”

Pre-emptive action

In other cases, corporates have been pre-emptively raising finance while conditions remain favourable. For example, King says that many of the bank’s clients have been raising funding from the debt capital markets in order to increase their liquidity levels, or to pre-fund debt maturities that are coming up over the next two years.

This may be at least partly driven by a sense that there is a window of opportunity which will not remain open indefinitely. “With interest rate expectations starting to tick up, and likely to do so through 2018 certainly in the US, corporates who need additional liquidity are looking to raise it now, before the rates go up further and while markets are strong,” says King. As a result, he explains, some corporates have been raising more liquidity than they actually need: “Since the financial crisis, corporates have learnt that you can never have too much liquidity. They’ve spent the last few years tidying up their balance sheets, so their leverage levels are very low and they have plenty of debt capacity, but they are also ensuring that they continue to increase their liquidity levels.”

Indeed, George Dessing, Senior Vice President Treasury & Risk at Wolters Kluwer, says that in early 2017 the company refinanced a €750m bond, due to mature in 2018 at approximately 6.4%, with a new €500m ten-year Eurobond at 1.5%. He adds, “this allowed us to use the attractive rate environment to lock in long-term funding.”

John Feeney, Head of Global Corporates at Lloyds, agrees that corporates currently have plenty of access to liquidity, with funding models which provide a certain amount of flexibility in case of future uncertainty. “We don’t see corporates locking themselves into one specific approach,” he says. “It’s much more a case of keeping the appropriate level of flexibility in their funding models and ensuring there’s ample access to liquidity, to be well prepared for the uncertainty that people are expecting.”

Choosing the right funding source

Bank loans and bonds naturally have different characteristics, so corporates have to factor in a number of considerations when deciding which route to choose. King points out that the bank term loan market provides a certain amount of flexibility. A bond is raised for a specific period, with a breakage cost typically payable if a company wishes to change the maturity. A bank loan, meanwhile, has more flexibility when it comes to early repayment.

In practice, King points out that companies are likely to make use of a number of different funding routes. “They may have a revolving credit facility for general liquidity. They may have a term loan to help their short-to-medium term financing, which they can repay depending on cash flow over the next few years. And they may have longer dated bonds for more permanent capital requirements. It’s possible to build a nicely mixed funding profile between those markets.”

Another point that treasurers need to consider is what the right currency mix is for their businesses, particularly in light of the impact of Brexit on sterling rates. “Considering what is the right currency mix of your debt to provide a natural currency hedge for your international business is definitely more important in this different FX world,” comments Karlien Porre, who leads Deloitte’s UK Corporate Treasury Advisory team.

King adds that while treasurers can enter into swaps in order to match the currency they are looking for – for example, by raising financing in the dollar market and then swapping it to euros – they are increasingly trying to match their underlying currency to their financing needs. “They will still do swaps, because some markets will be cheaper than others at any particular time, but they are trying to provide a more natural hedge when they can,” he explains.

Funding options

For corporates looking to raise finance this year, a number of different funding routes are available, from bank loans and bond issuance to direct lending.

Bank borrowing

Deloitte’s Q317 CFO Survey found that 85% of respondents rated bank borrowing as very or somewhat attractive as a source of external funding for UK corporates, whereas corporate debt was rated attractive by 80%. Indeed, the survey shows that bank borrowing has largely been seen as more attractive than bond issuance for the last three years – whereas corporate debt had the edge earlier in the decade.

King says that bank term funding has seen something of a comeback in the bank market over the last 12 months. “After the financial crisis, we went through a phase where clients were mostly doing bridge-to-bonds,” he says. “Meanwhile banks have been more stretched in terms of their own balance sheets over the last few years. That’s now starting to stabilise, and we’re seeing a re-emergence of bank term funding.” King adds that there is no shortage of supply: “Aside from some particularly large M&A financings last year, M&A activity was fairly subdued overall, so there is something of a pent-up demand on the bank side to provide loan financing to clients.”

Again, some corporates are taking advantage of the current window of opportunity by refinancing their existing revolving credit facilities in order to extend their maturity profile. “A lot of refinancing activity was done two or three years ago, and generally the revolving credit facilities have maturities of five years,” King explains. “So a lot of clients are now looking to extend those maturities with two or three years to go – partly because they are being conservative in terms of their debt maturity profile, and partly because they are taking advantage of strong market conditions.”

Bond markets – a global perspective

According to the Deloitte survey, 86% of respondents said that now is a good time to issue corporate bonds. Looking ahead to the coming year, Burgin says key questions for the bond markets will focus on the pace of inflation and how quickly interest rates rise. “Generally, as interest rates rise, bond prices fall to increase yields,” he explains. “In a rising interest rate environment, you will typically see bond yields rise to match that rise in underlying interest rates.”

Consequently, he says, the last six months have seen a pick up in terms of companies using index-linked bonds to shield themselves from the impact of inflation. “We think that trend will continue as people perceive that inflationary pressure might build back into both the UK and European economic landscape,” he adds.

Another factor is the ECB’s plan to wind back its quantitative easing programme. Burgin points out that while bond markets are strongly driven by the QE programme at present, the unwinding process is expected to be gradual – so “that mass of liquidity is going to continue to prop up the European bond markets, making them highly attractive for issuers and keeping rates at close to record lows”.

Conversely, in the US Burgin predicts that yields will continue to move slowly upwards off the back of the US economic recovery and anticipated interest rate rises, which will “inevitably widen out the gap between US and European rates”. He notes that this is a somewhat unusual situation: “Traditionally US markets are lower cost than Europe, so the fact that the ECB is continuing with its quantitative easing programme is actually going to keep the window of cheap finance open in Europe for the next nine to 12 months.”

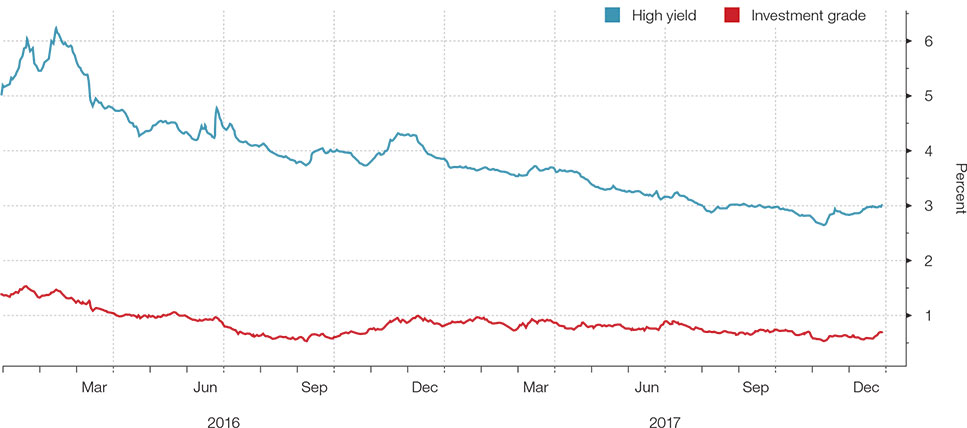

Chart 2: Cheaper borrowing costs

Yields on euro-denominated bonds dropped to record lows in 2017

Source: Bloomberg Barclays index data

Drivers in of funding in Asia

In Asia, meanwhile, different trends and catalysts are coming into play. “Historically, Asian companies are bank funded,” says Gourang Shah, Head of Treasury Services Solutions for Asia Pacific at J.P. Morgan. “So if you want to get a better distribution, it may be important to add bonds to the capital structure. As Asian companies grow, they are getting more exposure to best practice in capital structure and are raising more money.”

At the same time, Shah says that Hong Kong is trying to position itself as a viable option for Asian companies to look at in addition to the UK or New York. “Historically, IT companies in India have tended to raise money in Europe or New York – these locations may come with more liquidity and a better regulatory environment.” More recently, Shah says that the arrival of dim sum bonds has proved to be a good step towards creating a market in Asia for RMB. He adds that progress is also being made in the regulatory environment and in making sure investors feel comfortable with the jurisdiction.

US private placements and beyond

Beyond bank lending and bond issuance, King says that many UK companies have been accessing the US private placement markets. “Clients can raise as much as a billion dollars or more from that market, without having to go to the public markets, at very favourable rates and a range of maturities,” he comments.

Burgin says that he anticipates more direct UK private placements, whereby companies go directly to insurance companies to do a bilateral deal, in contrast to the traditional bank-led private placement route. “We are seeing more and more insurance companies saying they are happy to look at direct deals,” he notes.

Another notable trend is the rise of direct lending, particularly in the mid-market space. Burgin says Europe is moving towards a US model, in which funds and non-bank lenders are the primary source of capital for the mid-market, rather than banks.

“Essentially, there has been a flood of insurance company money, private wealth money and specialist debt investors looking for yield in a low interest rate environment, where gilts and treasuries are yielding low returns,” Burgin explains. “In the US, these lenders provide the bulk of capital into the mid-market – and we think Europe is transitioning rapidly to that sort of model.”

In conclusion, while rising interest rates and the winding down of QE in Europe may affect funding conditions over the course of this year, it’s clear that there are plenty of opportunities currently open to treasurers looking to raise finance. As Porre observes, “Treasurers who are currently looking at their annual or five-year funding plans really have a wide range of options to consider.”

Corporate India’s debt binge

One country that proved especially popular with bond issuers and investors alike in recent times is India. From March 2016 to March 2017 corporate bond sales in India were valued at US$51.5bn – a 40% increase from the previous year – according to data from Prime Database.

Driving this trend has been Prime Minister Modi’s progressive economic reform, which has opened the domestic market and attracted more investors, especially from overseas, to buy Indian corporate debt. The increasing demand for this debt has seen spreads tighten, making bonds a cheaper source of financing for corporates able to tap the market.

The attractive 7% average yields on India corporate bonds saw international investors flood the market. By the end of July, foreign ownership of corporate debt surpassed 92% of the US$38.1bn quota permitted by the government. This led regulators to suspend issuances of offshore rupee-denominated bonds to stem the inflow for a short-time.

It seems, however, that if the demand is their corporates will continue to issue. This is especially true given that the Indian banking sector is currently facing a multitude of issues limiting its ability to lend to corporates.

Panda bonds on the rise?

Another exciting bond market in Asia is the panda Bond market – RMB denominated bonds issued by international companies or sovereigns in China. After the first Panda bonds were issued in October 2005 by the IFC and the Asian Development Bank, the nascent market failed to live up to the initial hype with very few foreign corporates issuing bonds.

In more recent years interest has grown, especially because of some high-profile issuances from companies like Daimler. Yet, despite this the panda bond market still only accounts for a tiny fraction of China’s US$3bn onshore debt market, meaning that there is still plenty of room for it to grow.

By the end of August 2017, 42 panda bond issuers had entered the Chinese interbank market, including international development institutions, sovereign governments, financial institutions, and non-financial enterprises, from North America, Europe and Hong Kong, according to the International Capital Market Association (ICMA). This accounted for total of RMB11bn panda bonds through 57 transactions.

The ICMA believe that panda bonds may become increasingly attractive to corporate borrowers in the coming years because:

Funding onshore operations:

Raising RMB directly onshore can simplify cash flow operations and reduce potential currency risk to match their RMB funding needs for foreign corporates with operations in China.

Investor diversification:

The large Chinese bond market investor base presents a significant opportunity to expand the base of creditors.

Liquidity:

The onshore bond market is perceived to be generally more liquid than the offshore dim sum market.

Marketing considerations:

Issuance of panda bonds by foreign institutions helps domestic market participants to develop a better understanding of how these institutions operate, builds trust between the two sides, and ultimately fosters the sustainable and efficient operation of foreign institutions in China.

Global funding:

The Chinese onshore bond market, like other international markets, may present an opportunity for foreign issuers to obtain funding in their primary currency (usually USD, EUR or GBP) at attractive rates by issuing in RMB and entering into a cross-currency swap for their primary currency.

Market innovation:

The issue of some panda bonds to date has been motivated at least in part by a desire to be one of the first to market with an innovative transaction.

Continued opportunity

As we move into 2018, the outlook for corporate funding remains positive. Indeed, no matter what part of the world the company is looking at, there are lots of opportunity out there to raise reasonably priced debt.

For corporate treasurers, the advice is to begin reviewing their options now and perhaps take advantage of the favourable conditions whilst they exist. Indeed, Patrick Tai, Finance Director, CNOOC and Shell Petrochemicals Company Limited, who features in this editions Corporate View and whom has built a career on raising finance to fund some of the world’s largest petrochemical projects says: “One issue that I see many companies have is that they only focus on debt when they need it. We work on this even when times are good so that we can call on it when we need to.”

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.