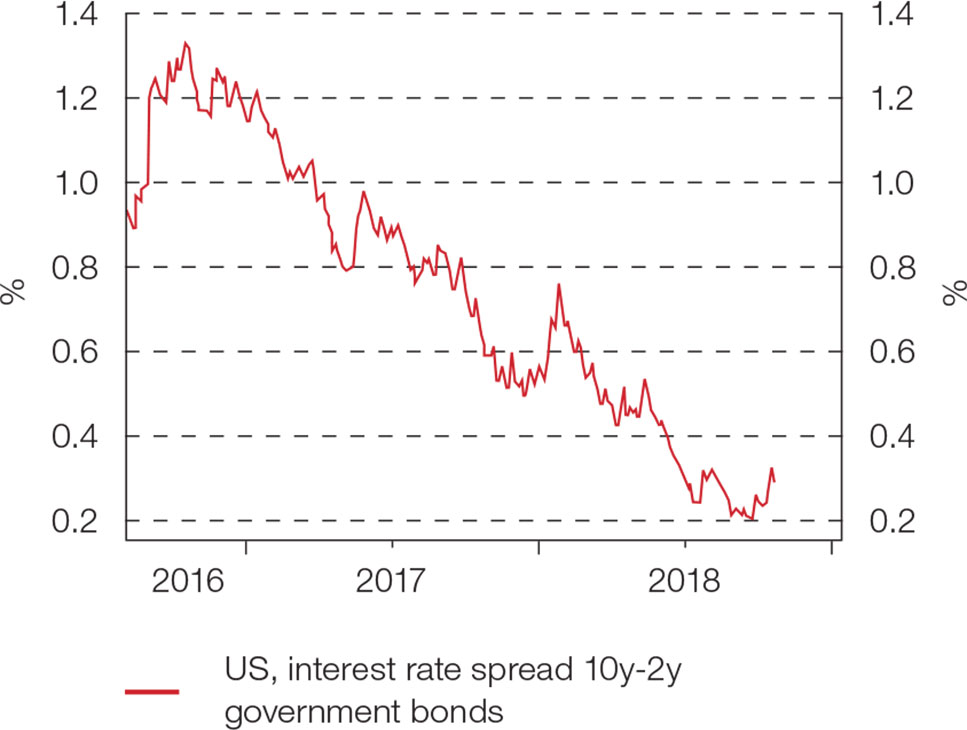

The US yield curve has been flattening for a long period of time. The difference between interest rates on two-year and ten-year US government bonds was only 20 basis points in late September and had risen to 30 basis points by mid-October. This is generally considered to be a logical development, as the market has been assuming US economic growth will decline next year as the effect of fiscal stimulus fades and higher interest rates start to bite against a backdrop of soaring debts and a strengthening of the dollar exchange rate. Given this outlook, inflation will come under downward pressure next year, forcing the Fed to stop hiking rates or to start cutting them.

However, it is also possible to have a different view. Robust US economic data has emerged lately, alongside very strong wage growth, and the outlook on both these fronts remains positive. In addition, oil prices have risen and higher import tariffs will drive up prices of imported goods. This could easily lead to higher inflation data before long. This could give rise to higher wage demands, higher consumption growth and surprisingly strong economic growth.

All that begs the question: does the flattening yield curve reflect bond buyer sentiment that they do not see interest rates rising to much higher levels in the future? Or is the flattening caused by foreign capital that was attracted by higher interest rates, by central banks purchasing massive amounts of long-term bonds, and by pension funds and insurers receiving fiscal incentives to purchase bonds on a large scale?

At the moment, the recent upward outbreak in terms of interest rates seems to have been caused by a combination of factors: improved US economic data; rapidly deteriorating supply/demand ratios due to much higher US government deficits; and a shift from QE to QT by the biggest central banks since October.

Chart 1: Yield curve US

Source: Thomson Reuters Datastream/ECR Research

However, the recent bout of surprisingly strong economic growth data could easily be a temporary phenomenon. In addition, higher interest rates would impact the emerging markets, with Europe being affected indirectly. They could also end up undermining themselves because credit spreads would (ultimately) rise rapidly and lead to share prices falling. That would likely decelerate the US economy. In addition, investors would purchase US government bonds as a safe haven.

In other words, interest rates could rise for a short period of time, but the tide would turn fairly soon afterwards. The direction and strength of US wage increases and inflation going forwards is therefore of crucial importance. The more wages and inflation rise, the more powerful the upward pressure on US interest rates will be.

More specifically, we anticipate the following scenarios for rates and market prices going forwards.

US interest rates

We believe that, for the time being, the US economy will continue to grow at a higher pace than potential growth. This will soon lead to additional wage increases and higher inflation. Higher import tariffs will also contribute towards inflationary pressure.

On that basis, we believe upward pressure on US interest rates will, on balance, intensify considerably over the next couple of months and that the Fed will raise its short-term interest rates in December, however we do not believe interest rates will climb in a straight line. We expect the dollar to strengthen before long, resulting in mounting problems for the emerging markets. In such an environment, US credit spreads would rise and share prices would decline.

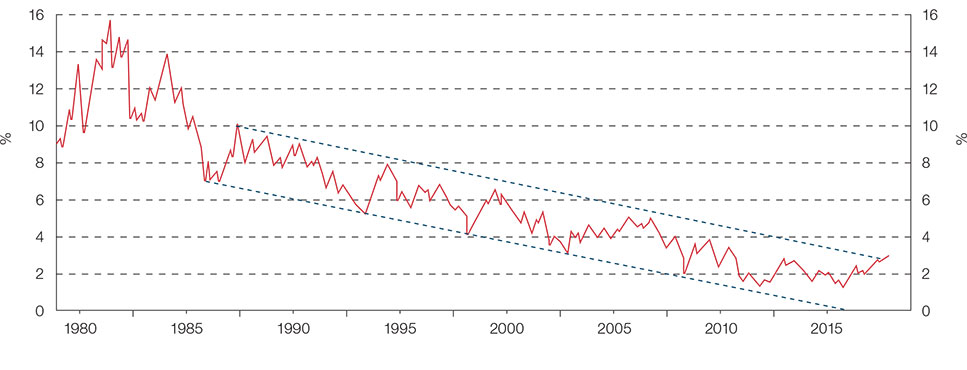

Chart 2: US ten-year treasury note yield

Source: Thomson Reuters Datastream/ECR Research

The S&P 500 index could fairly easily slide down to approximately 2,500 (at the time of writing the S&P 500 traded around 2,760). This would probably be enough for the Fed to pause the process of rate hikes. Long-term interest rates would then probably decline considerably for a brief period of time. Lower interest rates would subsequently boost asset prices and drive up economic growth.

We see the Fed pursuing a monetary policy that will allow growth to remain high enough for inflation to rise. That suggests to us that, following the hike in short-term interest rates in December, the Fed will wait for about two quarters before resuming its hikes and that short-term interest rates will ultimately be at around 4.5% by 2020.

Under this scenario, we believe interest rates on ten-year US government bonds will continue to rise to 3.35-3.5%, after which they will fall back to 2.75-3%. In the ensuing period, the long-term uptrend will continue. As a result, we expect ten-year interest rates to be at approximately 5% by 2020.

European interest rates

When we consider Europe we see rising tensions within the EMU as a result of the Italian government budget as perhaps the most important element impacting the outlook for the region. Rome assumes its budget deficit will be 2.4% of GDP in 2019; with the deficit expected to slowly decline on the expectation of higher economic growth in Italy. Many economists, however, doubt Italy will be able to achieve such an outcome. That lack of confidence in the near-term outlook for Italy suggests to us that, for the time being, a flight to German and Dutch bonds will become increasingly evident.

Yet German and Dutch government bond yields will also be influenced by interest rate developments in the US. Moreover, the above-mentioned negative developments will be partially offset by a weaker euro and the associated improved outlook for exports.

Under such a scenario, we believe interest rates on ten-year German government bonds will continue to rise to approximately 0.65%, after which they will decline to approximately 0.35% before the long-term uptrend continues. As a result, we expect ten-year interest rates to be above 1% in the course of 2019, and just below 2% by 2020. The ECB will initially hike its short-term interest rates by 0.25 percentage points every two quarters, after which it will hike its rates by 0.25 percentage points every quarter.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.