It’s the early 1970s and the US economy is in a mess. The boom years of the 1960s are fading fast; the New York Stock Exchange (NYSE) falls by 40% in the space of just 18 months; economic growth is weakening and unemployment about to hit double digits.

If that is not bad enough, there is also the problem of spiralling inflation. The US Federal Reserve, in a relentless pursuit of full employment, allows the rate of inflation to rise to over 10% by the mid-1970s from a base of just 3-4% the decade previous. Cash preservation therefore poses an enormous challenge for businesses in the US during this period; a challenge made particularly acute by the fact that the interest that banks are allowed to pay to their customers has a fixed limit.

An industry is born

It was against this backdrop that the first money market funds were introduced. The first MMF in the US was established in 1971 by Bruce Bent and Henry Brown. It was created, chiefly, for the purpose of side-stepping a federal banking law, Regulation Q, a rule introduced during the Great Depression which limited the rate of interest banks were permitted pay to depositors. Regulation Q had not been as much of an issue for depositors when inflation was around 3-4% as it was for much of the 1960s. When in the 1970s it began to surge to record highs, however, investors began to seek out alternatives to traditional deposit accounts.

In the commercial paper market, investors bypass banks altogether by lending directly to borrowers. The first MMFs were established when brokers and other financial institutions began to pool investors’ funds into the purchase of commercial paper and other short-term securities. MMFs could not guarantee the same level of safety as banks with FDIC-insured deposits, but, by residing outside of the banking sector – and so beyond the purview of banking regulators – they were able to attract an increasing number of investors through the offer of higher rates.

Despite the legal classification, MMFs like the Reserve Primary Fund, shared some traits in common with regular corporate bank accounts. To begin with, security and liquidity were the top priorities. From day one, the purpose was to provide investors with easily accessible, cash equivalent assets which meant restricting portfolios to short-term securities representing very high-quality, liquid, debt and monetary instruments. And, by matching the term structure of the portfolios assets with the term structure of its liabilities, funds were able to guarantee investors that their money would be there to withdraw as and when they needed it.

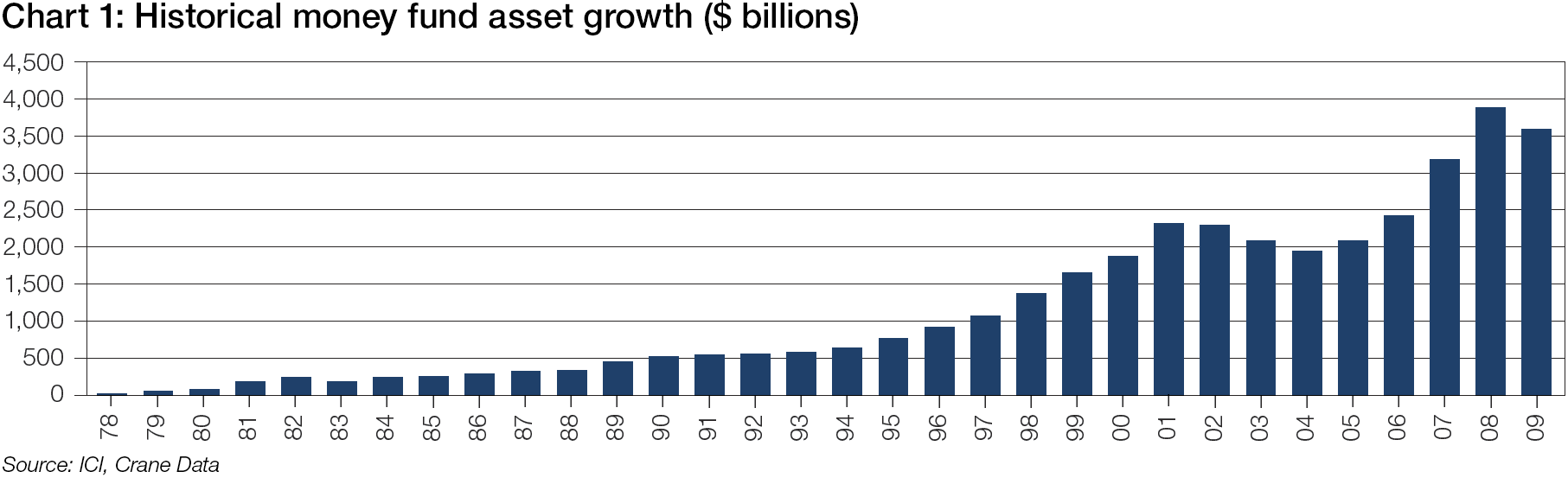

In the early 1980s, Federal Reserve Chairman Paul Volker – who many years later drafted as part of the Dodd-Frank regulation the eponymous ‘Volker Rule’ – liberated the banks by revoking the limit on interest payments to customers. Investors quickly began to flee MMFs, pushing their funds into new, FDIC-insured high interest savings accounts set up by the banks. As Chart 1 illustrates, MMFs took a big hit from the change, losing close to 25% of their assets in the space of just a few months. Clearly, funds needed to find another way to compete against the banks.

Chart 1: Historical money fund asset growth ($ billions)

Source: ICI, Crane Data

The solution for the MMF industry was to persuade the Securities and Exchange Commission (SEC) to allow them to adopt a new accounting treatment that made the value of their portfolios appear more stable than it really was. A constant net asset value (CNAV) which prices to two decimal places, helped make the funds a more attractive investment. This was particularly the case for corporates, the biggest MMF investors, who hold large sums of cash on a short-term basis and want to avoid dramatic fluctuations in value. But, as we will see, the special accounting treatment MMFs were permitted to use would, later on, become a target for regulators in the wake of the 2008 financial crisis.

Banks enter the game

Throughout the subsequent decade, the volume of assets under management in the MMF industry continued to grow and, by the late 1980s and early 1990s, banks that had been casting an envious eye decided that they too wanted a piece of the action. The problem for banks, however, was that in the US they were still prohibited under the provisions of the Glass-Steagall Act 1933 from combining their banking operations with a business in securities. If a bank wanted to offer a money fund, there was only one legal means for it to do so: it had to outsource either the administration or the distribution of the fund.

New, third-party organisations quickly began to emerge to perform these activities on the banks’ behalf. One of the largest of these, Concord Financial, was the company at which Ed Baldry, now the CEO in EMEA at ICD-Portal, began his career. “Our job was to go to these banks and, in addition to providing the administration, distribution or transfer agency functions, educate them around selling their institutional funds” explains Baldry. In fact, the large Wall Street banks – Citi and Bank of America, for instance – that entered the money market fund business at this time experienced little difficulty in finding clients. Banks, after all, were also the principal source of finance for many corporates and this gave them a clear advantage over non-bank funds. “For corporate investors I think that it was a fairly straightforward decision,” says Baldry. “‘Do I give my money to a bank or do I give it to another fund that has never done anything for me?’.”

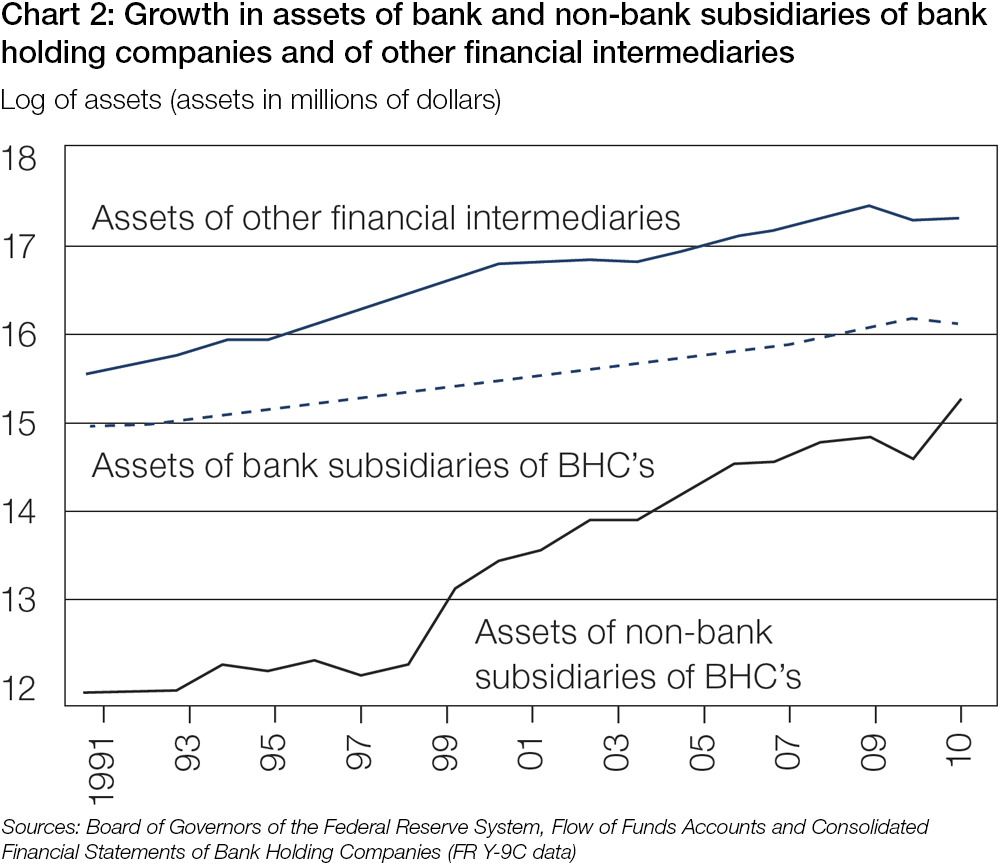

Unsurprisingly then, the bank share of the MMF business continued, with the help of intermediaries, to expand throughout the 1990s. Finally, after the Graam-Leach-Biley Act 1999 swept away the final remnants of Glass-Steagall, banking institutions, now sanctioned to own and control both bank and non-bank financial entities, began to assume a more direct involvement in the industry. In the years that followed, the assets under the management of non-bank subsidiaries of bank holding companies rose sharply (see Chart 2) and continued to grow right up until the recent financial crisis.

Chart 2: Growth in assets of bank and non-bank subsidiaries of bank holding companies and of other financial intermediaries

Log of assets (assets in millions of dollars)

Sources: Board of Governors of the Federal Reserve System, Flow of Funds Accounts and Consolidated Financial Statements of Bank Holding Companies (FR Y-9C data)

Breaking the buck

Prior to the 2008 financial crisis only one relatively diminutive fund had officially ‘broken the buck’; a colloquial expression used for when the capital price of a fund breaches tolerance levels and thus forces the fund to restate the actual share price below 1.00. But this fact only made the events that came to pass in the autumn of 2008 seem all the more shocking and catastrophic.

On Tuesday, 16th September 2008, the US’ oldest MMF, the Reserve Primary Fund, began to inform investors that they would lose money. The Reserve had made a decision to own a huge amount of Lehman Brothers commercial paper. After these securities became, in September 2008, worth less than the paper they were written on, the fund was left with no choice but to revalue shares. Instead of each share being valued at $1 for every dollar invested, the fund was forced to tell customers that shares were only worth 97 cents. It was the first time in 14 years that one of these seemingly super-safe investment vehicles had incurred losses and news of the impending $64.8 billion firesale caused shockwaves in the financial world. Suddenly MMF investors became incredibly anxious and, as they sought to redeem their holdings, a large number of funds were forced to liquidate assets or impose limits on redemptions. Investor conviction that MMFs were no riskier than regular bank accounts now appeared to be gone for good. “That really changed the landscape forever,” remarks Baldry.

In the space of just a few days following the Lehman Brother’s default, redemptions across the MMF industry had reached an astonishing $300 billion. The speed and scale of the exodus was so severe that the US government was left with little choice but to intervene by providing unlimited insurance to all money market fund depositors. A number of other funds in Europe were also underwritten by their respective governments.

Regulatory backlash

The story of the MMF industry – particularly in the US – is closely entwined, if not inseparable, from the evolution of financial regulation going right back to the Great Depression. Now, in the wake of a new global financial crisis, fresh regulatory proposals seem likely to drive change every bit as momentous as the industry changes seen in the past.

Government intervention may have brought a halt to the market panic and even saved the industry from probable implosion, but political leaders across the globe have been working ever since to ensure that funds are able to stand on their own feet in a future crisis. In the US, the SEC’s first move was to introduce changes to Rule 2a-7 that established stricter quality and liquidity requirements on funds. But more proposals were soon to follow.

In June 2013, the SEC offered two alternatives for further reform. Under the first option, institutional or ‘prime’ MMFs would be required to transact at a floating NAV, rather using amortised cost to value their portfolio securities. The second course of action suggested that MMFs could continue to use their accounting treatment of preference, but would be required to impose liquidity fees and redemption gates in times of market stress. In Europe, meanwhile, the European Commission (EC) has been weighing up the introduction of similar accounting proposals in tandem with compulsory capital buffers set at 3%.

The suggested reforms have resulted in much public debate and, in the case of the NAV proposal, strong opposition from market lobbyists. Corporate end-users, in particular, have raised concerns regarding the impact that an industry-wide switch to VNAV (variable net asset value) might have upon their investment strategies. Large numbers of corporate treasurers, both in the US and Europe, prefer the simplicity of the tax and accounting treatment under CNAV, and industry bodies have repeatedly cited empirical studies that suggest the form of accounting treatment will make little material difference to the behaviour of MMF investors in crisis scenarios.

No final decision has yet been made in either jurisdiction on the way to proceed. However, industry experts expect something to be agreed by the respective regulatory and legislative bodies within the next 12 months. Should the regulators choose to disregard industry concerns and press ahead with a mandatory switch to VNAV it is likely that we will see a seismic shift in investor preferences, with 20-30% moving away from MMFs into other investment vehicles according to estimates by the credit ratings agency Moody’s. It might even be a greater exodus than that. In the Association of Financial Professionals (AFP) 2013 liquidity survey, 65% of respondents indicated their intention to reduce or sell off their MMF holdings entirely if CNAV funds are prohibited.

Consolidation

These are uncertain times then for the $2.7 trillion dollar industry which has become a mainstay of the financial world. For fund managers, the challenge of managing the prospect of changes to the way the industry is regulated has been compounded by the pressure of ultra-low interest rates on both sides of the Atlantic. The twin pressures of rates and regulation appear to driving the industry full circle.

Deregulation at the turn of the millennium helped banks assume greater involvement in the industry by allowing them, for the first time, to establish subsidiaries in the securities business. The number of banks in the MMF business multiplied in the wake of that change, but now the trend appears to be going into reverse. Consolidation is now the name of the game.

In the past year, we have seen Lloyds Bank announce the sale of SWIP to Aberdeen Asset Management, Barclays selling their fund BlackRock, and RBS offloading theirs on Goldman Sachs. Once again the winds of change are sweeping through the industry; only this time they are blowing in a different direction.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.