Short-duration strategy: tailoring your cash portfolio for higher yields

Published: Sep 2012

Record low central bank rates are driving down the available yields from money market instruments. Regulation is compounding matters by suppressing yields and potentially limiting the pool of investments available to corporate treasurers. With these structural changes in the financial industry reshaping best practice cash management, how can treasury professionals look to optimise their cash portfolio and achieve higher yields, while being mindful of risk? A short-duration strategy within a separately managed account could be the answer, according to BNY Mellon Asset Management.

While the return on cash may be lower on the treasurer’s priority list today than minimising investment risk, this does not mean that the desire for yield has disappeared entirely. Nevertheless, the high-quality, easy access liquidity provided by money market funds (MMFs) and bank deposits has superseded the yield requirement for many companies of late. But by limiting their cash investments to these traditional tools, treasurers may be foregoing opportunities for higher yields – or even accepting negative returns. This approach may also preclude a corporate from achieving greater control and improved cost efficiencies over their cash investment portfolio.

So what is the alternative? A short-duration strategy within a separately managed account (SMA) can, according to Laurie Carroll, Director, BNY Asset Management, provide an attractive option for those investors in search of higher yields (than those currently offered by fixed net asset value (NAV) instruments). In order to fully embrace this tailored portfolio approach however corporates would be well advised to ensure they have a good, strategic hold over their available liquidity from the outset.

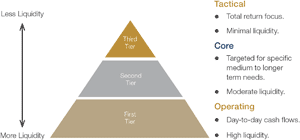

BNY Mellon recommends a three-tier approach, segmenting cash into operating, core and strategic balances. “We provide solutions appropriate to the three different tiers of cash typically held by clients,” says Carroll.

The first tier consists of operating cash which is required for daily cash flows. This needs to be highly liquid and money market funds or short-term separately managed accounts are the most appropriate means of providing this.

The second tier is the company’s core cash. This is allocated to particular medium and long-term requirements and therefore needs moderate liquidity. “We believe that treasurers may be missing an opportunity to pick up additional yield here,” continues Carroll. “We suggest using enhanced cash or ultra short separately managed accounts for the second tier.”

The third tier is set aside for longer-term liabilities (such as construction costs or capital calls) and therefore less liquidity is needed and higher yields and returns are expected. “We can provide this with one-three or one-five year maturity portfolios or matched funding separate accounts.”

Separately managed accounts can be used for all three tiers of cash, but may be of particular benefit in the second and third tiers, given their longer time horizon and higher total return objective.

Diagram 1: Separate account management

Sources of performance

For those corporate investors who have the flexibility to consider a broader scope of relative-value opportunities across slightly extended time horizons, a bespoke SMA can be constructed to capitalise on a wider range of strategies, sectors, and securities than those available through constant NAV vehicles. “Yes, companies need liquidity – whether that be money market funds, bank deposits or whatever you use for your daily/weekly cash needs – but in this environment where there is little yield, companies should also be looking to generate some excess return, for example by placing at least some of their money further out along the yield curve,” explains Carroll.

BNY Mellon Cash Investment Strategies (CIS) Team uses an active investment management approach to help clients generate consistent, low volatility returns. This is the team’s aim whatever the interest rate or macroeconomic environment.

The four strategies which the CIS team employs to do this are:

Increased maturity/duration.

Credit.

Liquidity.

Yield-curve positioning.

So how does each of these work?

Increased maturity/duration

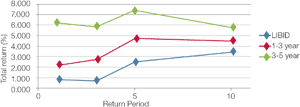

By modestly increasing the average maturity or duration of their portfolio, companies should be able to take advantage of the normally positive slope of the yield curve. In other words, by moving out slightly further along the yield curve, returns should typically be enhanced, as the chart below illustrates.

Nevertheless, corporates should be aware that there are several different types of yield curve. “The key point here,” says Carroll, “is that the yield curve is normally positive. Sometimes it isn’t. Furthermore, by extending the maturity, corporates will have their cash locked in for longer, which will impact their liquidity and could potentially increase volatility.”

This is where the three tiers of cash come into their own, as they essentially impose maturity limits on a segment by segment basis. “The team of experts at BNY Mellon will also work with companies to ensure that they have sufficient operating capital to meet any immediate or emergency liquidity requirements. In other words, we keep a very close eye on any risks so that clients can comfortably extend the average maturity of their portfolio in search of additional yield.”

Chart 1: Sterling Gilt and LIBID Total Returns

Source: Bank of America Merrill Lynch, through 30th June 2012

Credit

Looking for undervalued securities in the market is another way of increasing the yield potential of a portfolio. But this requires skill, expertise and resources. “We have a team of credit analysts who establish a ratings trend for each securities issue. An in-house assessment as to the likelihood of the issue’s current rating changing – whether it be an upgrade or a downgrade – is undertaken by the team. Our portfolio managers then combine this trend outlook with current spread levels to help inform their buy and sell decisions,” says Carroll.

Increasing the credit risk of investments can also enhance yield. For example, corporate securities tend to offer potentially higher yields than government securities since the credit quality of corporate securities is not normally as high as their government counterparts. This outperformance is particularly marked in the current macroeconomic environment, but has been noted across a variety of market cycles, as illustrated in the table opposite.

Case study

Short-duration strategy

Laurie Carroll

Director

In this interview we look at the benefits of a short-duration strategy as well as best practice in managing cash investments today.

What does a short-duration strategy within a separately managed account offer to corporates?

It’s a question of layering the cash that the corporate doesn’t need overnight – so that duration becomes part of the strategy. This is not a question of hedging; this is the investment management of a pool of ‘near cash’ whose average maturity or duration is not as short as a bank deposit or a money market fund. Realistically, that’s anywhere from a six month to a two-year duration.

At BNY Mellon Asset Management, we believe that this kind of approach should really form part of a client’s three to five year strategy. Naturally, the majority of a client’s cash is going to be very short-term, but you can never tell where interest rates or credit quality are going. As such, it is the investor’s duty to seek diversification of strategies today.

Just look at the Eurozone where deposits and MMF returns are very close to zero. Some corporates are keeping all their eggs in those very low-rate ‘baskets’ because they like the security and liquidity. But that does not necessarily constitute optimal cash management. Put simply, since no-one can forecast interest rates with any certainty, we feel that clients should diversify their sources of performance, even in the very front end of the yield curve.

How does the short-duration strategy look to enhance yields?

Within our short-duration strategy we have four tools that can be used to add value. As outlined, we use average maturity and duration; credit quality; liquidity – ie balancing how much the client needs overnight versus what can be put out longer; and then we look at yield curve positioning. It’s interesting that all of these tools are used to some degree in managing money market funds. Given the restrictions placed on MMFs however (take a AAA rated fund with a maximum WAM of 60 days), they can only leverage these tools to a small degree.

Moreover, those companies who cannot see beyond investing solely in MMFs or bank deposits are not embracing best practice cash management. Understandably, treasurers are not used to thinking about cash diversification in a way that uses longer average maturity and longer duration. They may therefore be hesitant that, by going in search of yield, they are putting company money at risk. But leaving money to earn zero or negative yields ultimately means losing out on both money (time value) and opportunity.

Why is this strategy a key part of BNY Mellon Asset Management’s offering?

Providing a more strategic approach for our corporate investors really differentiates us from those banks that are just offering money market funds. More importantly, it allows us to open up a full spectrum of instruments to our investors. And we’re not just talking about commercial paper, bank deposits or money market funds (MMFs remain a key part of our offering) – we’re talking about the shorter maturity part of the bond market. That in itself is extremely powerful and shows BNY Mellon’s commitment to this space.

Sterling corporates versus gilt returns

Three year

Five year

Ten year

Gilts

2.719

4.748

4.503

Corporates

5.879

4.961

4.963

Outperformance

3.160

0.213

0.460

Source: Bank of America Merrill Lynch, through 30th June 2012

Liquidity

Although many corporates would be wary of altering the liquidity of their portfolio too much, it is possible to make strategic tweaks. Says Carroll: “Take two securities that are to all intents and purposes identical – except for their liquidity. The less liquid of the two will tend to offer a higher yield. Shrewd allocations to certain securities or even sectors which are less liquid can potentially generate incrementally higher returns.” With the expertise available at BNY Mellon Asset Management, this tweaking should have minimal impact on the portfolio’s overall liquidity.

Yield curve positioning

Yield curves come in three primary shapes: inverted, flat or normal. Critical factors affecting the shape of the yield curve include:

Expected changes in monetary policy.

The current outlook for future inflation.

Currency flows driven by the trade balance.

The future path of interest rates.

There are two main ways that BNY Mellon’s CIS team attempts to realise above-average yields by ‘riding the yield curve’. Both relate to the spacing of maturities:

Bullet strategy. This is where a portfolio of securities with maturity dates concentrated at one point on the yield curve (eg ten years) is built. This maturity date is not necessarily the same as the time period for which the funds are available for investment.

Barbell strategy. This is where a portfolio of securities with maturity dates set at two extremes on the yield curve (eg five and 20 years) is built.

These techniques are best suited to the front-end of the yield curve, where a high degree of slope and curvature is typically found.

Balancing risk and return

By going in search of additional yield, corporates will inevitably encounter risks such as interest rate risk; liquidity risk; credit/downgrade risk and spread risk. At BNY Mellon Asset Management, however, these potential risks are factored into a holistic risk-reward framework and portfolio strategies are constructed with the aim of meeting clients’ specific investment goals. Separate account management is a key step towards achieving these.

The benefits of SMAs include:

A portfolio objective specific to the company’s risk tolerances and total return objectives.

Guidelines and strategy can be easily revised based on the company’s changing goals.

A separate investment management contract.

Custom guidelines structured to meet a company’s requirements for quality, liquidity and duration.

Investment management is not impacted by the flows of other investors, or controlled by regulatory changes.

The availability of customised reporting.

Finally, the use of a short-duration strategy within an SMA can be an extremely powerful tool for those companies seeking improved returns across a broad spectrum of cash activities.

BNY Mellon Asset Management

BNY Mellon Asset Management is the global asset management arm of BNY Mellon, one of the world’s major financial services groups with operations in 36 countries serving more than 100 markets.

At BNY Mellon Asset Management, our goal is to build and manage investment strategies that address the ever changing needs of our clients. With over $1.3 trillion in assets under management, as at 30 June 2012. We are rapidly becoming the trusted asset manager of choice for institutional investors globally.

BNY Mellon Cash Investment Strategies delivers customised and comprehensive investment solutions to meet the needs of institutional investors. Its consolidated credit research, investment management, and client service functions combine historic strengths and pioneering work in money market funds with separately managed short-duration, stable value and bond index strategies, giving BNY Mellon Cash Investment Strategies clients access to more than 50 years of investment experience

Contact details:

Marcus Littler

Managing Director, Head of Institutional Liquidity Sales

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.