Raising the standards of Chinese money market funds

Published: Jan 2018

The Chinese Securities Regulatory Commission recently published a set of new rules designed to strengthen the Chinese money fund industry. Its aim is to create a stable foundation for future growth. Aidan Shevlin, Managing Director, Head of Asia Pacific Liquidity Fund Management at J.P. Morgan Asset Management, outlines what this all means for investors.

Aidan Shevlin

Managing Director, Head of Asia Pacific Liquidity Fund Management

China’s money market fund industry has grown exponentially in a relatively short space of time. Today, total assets under management (AUM) stand at around RMB6.5trn1. Because of this, the Chinese government has marked it as ‘systemically important’ to the Chinese economy.

As a result of its status, the regulators have begun to pay more attention to money market funds. Recently, the Chinese Securities Regulatory Commission (CSRC) brought in a host of new measures. These have been designed to strengthen the money fund industry by more closely aligning the rules that govern it with international standards, forcing some funds to de-risk. It is a move that Shevlin calls “a hugely positive step for the money fund industry in China”.

A unique ecosystem

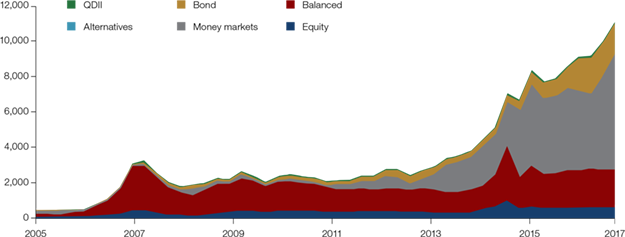

A large part of the growth in China’s money fund industry has come from retail investors. After years of being limited to investing in unattractive Central Bank controlled time deposits, many were buoyed by the chance to invest in different and higher returning products. Money market funds (MMFs) have proven to be especially attractive. Today, they account for roughly 60%2 of all assets invested in mutual funds in China. MMFs are also continuing to grow at an impressive compound annual growth rate (CAGR) of 70%3 over the past five years.

“The popularity of MMFs in China is quite unique,” says Shevlin. “There are various reasons that the market has developed in this way. When compared with returns on other investment options such as equities and fixed income, which have been quite volatile, money markets have posted fairly solid returns in China, with rates averaging between 4% to 7%.” The influence of Alibaba’s innovative Yu’E Bao fund4, the world’s largest with RMB1.4trn AUM, also cannot be overlooked, he adds.

Institutional investors have also taken advantage of the new range of investment opportunities. “There is a lot of corporate cash in China that needs a home,” notes Shevlin. “With corporates wanting to make sure it is invested in diversified and safe products, MMFs, especially AAA-rated funds, have become increasingly attractive investment vehicles.”

Emerging risks

Robust growth of MMFs in China has created plenty of competition. There are now over 400 funds5, mainly retail focussed, competing for investors cash. This level of competition has brought with it a less than welcomed phenomenon. “In China, local investors primarily focus on yield over security and liquidity,” explains Shevlin. “As a result, fund managers in China have increasingly sought to offer investors higher returns to differentiate themselves.” This is driving some fund managers to adopt very aggressive investment strategies. Many funds have high duration profiles and have also increasingly been buying less liquid bonds, which can be difficult to sell at times of stress.

Moreover, some funds have been looking lower down the credit quality spectrum in their hunt for yield. This is a risky strategy, given the cash flow problems of weaker issuers and the increasing number of corporate defaults in China.

Finally, some fund managers have also been using leverage via repurchase agreements (repos) – where securities are lent out and the cash received from this reinvested – to boost overall returns on the fund. In a stable interest rate environment, managing a fund in this way can significantly boost its overall returns. Issues arise if there is unexpected volatility, especially at the short end of the curve, which can reduce returns, pushing yields lower, triggering outflows and creating significant issues for the fund.

“The authorities are very aware of these risks. They realise that if a fund was to ‘break the buck’, it could create a contagion effect, potentially impacting confidence in the entire financial system and broader Chinese economy,” says Shevlin. “Because of the importance of money market funds and potential systemic risk, the regulators have realised that they need to install safeguards and curb the instincts of retail fund managers to boost yields without considering the risks involved.”

Tighter oversight

The key objectives of the latest tranche of rules brought in by the CSRC in September last year are to create a stronger link between risk and return. They impose tighter limits to reduce concentration risk, strengthen rules that limit a fund’s exposures to any single borrower, and reduce investments in assets with lower credit ratings.

Under the new regime, funds cannot hold assets (such as cash deposits or bonds) from a single bank if that holding represents more than 10% of that bank’s net assets. Also, rules further state that funds may hold a maximum of 2% of its assets from a single institution with credit ratings below AAA and cumulatively a maximum of 10% in such lower rated issuers.

In addition, the CSRC has clamped down on money funds’ use of illiquid assets. It has clearly defined what it considers illiquid and liquid assets, and states that funds must hold at least 10% of its assets in liquid instruments and a maximum of 10% in illiquid assets.

Finally, the CSRC is attempting to limit investor concentration. Shevlin explains that in China, funds with only one or two dominant investors create substantial liquidity risks: “If these investors were to redeem their investments, for any reason, it would have a significantly detrimental impact on the integrity of that fund that may send shockwaves through the rest of the market.” As a result, he says the CSRC is forcing funds with high investor concentration to shift, to hold even higher levels of liquidity and substantially lower durations. Meanwhile, new money market funds with high investor concentration cannot use amortised cost accounting.

Investor impact

The bad news for retail investors is that because of the new CSRC’s rules, the days of very high returns on their investments are over, says Shevlin. “The rules have brought down the average range of yields within retail funds, creating a lot less variability and a lot less opportunity for fund managers to manipulate the yield to look attractive.” This he believes “makes the industry as a whole more stable”.

On the institutional side, there is less impact. Corporates in China largely invest in AAA-rated funds which already abide by tighter rules than those outlined by the CSRC. “That being said, corporates are largely positive about the broader impact these changes will have on the money fund industry,” says Shevlin. “They are also encouraged that it is being more closely aligned with how the industry works in other developed markets. This gives them the comfort to increase their usage of these products and diversify their investment portfolio in China.”

In addition to the CSRC’s rules, Shevlin also comments on the Chinese central bank’s rules issued in November which prohibit asset managers from promising investors a guaranteed rate of return. “This is more good news for the financial development in China,” he says. “It dispels a myth that all financial investments are guaranteed by the government; they are not. Investors, particularly domestic corporates who are growing in sophistication and aiming to operate in similar ways to their Western peers, will need to do more research into their investment options. This too is pushing the market in the right direction, aligning it more with international standards.”

Broader context

Overall, Shevlin sees the new rules as a positive step for the industry, enabling the money fund industry in China to expand in a controlled and secure manner. “The industry is still growing and there is lots of potential for fund managers like ourselves, so you don’t want an event occurring that will disrupt this growth or destroy the industry,” he says. “More broadly, these new rules closely align with China’s economic ambitions over the coming five years. These focus on quality and controlled growth as the country continues to pivot away from a low cost manufacturing hub towards a hi-tech service-based economy with a strong and vibrant middle class.”

Chart 1: Chinese mutual fund industry AUM (billion CNY)

Source: J.P. Morgan Asset Management, Wind Data; data as at 30 September 2017.

Footnotes

Source: Wind Data; as at 30 September 2017.

Source: Wind Data; as at 30 September 2017.

Source: Wind Data; as at 30 September 2017.

Source: The securities above are shown for illustrative purposes only. Their inclusion should not be interpreted as a recommendation to buy or sell.

Source: Wind Data; as at 30 September 2017.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.