Money market funds – opportunities amongst the challenges

Published: May 2023

Money market funds are back in business now that central banks have boosted yields to levels not seen in years and the uncertain outlook incites investors to keep their powder dry. Market expectations are that official rates have not yet peaked, while volatility in fixed income appears set to continue.

At the start of March, investors appeared convinced that the European Central Bank (ECB) and the US Federal Reserve (Fed) would raise their key interest rates to 4% and 6%, respectively, and hold them at those levels for several quarters to ensure inflation returned to their 2% targets.

However, the financial stress then triggered by the closure of a regional bank by US regulators led markets to revise down the anticipated level of the central banks’ terminal rate in this cycle. Investors considered recessionary risks for the US economy had increased due to a likely contraction of credit as regional banks tightened their lending conditions for the small and mid-sized corporate sector.

We still believe in a scenario of a moderate recession in the US and anaemic growth in the eurozone. Markets remain wary, although the US authorities rapidly took measures to ensure market liquidity and financial stability.

While central banks have been prompt in announcing measures to maintain orderly markets, there is no indication that they will make concessions on the other part of their mandate – ensuring price stability.

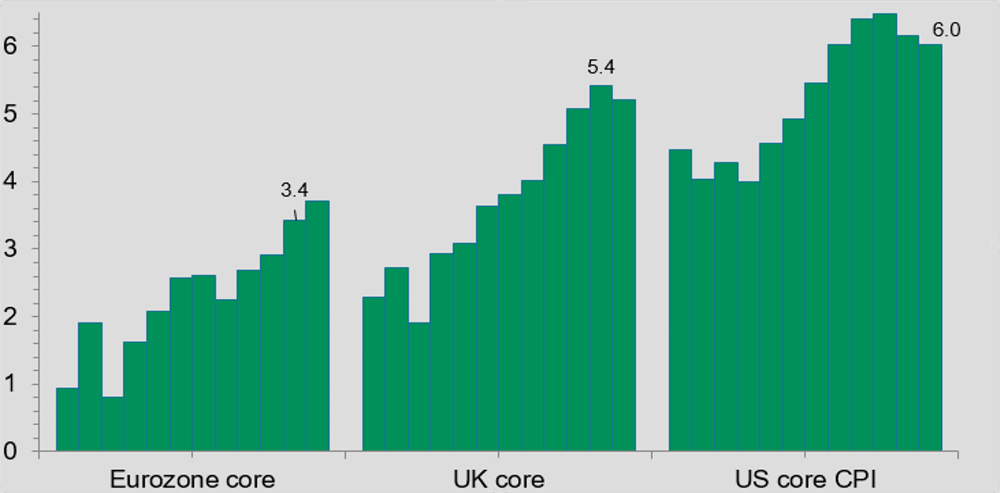

Indeed, we believe stubbornly high core inflation will necessitate restrictive monetary policy for some time yet, particularly in Europe. Hence our expectation that official rates have not yet peaked.

Exhibit 1: Core inflation is still rising in the eurozone

Source: BNP Paribas Asset Management, as of 24 February 2023

This is also the message from the latest central bank forecasts and comments, including those made during the financial turmoil. For example, the ECB indicated that recent tensions in financial markets added uncertainty to the outlook but made no change to its baseline scenario requiring tighter monetary policy.

To quell inflation, the Fed signalled ‘some additional policy firming’ might be needed. Several Fed officials have reiterated that the federal funds rate should be raised above 5% (i.e., there are probably a couple more rate rises to come) and that a positive real rate should be maintained for some time.

Exhibit 2: Our base-case scenario for the US

Q4 2022

Q1 2023

Q2 2023

Q3 2023

Q4 2024

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Gross domestic product (GDP) (year-on-year %)

0.9

2

2.7

2.1

0.8

-0.7

-1.2

-0.7

0.6

Core personal consumption expenditures (PCE) (year-on-year %)

4.8

4.6

4.4

3.9

3.5

2.9

2.5

2.3

2.2

Federal funds rate % (top of band)

4.5

5

5.5

5.5

5.25

3.25

1.75

1.75

1.75

Source: BNP Paribas Asset Management, as of 28 March 2023

What are the consequences for money markets?

Over the last year, the Fed and the ECB have made major adjustments to their monetary policies. The ECB has raised its deposit rate by 350bp from a negative 0.50% in the summer of 2022 to +3% today. The Fed has tightened policy by 475bp over the last year, taking the fed funds rate into the 4.75%-5.00% range.

After a long period of very low yields, money market funds are back in business. This is especially so given the considerable uncertainty about the economic outlook and prospects for risk assets in an environment of slower economic growth.

Exhibit 3: Our base-case scenario for the eurozone

Q4 2022

Q1 2023

Q2 2023

Q3 2023

Q4 2023

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Gross domestic product (GDP) (year-on-year %)

1.8

1.2

0.4

0

-0.1

-0.1

0

0.3

0.7

Inflation – Harmonised index of consumer prices (year-on-year %)

5.1

5.6

5.4

5

4.1

2.9

2.6

2.2

1.9

ECB deposit rate

2%

3%

3.50%

3.75%

3.50%

3.25%

3.00%

2.75%

2.50%

Source: BNP Paribas Asset Management, as of 28 March 2023

Risk/return profile favours money markets

With the current high level of yields in money markets and equity markets still fully priced, risk-reward profiles favour cash. Money market funds, especially short-term ones, can be seen as a perfect holding solution for investors in volatile equities or diversified products.

Even in an optimistic scenario of soft landing (which even the Fed deems unlikely based on the March Board staff forecasts), equity upside seems limited at current levels and unattractive relative to yields in money markets or short-term fixed income.

On the downside, even a mild recession may lead to equity markets retesting their previous lows and result in a meaningful downside. Money markets and short-term fixed income provides not only full protection on the downside but also optionality to buy risky asset classes should such a pullback occur.

Opportunities today

In our money market investment strategies, we have sought to accompany the rise in key interest rates by implementing variable rate strategies, both for US dollar and euro-denominated strategies.

In terms of money market instruments, the unwinding of the ECB’s bank refinancing operations – in other words, the repayment of amounts borrowed in recent years under targeted longer-term refinancing operations (TLTROs) – is already leading to a significant increase in outstanding amounts on the Negotiable European Commercial Paper market from bank and similar financial issuers.

Bank issuers have shown interest in maturities of nine to 12 months. Non-financial issuers have offered very short maturities (between one and four months). The latter represents new diversification opportunities after a long dearth due to a shift to medium to long-term financing after March 2020.

For money market funds, this likely means more liquidity in the maturities where they are primarily active, and, potentially, better yields given the competition between issuers.

Compared to the levels in early 2022, the spreads on bank and non-financial (corporate) issues have widened, creating an additional 25bp uplift to money market fund performance. We see scope for a continuation of this expansion by a few basis points.

Given this significant issuance, we do not consider it appropriate at this time to diversify our exposure to Treasury securities, as valuations are too high.

A revision of the European Money Market Funds Regulation (MMFR) is planned for 2024. MMFs (Money Market Funds) came through the full-scale ‘stress test’ of the pandemic without a hitch. As the AFG (Association of French asset managers) recalled in its response to the European Commission’s consultation on MMFs in July 2022: “No European MMF has been suspended during the pandemic and each MMF has ensured its redemptions”.

Conclusion

We believe that recent events in financial sector institutions have demonstrated the effectiveness of our proprietary credit research, which ranks the credit quality of issuers in accordance with the European Credit Rating Agencies (CRA) directive. The CRA requires asset management companies to assess credit risks internally without relying exclusively on ratings issued by credit rating agencies.

In our view, the rate hikes and the normalisation of other aspects of monetary policy at the US Federal Reserve and the ECB (i.e., the slow reduction of their balance sheets) have increased the attractiveness of money market funds for investors. We will continue to manage our exposure actively while monitoring market opportunities.

Disclaimer

BNP PARIBAS ASSET MANAGEMENT France, “the investment management company”, is a simplified joint stock company with its registered office at 1 boulevard Haussmann 75009 Paris, France, RCS Paris 319 378 832, registered with the “Autorité des marchés financiers” under number GP 96002.

This material is issued and has been prepared by the investment management company.

This material is produced for information purposes only and does not constitute:

an offer to buy nor a solicitation to sell, nor shall it form the basis of or be relied upon in connection with any contract or commitment whatsoever or

investment advice.

This material makes reference to certain financial instruments authorised and regulated in their jurisdiction(s) of incorporation.

No action has been taken which would permit the public offering of the financial instrument(s) in any other jurisdiction, except as indicated in the most recent prospectus of the relevant financial instrument(s), or on the website (under heading “our funds”), where such action would be required, in particular, in the United States, to US persons (as such term is defined in Regulation S of the United States Securities Act of 1933). Prior to any subscription in a country in which such financial instrument(s) is/are registered, investors should verify any legal constraints or restrictions there may be in connection with the subscription, purchase, possession or sale of the financial instrument(s).

Investors considering subscribing to the financial instrument(s) should read carefully the most recent prospectus and Key Information Document (KID) and consult the financial instrument(s’) most recent financial reports.

These documents are available in the language of the country in which the financial instrument(s) is authorised for the distribution and/or in English as the case may be, on the following website, under heading “our funds”: https://www.bnpparibas-am.com/

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.