The face of corporate funding is changing. Companies have been keen to lock in long-term funding while borrowing rates remain low, and with bank finance retreating under mounting regulatory pressure, the bond markets have become an increasingly popular destination for corporates.

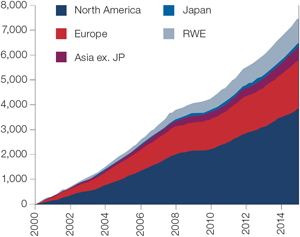

As a consequence debut bond finance has been surging across all the markets. As of June this year, a total of 402 newly rated companies have made their first issue globally, close to a 10% increase on the 364 companies who debuted during the same period in 2013, according to figures supplied by Moody’s (see Chart 1).

Chart 1: Newly rated issuers: global

Source: Moody’s Ratings Service

“Since the crisis the credit quality of corporates has improved massively,” says Pascal Ba, Head of EMEA Corporate Debt Capital Markets at Bank of America Merrill Lynch (BofA Merrill). “Because of that investors are more comfortable with this asset class at the moment and they are prepared to take the time to understand and invest in new names.” What this means is that capital market skills are becoming increasingly important to treasurers, wherever they are in the world.

Irish airline Ryanair is one company to have recently taken advantage of the growing penchant for ‘new names’ amongst fixed-income investors. “We have a large capital expenditure programme coming over the next five years,” explains Neil Sorahan, Finance Director at Ryanair. With commitments to buy 180 Boeing 737 aircraft in the years ahead the company sought access to financing that had ‘deep pockets’ and long tenor. They also wished to diversify their funding, having relied heavily in the past on secured financing. And, of course, they wanted to borrow cheaply.

“The debt capital markets, particularly in the current environment, gave us access to that,” says Sorahan. In June, the budget airline made a debut €850m BBB+ rated bond offering. The pricing the company secured, even in the context of ultra-low base rates, was excellent. In a sale that saw over €7 billion of orders, the coupon was fixed at just 1.875%, the cheapest BBB+ issuance in the market to date. Even still the bond was nearly eight times oversubscribed.

Tapping the capital markets is, of course, very different to raising equity finance or applying for a loan through a banking partner. For companies going through the process for the first time, understanding the particular nuances of the bond market quickly will be essential to get the best possible pricing on their credit. What then, have Ryanair’s finance team learnt from their debut issue? And what tips do they and the banks that facilitate such deals have for others considering the capital markets for the first time?

Picking the right advisors

The first point is that it would be a mistake to underestimate the workload involved in tapping the capital markets. Corporate treasuries are rarely overstaffed, after all. It is perhaps just as well then that this is a very well-trodden path where treasurers should be able to quickly find the assistance they need to lighten the load.

“If you are giving advice to a corporate that is planning to go into the market for the first time, my first piece of advice would be to pick experienced bookrunners and appoint an independent adviser if needed,” says Russell Maybury, Vice Chairman, UK Debt Capital Markets, RBS. The right advisory team will take a lot of the burden off the shoulders of the treasury, he notes. “They can assist you in every step of the issue, including the documentation, the investor memorandums, ratings advice and the roadshow.”

Ryanair agree that picking the right advisors is important. In their case, Citi were appointed to help them through the ratings process and were joined later by BNP Paribas (BNP) and Deutsche Bank to be book runners for the issue. Although tasks such as preparing the legal documentation ultimately proved to be relatively straightforward, Sorahan says the advice the business received at each stage of the issue was valuable to them as a capital markets debutant. “We had numerous calls on strategy with them (Citi, BNP and Deutsche Bank) throughout the process, discussing at each stage the best way to proceed, early pricing indications, and so on,” says Sorahan.

Getting rated

There is near universal agreement on the fact that a credit rating is needed for companies to secure the best pricing and volumes on the capital markets. For Ryanair, who were unrated when they began considering a bond issue, this was evidently a top priority. The important thing for those in charge of the issue was not to get the highest possible rating, however, rather a stable one which they felt could be comfortably maintained. The investment-grade BBB+ rating they were ultimately awarded by S&P and Fitch Ratings – the highest of any airline in the world – seemed suitable in that respect.

“S&P awarded us an A- anchor,” says John O’Flynn, Treasurer at Ryanair. That effectively means, he explains, that when you put the Ryanair model through S&P’s grading system, they come out in the A category. In the end, they ended up one notch down O’Flynn believes that resisting the temptation to overstretch in search of the highest possible rating was the right move though, and would advise other debuting companies to follow the same practice.

Positioning your credit

Once the credit rating has been obtained the next job is deciding what form the issue will take. There are, of course, a multitude of different options for corporates across the global capital markets, and different maturities that can be targeted. Ryanair, for instance, had to choose between a euro medium-term note programme (MTN) or US-dollar or euro private placements. There is no universal answer to these questions: what makes sense for one business is typically a reflection of its particular circumstances and priorities. But these early considerations are, says Ba, going to be critical to the success of the issue. “The key is to be really well prepared in terms of ambitions,” he says.

Companies that want to issue bonds need to have a clear view of what can and cannot be achieved. Having that awareness, it becomes much easier to position the marketing of the bonds. “I think one of the risks for a debut issuer is to be too focused on the pricing element and not enough on the credit position. When an investor buys credit, it’s because the credit has been correctly positioned.”

A lot of the new companies coming to the market are small, relative to other issuers, and it is going to be a challenge for them to issue on ten-year maturities. So they may find that a medium-term note (MTN) on the five-seven year part of the yield curve is the best option. “That is often the sweet spot for investors in that situation, unless they benefit from a solid investment grade rating,” he notes. Which market to issue in, meanwhile, will often be determined by the geographical footprint of the business and which currencies it has revenues in.

In the case of Ryanair, whose revenues are all in euros and do not intend their financing to be a one-off, the decision to issue a euro denominated EMTN programme was an easy one.” Now we have all the ratings work and documentation in place, it should be a relatively straightforward and quick process to reissue. That will allow us to take swift advantage of movements in the market when opportunities present themselves.”

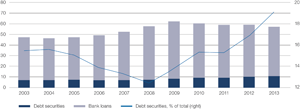

Chart 2: Funding mix shifts towards capital market instruments

Outstanding amounts with non-financial corporations in the euro area. Percentage GDP (left)

Source: ECB, Deutsce Bank Research

However, that is not to say the company will take the same approach when they return to the market in future. On the contrary, Sorahan says they are open to trying new things in the future. “We will look at all forms of suitable financing as we move forward,” he says. “We will continue to look at the likes of the global bond in the United States and the private placements market. But for the size of the transaction we’re looking for, the EMTN seemed like the ideal place to start.”

On the road

“Don’t fall into the trap of expecting that a fixed-income roadshow will be more or less the same as an equity roadshow,” warns BofA Merrill’s Ba. “They are very different.”

The first thing those familiar with equity roadshows will notice is the obvious difference in priorities. To fixed-income investors, the growth trajectory of the business is but a secondary consideration. What these investors are really after, and what new issuers need to focus on, is to be convinced that the company will be able to meet its repayment commitments whatever happens.

It will be hard work. Ryanair’s own campaign, for example, comprised more than 30 one-on-one meetings and group presentations in eight different European cities in just four days. But the roadshow should not be taken lightly by anybody, especially new issuers. Investors will, of course, be able to obtain public information indicating the financial health of a rated company, but they will not yet know the business on a deeper, personal level.

So the roadshow is the company’s big chance to impress, and the presenting team would be well advised to go as prepared as possible. “We always encourage debut borrowers to practise their roadshow thoroughly before they go on the road,” says RBS’s Maybury. “It won’t necessarily go wrong if you don’t, but we do feel it gives you a better chance of success.”

In the current environment there is little doubt around whether you will get your money or not. What is at stake, however, is the pricing. Sometimes a good performance on the road can make all the difference when it comes to grabbing the intention of prospective investors. “On some road shows you see that the issuer is doing a great job of winning over investors,” says Maybury. “On the other hand, sometimes you feel that they aren’t generating the same level of enthusiasm.”

No time to lose

The last, but certainly not the least, thing for treasurers to note is to keep a watchful eye on market conditions. With experts agreeing that the favourable market conditions for corporate debt issuers are likely to continue through 2014, should a corporate considering a debt issue move now or wait for the market to move even further in their favour?

Most experts believe it would be unwise to delay. We saw last year how even a hint from the Federal Reserve of a reversal of accommodative monetary policy measures panicked markets and drove up yields on government, and by extension, corporate debt. With recent tensions in Crimea and ongoing conflicts in the Middle East, the geopolitical backdrop in 2014 is far from settled either. The longer a corporate waits, the more chance there is of an event producing a massive swing in government yields.

Until then though, conditions remain favourable, and corporates with the ability to tap the capital markets would be advised to continue taking advantage, even if the cash is not needed right now but somewhere further down the line. “I think we will continue to see more borrowers coming to the market. Investor appetite is very strong, and they are looking at opportunities they wouldn’t have considered just a few years ago. Issuers can certainly feel very confident and, even if they have only a very small requirement, the bond market will be very keen to see them.”