Whether you are looking for a traditional short-term money market fund or a fully customised solution, finding products that match your liquidity needs is crucial to any successful cash investment strategy. In this Product Profile, we look at a range of available liquidity products, how they differ in terms of risk, return and duration and how they tie in with cash segmentation. We also discuss the ways in which yield can be maximised for a given level of risk.

Maintaining sufficient liquidity while generating a suitable level of return from a pool of cash investments continues to be a challenge for today’s corporate treasurer. There is no easy answer to striking the right balance, but adopting an organised investment approach by segmenting cash according to its purpose – and therefore the time horizon for which it can be invested – is a good first step. Segmenting cash also makes it easier to identify those investments that accurately align with the company’s desired risk/return profile.

Companies may categorise their cash differently, but usually there will be two, three or four options reflecting the short-term, medium-term and longer-term needs of the business. It is possible that there will be sub-categories according to location or currency, for example, and the liquidity management structures in place (such as cash concentration and notional pooling) will also need to be taken into account. Broadly speaking though, the following categories provide a simple, clear and useful segmentation between the different types of cash a company has:

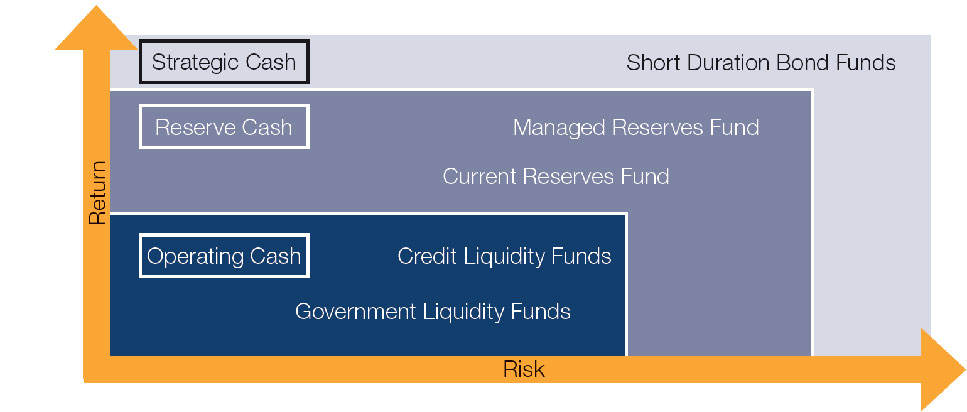

Operating (short-term horizon)

Cash typically used for daily operating needs which is likely to be required at very short notice.

Requires preservation of principal, late-day access and same-day liquidity.

Reserve (medium-term horizon)

Same-day access not needed, although must be kept liquid in case of unforeseen requirements.

Cash set aside for possible acquisition, stock repurchasing and R&D.

Typical investment horizon of 3 to 12 months.

Strategic (longer-term horizon)

No short-term use forecasted.

Cash on the balance sheet that has not been historically used.

Investment horizon of one year or longer.

But what instruments are available to maximise the use of surplus cash across these segments and across the liquidity spectrum?

Informed investing

Travis Spence

According to Travis Spence , Head of Global Liquidity, Asia Pacific, J.P. Morgan Asset Management, corporates that are looking to truly optimise their cash investments should consider broadening their horizons beyond bank deposits. “That’s not to say that deposits are not useful tools – they absolutely are –and in some cases, they are the only available option.

However, many corporates have simply relied on bank deposits as a matter of legacy process rather than active decision making. Fixed Income Markets, especially in Asia, have developed rapidly over the past five years. Now, more than ever, it is crucial for companies to revisit and update their investment policies and practices, taking into account all of the investment instruments available to them.”

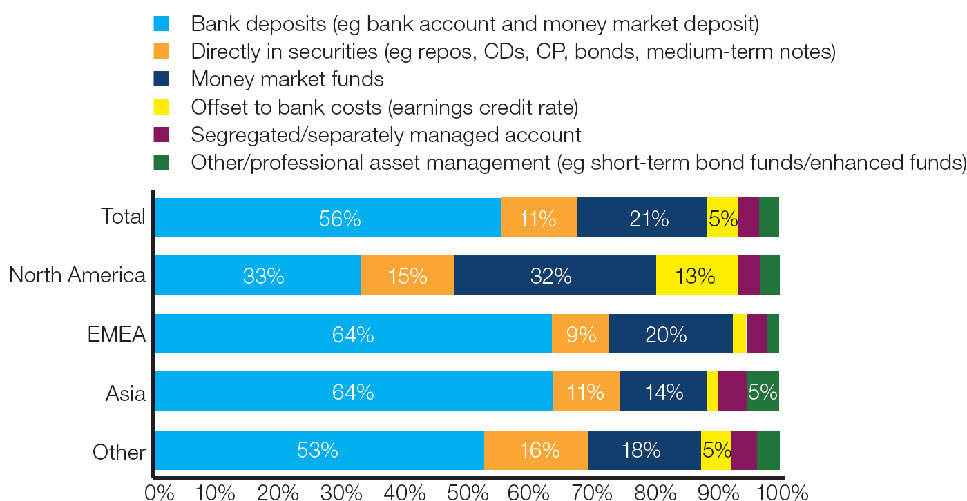

Some companies are already doing just that, as the results of the J.P. Morgan Asset Management Global Liquidity Survey 2011 demonstrate:

Q. How is your surplus cash currently allocated?

Please indicate the asset allocation of your total surplus cash portfolio as of 30 June 2011

In fact, treasurers across Europe and Asia have a similar allocation to instruments outside bank deposits. However, these results also highlight the heavy reliance on bank deposits that Spence mentioned. “At J.P. Morgan Asset Management, we are able to place bank deposits through our parent bank, if that is what is best for the client. But we also have a suite of liquidity products available for ‘all seasons’ from a risk-return perspective. In other words, no matter which way a client’s requirements shift from a risk standpoint, from an interest rate or currency perspective, we have a product to suit their needs.”

The range of short-term investment products available from J.P. Morgan Asset Management (JPMAM) Global Liquidity encompasses the following:

Stable Net Asset Value (SNAV)

Government Liquidity funds. AAA-rated funds with same-day liquidity investing predominantly in government issued securities, offering maximum security.

Liquidity funds. Also known as credit funds or money market funds are AAA-rated funds with same-day liquidity investing in a broad array of money market securities selected by JPMAM’s global team of credit analysts.

Variable Net Asset Value (VNAV)

Current Reserves Funds. These are AAA-rated funds investing in a broad array of money market securities while potentially offering an incremental return over AAA-rated liquidity funds.

Managed Reserves Funds and Strategy. Either AA-rated funds or separately managed accounts, these potentially offer an additional return over AAA-rated liquidity funds while maintaining a low level of volatility.

Short Duration Funds and Strategy. These funds or managed accounts potentially offer an additional return over a low duration market index while maintaining a moderate level of volatility.

J.P. Morgan Asset Management’s suite of liquidity solutions extend from the very safest fund offerings to those that cater for a slightly higher appetite for yield. This means that our experience not only spans a broad risk-return spectrum but also takes into account a variety of liquidity needs.

“Moreover, the solutions we can offer in our liquidity fund range are becoming increasingly global,” says Spence. “We expanded from a USD MMF house in 2000 to offer euro and sterling funds. Since 2005 we pioneered the development of a consistent platform of money market funds in Asia including Chinese renminbi, Japanese yen, Singapore dollar and Australian dollar. And more recently we added solutions in Brazilian real. So our platform is very international from a currency perspective too.”

Matching requirements

“Of course, our conversations with clients aren’t about the presentation of our product line up though,” Spence explains. “It’s a question of understanding how well they know their cash position, as well as the policies they have in place to manage their cash. In conjunction with that, we like to have a healthy discussion around issues in the short-term investment space and the outlook for the current yield environment. That really enables us to get a holistic picture of how the client’s cash could be put to best use, whilst ensuring liquidity requirements are met.”

Speaking about which products are most suitable for each segment of cash, Spence says: “Our SNAV products – the credit funds and the government liquidity funds – are ideal for operating cash, that is, day-to-day working capital type liquidity. From a regulatory perspective, both of these SNAV funds fall under Rule 2a-7 in the US and under the ESMA definition of a short-term MMF in Europe. This means that they have daily liquidity and the investor sees no volatility and cash equivalent in accounting treatment.”

Stepping out a little further along the liquidity spectrum, we then have our Current Reserves and Managed Reserves funds. These are ideal for reserve cash allocations with longer investment horizons, from over one month to over six months, respectively. Such funds tend to sit just outside of the 2a-7 and ESMA short-term MMF space and by their nature they may carry slightly lower levels of liquidity. There may also be some volatility as these funds have a variable NAV. Nevertheless, in a product like this, the volatility is still managed to tight parameters.

“As we step out further again, we enter the short duration funds space, which is ideal for strategic cash allocations with an investment horizon of over 12 months. Again, volatility will be more noticeable in this kind of fund, but while an investor may see a deterioration in NAV on a daily or even monthly basis, this would perhaps not be the case over a historic rolling three-month period – hence the longer investment horizon.”

In addition to its range of funds, J.P. Morgan Asset Management also offers separately managed accounts in all our major markets including China. These are for clients who require a customised portfolio of securities to meet specific investment needs. Portfolios can be tailored based on a client’s credit risk, interest rate risk, cash flows, tax status and investment horizon. When establishing a separately managed account, J.P. Morgan’s teams work closely with the client to set a clear mandate.

The portfolio management team for a separately managed account also holds discussions with the client to establish the desired investment objective, benchmark, expected risk/return characteristics and other requirements of the new account. Based on these in-depth conversations, an investment strategy is developed, as well as a set of investment guidelines. These guidelines will be closely followed at all times in order to successfully execute the investment strategy on the client’s behalf.

“Our aim is to help clients identify which products are best suited to their liquidity needs and also to help them recognise how yield could be maximised, while adhering to any risk parameters,” adds Spence. But why choose an asset manager to invest your surplus cash, and more specifically, why choose J.P. Morgan Asset Management?

Segmenting cash across the liquidity spectrum

Working with an industry leader

“We are one of the world’s largest liquidity managers and we have a first class reputation for managing short-term investments. This has been built over a number of decades of prudent investing. Likewise, we have a relentless focus on risk management which underpins everything that we do.”

Moreover, J.P. Morgan Asset Management is able to leverage its size and scale to the advantage of its clients, accommodating transactions without sacrificing daily liquidity. The asset manager operates the world’s largest AAA-rated prime MMF; the largest international US dollar liquidity fund; the largest euro liquidity fund; and the largest US government MMF. It is also very highly ranked in the industry:

No. 1 international MMF complex.

No. 1 provider of institutional MMFs.

No. 1 global manager of AAA-rated MMF assets.

No. 1 global manager of government MMF assets.

Consistently honoured with industry awards, J.P. Morgan Asset Management also has significant experience in working with a range of clients, including some of the world’s largest corporations and financial institutions. As Spence says: “We pride ourselves on being a liquidity partner for clients of all sizes, whether they are investing locally or globally, and whatever the economic ‘weather’ may be. We believe in creating long-term, strategic partnerships with clients through consultation, expertise and, of course, quality investment solutions.”

Source: iMoneyNet as of 30th March 2012

J.P. Morgan Asset Management

J.P. Morgan Asset Management, the investment management arm of J.P. Morgan Chase, offers a range of comprehensive global short-term and medium-term investment solutions, from AAA-rated liquidity funds to short-term fixed income products. A combination of these products can assist you to achieve the liquidity, security, risk and return profile that you desire.

By entrusting your liquidity investments with J.P. Morgan Asset Management you can be sure that you are investing with a market leader.

Please note that this document is for institutional investors’ use only. It is not for public distribution and the information contained herein must not be distributed to, or used by the public.

J.P. Morgan Asset Management is the brand for the asset management business of J.P. Morgan Chase & Co. and its affiliates worldwide. This communication is issued by the following entities: in the United Kingdom by J.P. Morgan Asset Management (UK) Limited which is regulated by the Financial Services Authority; in other EU jurisdictions by J.P. Morgan Asset Management (Europe) S.à.r.l., Issued in Switzerland by J.P. Morgan (Suisse) SA, which is regulated by the Swiss Financial Market Supervisory Authority FINMA; in Hong Kong by JF Asset Management Limited, or J.P. Morgan Funds (Asia) Limited, or J.P. Morgan Asset Management Real Assets (Asia) Limited, all of which are regulated by the Securities and Futures Commission; in Singapore by J.P. Morgan Asset Management (Singapore) Limited which is regulated by the Monetary Authority of Singapore; in Japan by J.P. Morgan Securities Japan Limited which is regulated by the Financial Services Agency, in Australia by J.P. Morgan Asset Management (Australia) Limited which is regulated by the Australian Securities and Investments Commission and in the United States by J.P. Morgan Investment Management Inc. which is regulated by the Securities and Exchange Commission. Accordingly this document should not be circulated or presented to persons other than to professional, institutional or wholesale investors as defined in the relevant local regulations. The value of investments and the income from them may fall as well as rise and investors maynot get back the full amount invested.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.