Industry View: Jason Straker, J.P. Morgan Asset Management

Published: Sep 2016

With regulatory reforms expected in the money market fund industry, negative interest rates, and Basel-pressured banks becoming ever more selective about the deposits they accommodate, treasurers are having to rethink short-term investment strategies. But what alternative investment opportunities are being explored by corporate cash investors? Jason Straker, Client Portfolio Manager, Global Liquidity Group, J.P. Morgan Asset Management, talks about how investment portfolios are changing and what clients need to know before using alternative investment vehicles.

Jason Straker

Head of Client Portfolio Management, Global Liquidity EMEA

What does J.P. Morgan’s Global Liquidity Investment PeerView Survey tell us about the way in which corporate investment portfolios have been changing over recent years? How are your corporate clients adjusting in the face of recent regulatory and market changes?

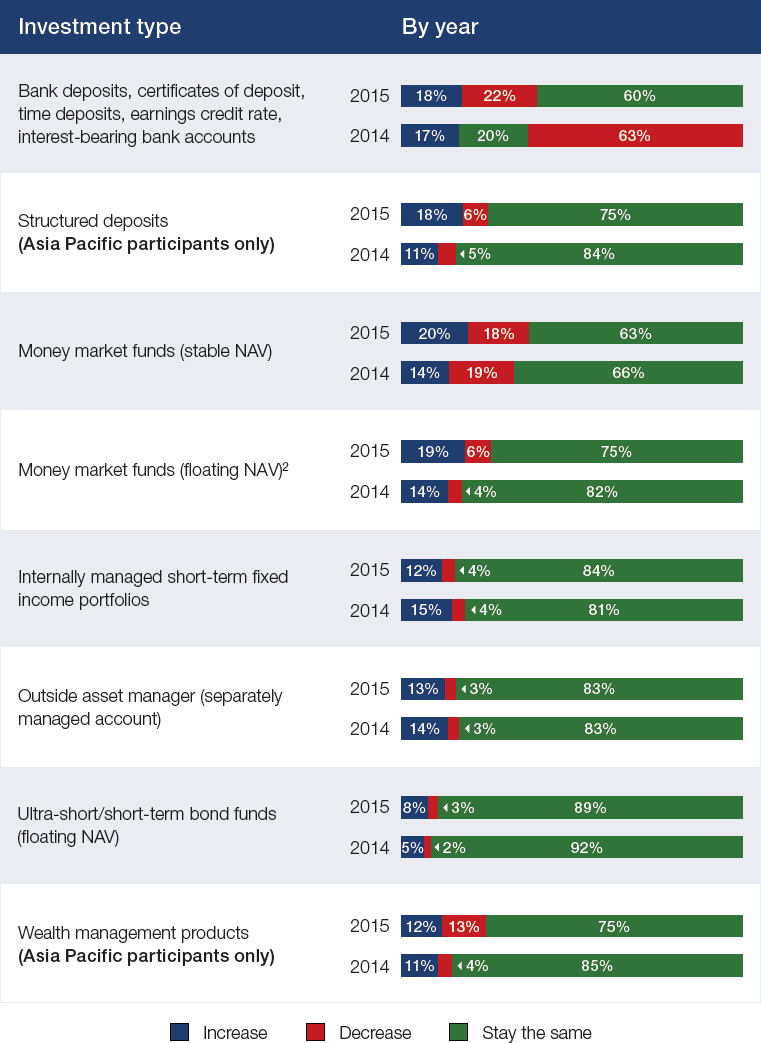

One of the most telling responses we had in the Global Liquidity PeerView Survey came when we asked what changes respondents are likely to make to their investment portfolio in the next year. For each type of cash investment made by corporate treasurers, we saw a high number of increases and decreases in the cash that treasurers plan to invest. Significantly, that includes bank deposits and stable Net Asset Value (CNAV) MMFs, which are obviously important instruments for European treasurers in particular.

So treasurers are evidently thinking about their investment policies; thinking about what to add and what to remove, much more than they have ever done in the past. I think that is a positive development. Given that there is so much happening at the moment, in the market and around regulation and the emergence of new investment products, I would recommend that investors look at and review their policies on an annual basis at the very least. They should not be updated too often, of course, but we are seeing some large corporates updating their policies more frequently in reaction to deteriorating credit ratings, particularly in the financial sector.

What alternatives to MMFs are treasurers now showing greater interest in?

The use of separately managed accounts (SMAs) is definitely on the increase. If we look again at the survey responses, nearly a quarter of respondents with considerable cash on balance sheet are considering an increased use of SMAs in the next year. The growing appetite for SMAs is really a reflection of the fact that investors are searching for yield. They are giving more attention to cash segmentation, so that a portion of their cash can be allocated to products – like SMAs – with longer investment horizons. This ensures that they are not paying for liquidity they do not need.

As an investment vehicle, SMAs represent a good first step beyond MMFs. I think the trend also demonstrates the fact that investors are becoming more sophisticated. After all, SMAs do require a higher level of understanding of the risk-return relationship and the different types of individual investment within a given portfolio. That requires thinking about what specific guidelines make sense. As investors become more accustomed to those investment types they can then take a view on what they feel is appropriate for their own portfolio.

How is J.P. Morgan Asset Management’s own product portfolio evolving to meet the needs of investors in this new short-term investment environment?

Our aim is to offer our clients a range of investment products that sit across the risk and return spectrum. In addition to SMAs, we offer products such as Managed Reserve Funds (MRF) that can work for clients as they continue to move out of MMFs in the search for additional yield.

And our portfolio of products is constantly evolving. For example, in August we launched a new Sterling MRF1; this is a bond fund which will invest exclusively in short-term investment grade sterling securities. So for sterling investors the launch of this product really comes at quite an opportune time, given that post-Brexit we are now facing the prospect of lower interest rates in the UK. We will certainly be continuing to talk to our clients about alternatives like MRFs and help them better understand what it means to move into such products away from more familiar instruments like MMFs.

We also expect to see an evolution in our portfolio of MMF products. When we finally see the details of the forthcoming regulatory changes in Europe it is very likely that we will need to look again at the funds we offer to investors in the region. That could include the proposed Low Volatility (LVNAV) MMF. Should LVNAV MMFs indeed become a reality, we could look at launching or even converting our existing funds to be able to offer the product.

The short-term universe is certainly growing and it is not just the European and US regulatory changes driving this – it is also factors like Basel III and interest rate environment. Of course, this means greater choice for the investor, but the downside is that investors will need to pay more attention to due diligence when using some of these new products as there will be marked differences between them. MMFs are heavily regulated and mostly AAA-rated, so the differences between them from a portfolio standpoint are typically quite small. But when we look at ultra-short bond funds, for example, we see much larger differences between providers, and for investors who wish to use these products it is absolutely necessary for them to understand precisely how they differ.

So what should a treasurer do differently when evaluating potential alternative investment products relative to how they would traditionally go about evaluating a MMF investment?

I think it is important to look at the history of the provider, the resources that are available to the firm and the management of the particular product, including portfolio managers, traders and, perhaps most importantly, credit analysts (who, after all, are responsible for managing the most important type of risk within these products, the credit risk). A good RFP questionnaire, will request information around the track record of the fund, the ability of the team, and the approach to risk management.

Although the key objectives of preservation of principle, liquidity and then yield remain intact – and rightly so – we feel that the realities of today’s short-term investment environment require some new thinking around what these objectives should mean.

With respect to evaluating track records, it is important to look at how different funds have reacted in times of stress. That is often a key differentiator: how a fund manager acted in times when the effective management of risk is critical. When the markets are calm, there will be only a slight difference in returns between managers, but when the markets become more volatile, that is when differences in performance become more apparent. Whether changes were made to the portfolio to avoid credit or liquidity issues is an item that should be of particular interest. Even though one should not simply extrapolate past performance and expect it going forward, it is certainly informative to look at how managers have reacted to different market conditions throughout the interest rate and credit cycle. This sort of analysis can also be performed before investing in SMAs, with investors looking at a composite that represents all the portfolios managed to a particular investment strategy.

Investors should also be cognisant of differences in the way alternative products are treated by the ratings agencies. The rating on a MMF is unique as there is a liquidity component. Ratings agencies will look at some aspects of the fund such as shareholder concentration and the amount of overnight liquidity. That is different to a bond fund rating, which has a much larger subjective or qualitative component. For bond funds, the ratings agencies consider factors such as the stability of the team, the resources and the credit research track record. So it is important to understand how the ratings differ. Typically, MMFs will have a AAA-rating, whilst ultra-short bond funds, like the AA-rated sterling MRF we recently launched, will have a rating based on slightly different criteria.

Outside of the asset management industry, what other short-term investments are being considered by treasurers? What would you say are the main attractions for investors of these products?

One of the investment vehicles treasurers with very large cash balances are taking a lot more interest in lately is reverse repurchase agreements or repo. The first benefit of trading repo is that, because it is not a security or a fund, the accounting of the value of the investment can be stable. There is no need to mark-to-market repo, as the value does not change from one day to the next. That makes life a bit easier for treasurers, from an accounting perspective. The treasurer can simply book the investment and book the interest or yield received at maturity.

There are a number of drawbacks to trading repo for corporate treasurers though. Firstly, they will not normally be offered overnight repo since most counterparties would prefer longer-term deposits. In the post-Basel III world, less than three months is not especially attractive to banks. A second disadvantage is the ever diminishing availability of high quality collateral. Even though central banks around the world have been issuing more debt, the demand for sovereign debt has increased to the extent that the availability of those securities for repo has reduced significantly. Consequently, what tends to happen is treasurers will be offered other types of collateral instead, such as corporate bonds, or what we would call ‘non-traditional’ collateral.

Likelihood of changes to investment portfolio based on next year’s market outlook1

Source: J.P. Morgan Global Liquidity Investment PeerViewSM

“Other” responses are not shown because this was an optional answer choice in 2015; therefore, results are not comparable with 2014 data.

In 2014, this investment was asked only of EMEA respondents. In 2015, it was asked of everyone.

Direct investment into securities, meanwhile, is less in vogue. Five years or so ago, perhaps, it was fairly common to see treasurers buying commercial paper directly themselves. But our Global Liquidity PeerView Survey shows that respondents expect to be reducing, rather than increasing, the use of these instruments. In the current environment, where credit events do occur, that is becoming less popular.

What are asset managers such as J.P. Morgan doing to help clients better understand alternative short-term investment products – what advice would you give treasurers around using such products?

One of the things we do at J.P. Morgan Asset Management to help our clients better understand the differences between various investment products is provide discussions around how each vehicle performs in different market conditions. We demonstrate how the products have performed during periods of market stress, for example, or in an environment where interest rates are rising. And on top of that we provide forward looking analysis to discuss with the client how we believe different products will perform going forward in different market outlooks.

Supplementing that, we also provide a large amount of educational material detailing the different investment types particular funds make. It is not always obvious to cash investors what particular investments a cash fund makes, and therefore such material can be very useful in terms of helping the investor understand why we believe that type of investment is suitable for a low-risk fund.

Finally, in our conversations with clients we are encouraging them to rethink how they define their investment objectives. Although the key objectives of preservation of principle, liquidity and then yield remain intact – and rightly so – we feel that the realities of today’s short-term investment environment require some new thinking around what these objectives should mean. Take, for example, the objective of preserving principle. Should that mean preserving principle from one day to the next or, perhaps, over one week or one month? Similarly, when thinking about liquidity, treasurers might wish to consider whether they require liquidity on any given day or over a period of, say, one month.

This approach allows the treasurer to alter those two measures of risk, to drive the level of yield that they feel is appropriate. That is something we are seeing more of and it is an approach we would certainly urge our clients to consider taking.

JPMorgan Funds – Sterling Managed Reserves Fund is only registered in Austria, Belgium, Germany, Ireland, Jersey, Netherlands, Sweden, Switzerland, United Kingdom and Singapore.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.