Today’s liquidity management landscape continues to present corporate treasurers with considerable challenges. Despite the US Federal Reserve’s decision to raise the base rate from 0.75% to 1% in March, interest rates around the world remain low or, in some cases, negative. Meanwhile, regulatory developments such as Basel III have resulted in some banks having a more limited appetite for liquidity than in the past.

This challenging liquidity environment has prompted corporate treasurers to think differently about the cash they need on a daily basis, and to ask how they can make their cash work harder. In many cases, this is leading to more conversations about the strategic use of cash, with corporates looking to segment their cash into different buckets based on their short-, medium- and long-term needs.

While many corporate treasurers have historically met their investment needs using bank deposits and money market funds (MMFs), these challenges have prompted some to look further afield. In certain cases, treasurers are taking a closer look at the opportunities presented by exchange traded funds (ETFs).

“When corporates segment their cash, the strategic bucket tends to have a bit more flexibility in terms of the investment guidelines and the tolerance to risk,” explains Ashley Fagan, Head of the UK Institutional Team for iShares at BlackRock. “So because of that, there’s a broader range of short duration solutions that they will consider. ETFs sit nicely as a solution within that, as well as broader tailored liquidity solutions that can encompass ETFs, or a combination of ETFs and traditional money market fund (MMF) instruments.”

Overview of ETFs

As the name implies, exchange traded funds (ETFs) are investment funds which are traded on a stock exchange. ETFs typically track an index such as the S&P 500 or FTSE 100 and hold a portfolio of assets such as stocks, bonds or commodities. Investors can buy or sell shares in an ETF in order to gain exposure to a particular index or market. Unlike mutual funds, which are priced once a day, ETFs may be traded intraday.

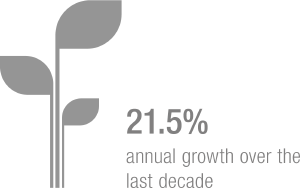

The first ETFs were launched in the late 1980s and 1990s. Since then, ETFs have grown to become a popular investment vehicle for individual and institutional investors alike. Worldwide ETF assets were worth around US$715bn in 2008, but growth in the intervening years has been considerable. As of August 2016, the ETF industry was overseeing assets under management of US$3.4trn, according to EY’s Global ETF Survey 2016, following “a decade of growth averaging 21.5% per annum”. The EY report predicted that AuM will reach US$6trn by 2020.

Bill Donahue, Managing Director in Asset Management and one of the leads of PwC’s ETF practice, notes that, “ETFs continue to experience significant inflows, including a record US$133bn for the three months ended 31st March 2017.” According to Donahue, there continues to be a lot of interest in smart beta ETFs and fixed income ETFs, with ETFs continuing to benefit from the trend towards passive, low cost investment products.

At the same time, a number of different factors are affecting the direction in which the market is developing. “At the macro level we have a more robust regulatory environment putting pressure on traditional commission-driven financial product sales, coupled with the age of the internet shining the light of transparency on the asset management industry,” comments Will Rhind, CEO and Founder of ETF sponsor GraniteShares. “As a result, investors are becoming more educated and are actually seeking out low-cost, transparent and liquid investments. Those are ETFs.”

André Horovitz, Lecturer at London Financial Studies, says that the ETF segment “seems to be blooming as investors tend to be increasingly concerned about the high cost of traditional investment vehicles with historically proven suboptimal delivery of expected returns – especially after costs, commissions etc.” As such, Horovitz says that many investors – both individual and institutional – have pursued a “change of heart strategy” as they migrate towards passive investment vehicles. “Indeed, Vanguard, Dimensional and iShares have recently gained a higher than expected share of the overall investment pie, and this trend seems to continue,” he adds.

Benefits for institutional investors

ETFs have much to offer institutional investors in the current climate. Rhind explains that ETFs offer the same benefits that are true for all investors: “low cost, transparent, liquid investment funds that provide exposure to a multitude of investment themes.”

“ETFs provide the institutional investor price discovery and tighter bid-ask spreads in the fixed income market that has eclipsed that of the bonds themselves that make up the fixed income ETF,” adds Geoffry S. Eliason, Chief Operations Officer and Head of Distribution at Peak Capital Management LLC. “Further, ETFs offer a level of agility that will become imperative as the economy dictates a rotation out of risk assets during a correction or recession.”

Donahue says that ETFs can be used by institutional investors in various ways, including cash management, transition management, rebalancing investments, accessing new sectors and markets, portfolio completion, for hedging purposes and tactical adjustments, and as an alternative to using derivatives. He also notes that ETFs can provide a way of accessing various industries, sectors and geographies. According to Donahue, corporate treasurers are using ETFs for many of these reasons, although some investment strategies are preferred over others depending on market conditions.

Meanwhile, a report published by Greenwich Associates in Q1 2017, ETFs: Dynamic Tools for Institutional Portfolios, highlighted some trends in terms of how institutional investors are using ETFs. According to the report, 45% of institutional ETF investors are now using ETFs for liquidity management, up from 36% in 2015. Other key uses of ETFs cited by the survey’s respondents included tactical adjustments (73%), international diversification (57%), core allocation (55%) and risk management/overlay management (36%).

Treasurers and ETFs

While ETFs might not have traditionally formed part of the investment toolbox for all corporate treasurers, there are a number of reasons why treasurers might consider looking at ETFs in the current environment. “Corporate treasurers recognise that ETFs offer liquidity across various asset classes, a viable solution for cash management, and an effective hedging mechanism,” notes Eliason.

Indeed, the benefits of ETFs for corporate treasurers include the ability to access a range of different risk return profiles. “Another benefit is the transparency they offer,” says BlackRock’s Fagan. “Full portfolio holdings are published on our website on a daily basis, so they have full transparency into what the underlying investments are on an ongoing basis.”

GraniteShares’ Rhind observes that in the US, corporate treasurers, and corporations more generally, have been increasingly attracted to ETFs. “The money market fund debacle of 2008 and subsequent regulatory reform has led in some cases to situations where banks can no longer – or are no longer – willing to take corporate cash as they are holding too much of it and can’t make a return,” he says. “This has led to more interest in short-term government securities and short-term government bond ETFs.”

Recent market conditions have also played a part in underlining the potential benefits of ETFs for corporate treasurers. “There’s more volatility in the market,” says Fagan. “And where returns are concerned, we’ve got the negative interest rate environment with German government bonds yielding -85 basis points in the three-month space, for example.”

These factors have a knock-on effect for corporate treasurers, who may decide to look into alternative investment vehicles as a result. Fagan says that one of BlackRock’s corporate treasurer clients recently reported that they were being charged up to 2% on their USD deposits, even though the US has not adopted negative interest rates. “That just shows you the lessening appetite that banks have to hold these cash balances,” she comments.

How to use ETFs

According to Fagan, when using ETFs corporate treasurers tend to segment their cash balances so that money market funds continue to be used for the core ‘bucket’ while ETFs can be used for strategic cash. In practice, clients might look for tailored solutions such as a combination of different ETFs, or a combination of ETFs and money market funds to suit their investment criteria or guidelines.

While ETFs can provide a number of benefits, there are also some considerations that treasurers should bear in mind when looking at this type of investment vehicle. For one thing, not all treasurers have their own brokerage accounts set up. “It may be obvious, but the first and most important thing to note is that ETFs are exchange traded and are bought and sold like stocks,” says Rhind. “Many companies do not have the ability to trade in or buy stocks especially private companies.”

However, companies which do not have brokerage accounts may still be able to access ETF. Fagan says that while treasurers in this position may be challenged in terms of how they buy ETFs, “we’ve got over that by offering an implementation service for ETFs, so that’s something we’ve dealt with and been able to help corporate treasurers with.”

Understanding the risk-return characteristics

It is also important to be aware that unlike many money market funds, ETFs do not offer a stable net asset value, and to understand the risk-return characteristics of this type of investment. “You are potentially increasing duration compared to money market funds, and potentially adding credit risk as well,” Fagan explains.

Tom Byrne, Director of Fixed Income at Wealth Strategies & Management, points out that with rare exceptions, ETFs have no final maturity. “Depending on what the ETF holds, the ETF could be worth less than for what it was purchased,” he explains. “The same with alternatives. Nothing can provide the certainty than an actual bond or bill (treasury, sovereign or corporate) can provide. If a vehicle promises more than bonds are offering, then there is probably greater risk to principal.”

Not all ETFs are equal

Meanwhile, Eliason says that treasurers should be aware that not all ETFs are created equal. “Tremendous time should be spent understanding the ETF provider, their commitment to maintaining their ETF line-up, the trading and liquidity nuances of the respective ETF, and comparing the underlying holdings of the ETF versus its respective ETF peers,” he explains.

Rhind adds that as with any investment, treasurers should do their homework on what an ETF is invested in and whether they are getting the exposure they want. “Index ETFs just track an underlying index, so knowing what the index is and how it performs is most important,” he comments.

Understand the risks and rewards

Last but not least, Donahue notes that treasurers should make sure that they fully understand ETFs before embarking on this type of investment. “There are a lot of misconceptions on ETFs, including risks, impact on the markets, etc,” he explains. “It is important that treasurers perform their own due diligence to understand the potential risks and rewards with respect to investing in ETFs.”

Where the fine detail is concerned, Eliason says that treasurers should have a deep understanding of the index methodology the ETF represents. In particular, they should:

Be clear on how the index behaves under various market conditions.

Develop confidence in the ETF company and their commitment to not closing an ETF down.

Be familiar with the underlying holdings of the ETF and their liquidity.

Understand how the ETF trades throughout the day, particularly international exposure. Different asset classes trade uniquely at different parts of the trading day.

Evolution of ETFs

With the ETF market growing steadily, considerable developments are taking place in terms of the range of products available. Eliason notes that the ETF universe “continues to grow exponentially, offering cash alternatives, unique ways to carve out the fixed income market, and innovative ways of indexing that may offer more attractive risk-adjusted returns versus traditional market cap weighted indexes.”

Donahue says that the range of ETFs across asset classes is continuing to expand, adding that “fixed income, international equity and multi-asset allocation ETFs were the top three asset classes considered to have the most potential based on our 2016 ETF survey, which will be published in the second quarter of 2017.” He notes that a lot of discussions are taking place about active ETFs, which currently comprise approximately 1% of the US ETF market.

“There’s more volatility in the market. And where returns are concerned, we’ve got the negative interest rate environment with German government bonds yielding -85 basis points in the three-month space, for example.”

Ashley Fagan, Head of the UK Institutional Team for iShares, BlackRock

Rhind says that the biggest trend currently is ‘smart beta’, which involves “inventing new indices primarily in the equity space that have different weighting methodologies to traditional ‘market capitalisation’ indices such as S&P 500 or FTSE 100 where the largest companies, regardless of fundamentals, represent the largest holdings.” He adds, “the Trump presidency is also causing a renewed interest in inflation motivated investments. Commodities, for example, are seeing a lot of renewed interest as a result.”

Fagan says that BlackRock provides a broad range of ETF products, including an ultra-short duration bond ETF which has grown 430% in the last 12 months. She cites the example of a large European corporate which is in the process of reassessing its bank credit risk with banks across the region. “In the past, they would just have considered bank deposit risk as very low risk,” she explains. “Now that’s evolving, and they are looking at ways to reduce concentration risk and increase diversification, which includes looking at strategic cash balances which were historically held in bank deposits.” In light of current negative deposit rates, Fagan says the client has asked BlackRock to look at look at alternative solutions, including a range of short-duration ETFs.

Looking forward, PwC’s publication ETFs: a roadmap to growth found that a number of investor segments are set to drive demand over the next five years, including financial advisors, online platforms, retail investors, ETF strategists, insurance companies and private banks/wealth management platforms. “We are seeing each of these investor segments continue to drive ETF growth in 2017,” says Donahue.

As development continues, Donahue says that many more ETF issuers are expected to come to market over the next 12 to 18 months. “Thus there will continue to be challenges for ETF sponsors to differentiate themselves in an increasingly crowded market.”

In conclusion, ETFs may not be seen as an obvious choice of investment for corporate treasurers. However, in today’s challenging liquidity environment there may be benefits to keeping an open mind to a broader range of possibilities. That said, corporate treasurers considering using ETFs should take the time to understand the risks and returns associated with this type of instrument.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.