Since derivatives are often used by speculators to take positions on price movements in an underlying asset, it is easy to overlook their raison d’être – to hedge risk. In this article, we remind readers that the derivative is a useful tool in the corporate’s armoury.

Derivatives play an important role in risk management, especially hedging, and are commonly entered into by producers of commodities. Indeed, the futures contract, a basic hedging instrument, was devised by Osakan rice farmers in 17th century Japan to mitigate price risk when it came to selling their crop. Rice futures were referred to as ‘empty rice’ coupons in acknowledgement of the fact that the rice was not in the trader’s physical possession.

Today, many derivative contracts – especially futures – are often settled in cash and are traded on futures exchanges such as the Chicago Mercantile Exchange and the New York Mercantile Exchange. For much of their history, derivative contracts were entered into and transacted on the trading floors of these exchanges, but are now for the most part bought and sold over electronic trading networks.

In the current volatile economic environment, derivatives play a more important role than ever. Indeed, in a survey of 130 of its corporate clients, Misys, the global application software and services company, found recently that that its client activity using Misys Confirmation Matching Service (CMS) in 2011 compared to 2010 showed a marked increase in the use of foreign exchange (FX) options by its corporate clients.

Definitions

A derivative is a contract entered into by two parties. The contract is drawn up on an underlying asset, often simply referred to as ‘the underlying’. The underlying can be anything from a foreign currency or stock to an interest rate or bond index.

Derivatives come in two flavours – vanilla and exotic – and tend to be characterised by high leverage. The former are straightforward derivative instruments that allow basic risk mitigation. A simple put/call option is an example of a vanilla derivative. Exotic derivatives, on the other hand, are often complicated and sometimes unwieldy.

The rise of derivatives

The shift to electronic trading coincided with the birth of more exotic futures trading in the 1980s, which saw the deregulation of many of the world’s largest stock exchanges. It was then that derivative contracts started to be written on all number of equities, bonds, interest rates, foreign currencies and other underlying assets. The rise of ever more exotic and complicated derivative instruments has been inexorable – and these were largely to blame for the sub-prime CDO debacle in 2008.

Although they are generally used to mitigate and manage risk, derivative contracts can also be used to speculate on the price fluctuations of the underlying. An investor in the United States, for example, who owns stock in a European company, might mitigate their exchange rate risk on their repatriated dividends by entering into a currency futures contract to lock in an attractive exchange rate.

When derivatives are used to speculate on price movements, they allow the purchaser to gain price exposure to an underlying asset or security – typically a commodity, index or exchange rate, but occasionally to something more exotic such as the amount of rainfall in a region. A derivative contract that is used for speculative purposes does not usually involve the transfer of the title to the underlying security or asset.

Dodd-Frank Act

On July 21st 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act (‘Dodd-Frank Act’) was signed into law by the US President, Barack Obama. Title VII of the Dodd-Frank Act, entitled the Wall Street Transparency and Accountability Act of 2010, establishes a new framework for regulatory and supervisory oversight of the over-the-counter (OTC) derivatives market.

The effect of the Act is to move OTC derivatives onto exchanges and ‘swap execution facilities’ (SEFs), which will mean that most derivatives will henceforth be processed through clearing houses and central counterparties.

Source: KPMG

Using derivatives

Next, we explain how the following derivative instruments work and can be used by corporates to mitigate risk:

Swaps.

Futures.

Forwards.

Options.

Swaps

If a company that is paying a floating interest rate on its debt wishes to fix the interest rate, it may choose to swap its floating interest rate for a fixed rate by entering into a swap contract. When interest rates are swapped, the two companies enter into an agreement to make the other’s interest payments (see diagram below).

The fixed or floating rates the companies pay is multiplied by a notional principal amount, which isn’t typically exchanged between counterparties, but is used as a means of calculating the interest payments to be exchanged by the parties – which are usually netted out. The floating rate is calculated using a reference interest such as LIBOR or EURIBOR.

The first swap agreements were drawn up to allow multi-national companies to avoid exchange controls. Today, as with other types of derivative, interest rate swaps are often used to speculate on and hedge against movements in interest rates.

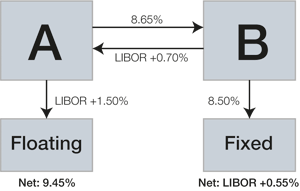

Swaps example

In the above example, company B has swapped its fixed rate (8.5%) for a floating rate (LIBOR +0.70%). Both A and B are still locked into their original loans with their banks. Company A still pays LIBOR +1.5% to its bank, while company B still pays a fixed 8.5% to its bank. However, by signing a swap contract between them, companies A and B have now effectively swapped interest rates.

One of the main reasons a company with a fixed interest rate may wish to swap it for a floating rate is because it suspects the reference rate is due to fall. However, companies also swap their interest rates for other reasons – a company may wish to fix the interest rate of interest payments and thereby eliminate some of uncertainty surrounding its cash outflows, or to hedge against rising interest rate.

Swaps are not always fixed for floating. Floating-for-floating and fixed-for-fixed also occur.

Futures

Futures contracts are similar to forwards because they give the holder the right to buy or sell an asset/commodity at a date and time in the future. A futures contract may require the seller of the contract to physically deliver the underlying asset at the date stipulated – other contracts are settled in cash.

The contract specifics

A futures contract will include the following information:

The amount of the underlying.

The date or range of dates in the future.

The price agreed between the two parties for the derivative.

The contracts are traded on a futures exchange, where the party agreeing to buy the underlying asset expects its price to rise and the party agreeing to sell the asset expects it to fall. Futures contracts are used as financial instruments by producers and consumers, both of whom deal in the underlying physical asset, and also by speculators, who use them as a means of taking positions on price fluctuations in the commodity. For this reason the futures market, can be risky.

When two parties have signed up to the futures contract, the clearing house of the exchange becomes the third party to the deal. A company wishing to trade in futures must first open a futures account with a brokerage firm in order to buy and sell the contracts. Once a futures contract is agreed, the buyer and seller are required to deliver an initial margin (typically 1% to 5%) of the total purchase price of the futures contract.

The profit or loss of the futures contract to each party is calculated daily basis and added to or subtracted from the buyer’s or seller’s margin account, thereby reducing the risk of counterparty default.

Forwards

A close relative of the futures contract is a derivative known as a forward. With a forward contract the buyer agrees to buy an asset/commodity from the seller. The delivery of the asset will take place sometime in the future, but the price is determined at the time/date on which the deal is transacted.

Popular types of forward contract are currency forwards and commodity forwards. Foreign currency forwards are used to hedge an FX exposure when an investor has a payable or receivable in a foreign currency.

The party agreeing to buy the underlying asset in the future assumes a long position, and the party agreeing to sell the asset in the future assumes a short position.

Forwards or futures?

While forwards and futures are very similar types of derivative, there is a fundamental difference between them. Both types of contracts allow people to buy or sell an asset/commodity a time, date and price in the future.

Futures contracts, however, are exchange-traded; forward contracts are private agreements between two parties and therefore are not as rigid. With futures, counterparty risk is much reduced because the exchange acts as the counterparty. Because they are exchange traded, futures are a much more liquid market than forwards – and therefore traders finds their prices more revealing of current market conditions.

Options

As the name suggests, an option is a derivative instrument that gives the purchaser the option of purchasing the underlying asset or commodity at a later date. Of particular interest to treasurers are interest rate options, which allow the purchaser to lock-in interest rates and to limit their exposure to higher interest rates.

An options contract will establish a specific price for the underlying, this is called the ‘strike price’ or ‘exercise price’. There will also be an expiration date included in the contract. There are two varieties of options: call options and put options. When buying a call, you have the right to buy the underlying at the strike price – either on or before the expiration date of the contract. If you buy a put however, you have the right to sell the underlying – again on or before the expiration date.

In addition to the above, an options contract will also specify the quantity and class of the underlying and the settlement terms (ie whether the underlying must be physically delivered or whether the equivalent can be paid in cash.

The purchase price of an option is called the ‘premium’. This is not a fixed amount, as explained in the box below. The most a company can lose on an option is the premium – if the market goes against them then they simply do not exercise the option.

Interest rate options: an example

A company wants to borrow $10m from the bank for three years at a rate of EURIBOR + 0.5%, with EURIBOR at 1.5%. In order to protect the company against increasing interest charges as a result of EURIBOR rising beyond 2.0%, and to fix the maximum borrowing rate to 3.0% (plus option premium), the treasurer buys a three-year interest rate cap.

This option can be exercised every six months. If the EURIBOR rate remains below the strike rate of 2%, the option will not be exercised. Should the EURIBOR rate exceed the strike rate, the writer of the option contract will have to compensate the company for the difference between the two rates. Whether or not the option is exercised, the company will have to pay a premium to the bank writing the option.

The premium

The price of the premium is determined by the notional amount, the length of the term covered by the option and the strike rate. As with conventional insurance, the charges will be higher if it is more likely that the bank will have to pay out. This means the cost of the premium is dependent on the tenor of the option and its intrinsic value, which mainly depends on the difference between the reference rate and strike rate.

Premium= principal × number of days × basis points quote number of days in the year

The premium will be quoted in basis points per annum. If we assume in our example that the bank charges 50 basis points for the option, the annual premium for the three year period will be $50,000.

The pay-out

If EURIBOR increases to a rate of more than 2%, for example 2.5%, at any of the six pre-agreed reset dates, the writer of the option is obliged to pay a compensation for the difference of 0.5% between strike rate and reference rate. For each six-month period, the compensation payment can be calculated as follows:

Compensation payment=Notional amount × difference between strike and reference rate × number of days365

In the given example this would be:

10,000,000 × 0.005 × 183365= $ 25,068.49

As a result of purchasing the option, the company is able to fix its maximum borrowing costs to EURIBOR +0.5% credit margin plus the cap premium, without having to alter the loan agreement. At the same time, the company benefits from any interest rate fall which would translate into lower borrowing costs.

Why might companies use derivatives?

Derivatives can mitigate risk on future price movements in the underlying – be it a commodity, currency or interest rate. If the underlying moves, the derivative protects the buyer from the volatility.

The treasury team can budget more accurately when they know that their exchange rates/interest rates have been fixed for a period.

No need to monitor price fluctuations of the underlying – the contract has locked the price in. This frees up staff for more value-added tasks.

Derivatives are tradable. If the purchaser no longer needs the protection of the hedge, it can be sold on.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.