Corporate bonds were one of the most popular asset classes for investors in 2012. The reason is quite straightforward. Yields on corporate debt may have fallen to record lows, but with governments around the globe committed to maintaining artificially low interest rates, the spreads between corporate/gilts have compressed.

This has created the perfect environment for corporate debt. Investors seeking yield are rushing to buy into the asset class, where they can get better returns than with government debt without exposing themselves to volatile equities. Corporates, meanwhile, have had to find alternatives to bank debt, as bank lending is not as buoyant as it used to be. For example, recent data from the Bank of England’s (BoE) ‘Trends in Lending’ survey reveals that the total stock of lending to UK businesses fell by around $4 billion between September and November 2012. As a result, corporates now need to think outside the box much more when it comes to funding opportunities, and the $4 trillion surge in global debt issuance witnessed over the past 12 months is evidence of this developing creativity.

Getting in while the going is good

With record low rates of borrowing available on the capital markets for junk-rated and investment-grade alike, corporates have rushed to take advantage of market conditions. And, as finance departments start planning further ahead, the “doubling-up” factors of pre-funding and liability management begin to come into play, according to Farouk Ramzan, Head of Corporate Debt, Capital Markets, Lloyds.

“All in all, the cost of debt in 2012 was very low,” he says. “Corporates see the current market conditions as a great opportunity to pre-fund and for liability management – to get more cash on the balance sheet and buy back expensive debt.” Companies, have been funding not just for the current year, but also further out in the future. “That is one of the main reasons for this quick increase in debt issuance,” he says. “Since credit spreads and yields are really low, many treasurers and CFOs are looking beyond the 2012 maturities to 2013, or perhaps 2014.”

As Ramzan explains, companies have been using the bullish trajectory of fixed income capital markets to improve their balance sheets. Ford Motor Company was among a number of companies borrowing on the capital markets taking advantage of a post-fiscal cliff rally in early January, issuing $2 billion worth of 4.75% 30-year notes. Neil Schloss, Vice President and Treasurer of Ford, explains that favourable market conditions were a significant factor in the company’s decision to enter the capital markets for funding in January. “Interest rates have been lowered again and again,” he explains, “and so have credit spreads.” Combining the business case and an ideal capital markets environment meant that issuing bonds is a “no-brainer”. The ability to issue a BBB-rated bond with a sub 5% yield was an opportunity in the market that Ford couldn’t pass up.

“We are using the proceeds partly to call higher cost debt,” he adds. “There is about $600m of similar maturity which has a 7.5% coupon, so that represents a significant saving and interest expense. The bulk of the remainder will be used to fund our pension plans.”

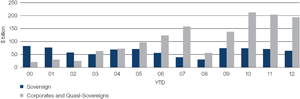

Corporate debt in emerging markets

Despite a very different macroeconomic backdrop, the market for emerging corporate debt has been just as positive. Recent data published by J.P. Morgan reveals that $329 billion worth of emerging market corporate debt was issued during 2012, breaking a record of $210 billion set back in 2010.

In the past, interest in emerging market corporate bonds was often tempered by concerns over the credit worthiness of companies in those regions. Instead, sovereign debt was the main focus for investors seeking exposure to global bonds. Not anymore however. As the chart illustrates, corporate issues have far surpassed issuance of sovereign bonds in each of the past six years.

“Corporates see the current market conditions as a great opportunity to pre-fund and for liability management – to get more cash on the balance sheet and buy back expensive debt.”

Farouk Ramzan, Head of Corporate Debt, Capital Markets, Lloyds

There is a similar dynamic at play in the market for emerging corporate debt as elsewhere, says Esther Chan, Emerging Market Debt (EMD) Portfolio Manager at Aberdeen Asset Management. The falling cost of borrowing has led to greater issuance and therefore increased liquidity. Meanwhile tightening credit spreads, together with the improving fundamentals for emerging market companies, have brought about an increase in investor demand for the asset class. “The good thing is that a lot of these companies, because of access to markets, are able to access cheap funding,” she says. “And having all that additional liquidity in the market helps alleviate the thing which we fear the most – the inability for companies to get the funding they need.”

One of the principal reasons for this positive trend is the greater capacity for growth and development in the emerging markets. But with growth slowing and with various structural challenges now coming to the fore, it may be overly optimistic to expect the same favourable market conditions again this year, Chan argues. “I think that the way companies manage the different growth levels will be important,” she says. “Whether a company wins or loses depends on its ability to navigate through the changing environment. It is much easier to hide your mistakes in times of high growth because your buffer is much bigger.” This is a factor which will rise in importance more for emerging market corporates in the capital markets over the course of the next few years, if it hasn’t begun to already.

Chart 1: EM corporate issuance exceeds sovereign

Source: J.P. Morgan, 10th September 2012

Nevertheless, Chan remains optimistic about the prospects for emerging market corporates to meet these new challenges. Companies in developing economies have a considerable experience of operating in difficult conditions, something which she believes will stand them in good stead for the potentially turbulent times ahead.

The market in developing economies is less homogenous than in the US or Europe, comprising of more than 40 different countries, each with a unique political situation and set of dynamics. And this can be an advantage for investors, offering them a level of choice not likely to be found in the capital markets of developed economies.

With that in mind, Chan expects the investor base for emerging market corporate debt to continue to widen in the coming years, despite the changing macroeconomic backdrop.

Will bonds continue to boom in 2013?

In the capital markets of developed nations, the uncertain economic environment ahead in 2013 is dangerous for investors on two fronts: already marginal yields could be further eroded by inflation; and the value of fixed income assets could deteriorate markedly if central banks, particularly the Federal Reserve, begin to move away from their policy of near-zero interest rates.

A rise in interest rates could be particularly damaging to the corporate bond market. At the end of 2012, the ratings agency Fitch warned that while the damage would be limited by a gradual reversion to higher rates, a sudden rise could have dramatic consequences. According to Fitch’s projections, a typical investment-grade US corporate bond with a ten-year maturity could lose as much as 15% of its market value were interest rates to return to their 2011 levels. For longer duration bonds, the drop would be even steeper with as much as 26% valuation loss anticipated if that scenario were to play out.

Not everyone is convinced of the likelihood of this happening during 2013, however. “I don’t think that corporate bond spread levels are currently in bubble territory,” says Euan McNeil, Co-Manager of Kames Investment Grade Bond Fund and the Kames Investment Grade Global Bond Fund. “If you look at it on a three or four year spread history, they are certainly close to the tights. But on a longer-term view they still offer some value, particularly against underlying government bonds.”

The macroeconomic backdrop should continue to be supportive of the corporate bonds for the foreseeable future, McNeil argues. “We don’t subscribe to the view that government bonds – particularly domestic gilts – will be materially high in 2013, given the relatively moribund economic backdrop and the commitment of central banks to keep rates at exceptionally low levels for the near future. We would be surprised to see any rate hikes before the summer of 2014.”

The market for corporate debt could also be affected in the coming year by forthcoming regulatory changes, such as Basel III and Dodd-Frank. New liquidity rules soon to be introduced by the Basel Committee on Banking Supervision were diluted at the beginning of the year and now allow banks to hold some corporate bonds to satisfy their liquidity coverage ratios. Under the previous guidelines, banks were permitted to hold only corporate debt rated AA- and above, but can now include any bond rated BBB- or above as part of the buffer. But with such high levels of liquidity presently in the market for corporate debt, Ramzan is doubtful that the change will make much difference to demand level. The main thing to be watchful for in the coming year, he argues, is a sudden deterioration in the political situation in either the US or Europe.

“Whether a company wins or loses depends on its ability to navigate through the changing environment.”

“Let’s be clear, if there was a ‘black swan’ event and a risk-off period, then the high yield market would certainly suffer,” says Ramzan. But excluding an extreme scenario, he predicts demand for high yield to continue for the foreseeable future. “And I think that institutional investors are becoming a little bit more comfortable with this ongoing background volatility. So unless there is a major event, I expect high yield issuance to continue to come to the fore.”

No time to lose

With experts agreeing that the favourable market conditions for corporate debt issuers are likely to continue through 2013, should a corporate considering a debt issue move now or wait for the market to move even further in their favour?

Ramzan believes that it would be unwise to delay. With the recent compression in spreads with government gilts, treasurers and CFOs may be tempted to hold out for further tightening that would generate an even lower cost of borrowing. “They are probably right,” he says, adding that he expects to see a 50 basis points tightening over the course of 2013 for the indexes. “However, the problem is that while you go fishing for the best level of compression in your credit spread, there is a risk that something will happen that would produce a massive swing in government yields – and the risk of that happening is probably greater than seeing a three or four point compression in your credit spreads.”

Ford’s Schloss agrees that waiting any longer would not be a gamble worth taking. Corporates should be looking to take advantage of low cost debt while they still can. “I would do it sooner rather than later,” he advises. “Ford Credit is constantly in the market. Over the past three or four years we have issued between $6 billion and $10 billion a year in unsecured bonds – and we’ll be continuing to do that throughout the year in multiple markets.”

“But if I was a one or two time issuer in the market, I would go in early and take the chance while it’s still there,” he adds.