China’s Money Market Fund Regulation in a Global Context

Published: Nov 2014

The global campaign to better safeguard investors in money market funds (MMF) in the wake of the financial crisis has focused attention on fund regulatory efforts in the US and Europe. Less is known about the regulatory environment in one of the world’s fastest growing markets. The rise of MMFs in China has accelerated as investors gravitate to the relative security and diversification of professionally managed funds, not to mention the substantial yield pickup over bank deposits. However, not all MMFs in China are created equal. Financial market regulatory changes over recent years have had the effect of opening the local fund industry to further expansion, and the standards of operation vary considerably. We believe investors can benefit from insights into the range of funds available in China and the risk management guidelines under which they operate.

Sponsor article published: 21st November 2014

China’s Money Market Fund Regulation in a Global Context

The global campaign to better safeguard investors in money market funds (MMF) in the wake of the financial crisis has focused attention on fund regulatory efforts in the US and Europe. Less is known about the regulatory environment in one of the world’s fastest growing markets. The rise of MMFs in China has accelerated as investors gravitate to the relative security and diversification of professionally managed funds, not to mention the substantial yield pickup over bank deposits. However, not all MMFs in China are created equal. Financial market regulatory changes over recent years have had the effect of opening the local fund industry to further expansion, and the standards of operation vary considerably. We believe investors can benefit from insights into the range of funds available in China and the risk management guidelines under which they operate.

Regulatory framework and function

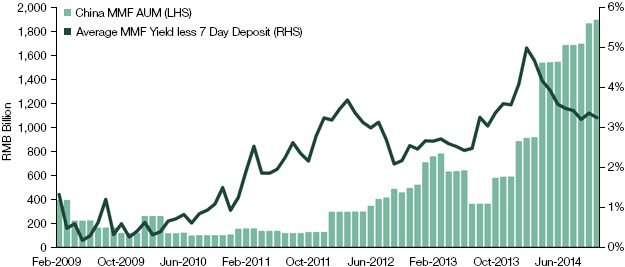

China’s MMF industry is barely a decade old, but assets under management (AUM) have grown nearly fifteen-fold in the past four years alone to around RMB 1.9 trillion as of October 2014.

Figure 1: China’s Growing MMF Industry

With a large and consistent yield pickup vs deposits, MMF AUM has grown rapidly in recent years

Source: WIND, as of October 31, 2014

The industry operates within a formal regulatory framework that has itself come together quickly since the early 1990s, with the China Securities Regulatory Commission (CSRC) as the leading oversight and enforcement authority for MMFs. Overall, the CSRC’s responsibilities include:

Formulating policies, laws and regulations concerning markets in securities and futures contracts.

Overseeing issuing, trading, custody and settlement of equity shares, bonds, investment funds.

Supervising listing, trading and settlement of futures contracts; futures exchanges; securities and futures firms.

Regulatory oversight of money market funds varies globally. In the European Union (EU), there are a number of important regulatory and legislative bodies. National legislators and the European Council, European Parliament and European Commission develop MMF regulation, while national regulators are responsible for oversight. In the US, the Securities and Exchange Commission (SEC) is the primary regulator with discretion over MMF rules, similarly to the CRSC.

Like its international peers, the CSRC is developing policy to address the oversight challenges of a sizeable industry at the core of the financial system. However, the priorities for China’s policymakers at this stage of the MMF industry’s evolution are different from those in longer-established markets. For instance, the SEC and EU institutions are addressing perceived shortcomings as a legacy of the financial crisis, including more restrictions on existing, standardized investment requirements for MMFs. The CSRC, meanwhile, is focusing on ensuring that there is proper oversight of new entrants in a market with many different types of funds—particularly given the ascendance of online funds in the retail space.

“The CSRC, meanwhile, is focusing on ensuring that there is proper oversight of new entrants in a market with many different types of funds—particularly given the ascendance of online funds in the retail space.”

CSRC spokesman Zhang Xiaojun underscored this priority in a press conference on February 28, 2014. Zhang noted that the CSRC is “working to adopt relevant rules on further enhancing risk management for money market funds and supervision of internet-based offers and sales of funds.”

Points of difference

Like its peers in the US and Europe, the CSRC sets risk management requirements for MMFs that limit the duration exposure, credit risk, liquidity risk and concentration of assets in portfolios. The main difference is that CSRC standards allow MMF managers more flexibility than the US and European regulations, particularly given the tightening in SEC and European rules since the crisis. US and European managers are further constrained from a yield standpoint by the historically low interest rates and shortage of high-quality assets in developed markets. The following are key distinctions between the CSRC’s guidelines and international standards:

Duration exposure Money market funds typically comprise very short-dated securities, in order to limit the potential impact of rising interest rates on the value of the investments. The CSRC’s requirements for MMFs allow for greater interest rate management flexibility, both in the overall average maturity and individual investments, than US and European requirements.

In the US and Europe, regulators impose restrictions on the maturity of each instrument as well as the weighted average maturity (WAM) and weighted average life (WAL) of the portfolio in total. In the US, the SEC limits the maturity of any fixed- or floating-rate security to 397 days, with the exception of government floating-rate notes, for which there is no maximum (other than those resulting from the overall portfolio WAL limit of 120 days). The CSRC similarly sets a maximum maturity of 397 days for fixed-rate notes, but does not set a limit for floating-rate securities (no overall WAL limit) although holdings for those floating-rate securities with a maturity that is longer than 397 days may not be more than 20% of the MMF’s assets. As for the portfolio’s average maturity, the SEC and ESMA each impose a maximum WAM of 60 days, while the CSRC’s limit is 180 days.

Net asset value (NAV) Changes to the accounting regime for MMFs were a big feature of the latest US amendments as well as those being contemplated in Europe and they affect how a fund’s NAV (or price at which an investor transacts) is reported. A fund with a “stable NAV” traditionally uses amortized cost accounting methodology, where the price of a unit/share is held constant at 1.00 by amortizing the underlying investments while the actual underlying market prices of investments in the portfolio may be very slightly higher or lower than the amortized price. A NAV calculated using market value prices is commonly referred to as a market-value or shadow NAV. China’s MMFs generally use amortized cost accounting methodology to offer stable NAVs, and managers are required to calculate their market-value NAV and publish their maximum deviation during any calendar quarter following the end of that quarter. By contrast, in the US, within a couple of years, US institutional prime funds will fully switch to a floating NAV, and MMFs that transact at a stable NAV, including government funds and retail funds, will be required to report market-value NAVs on a daily basis.

Credit risk China’s MMFs are permitted to hold a range of assets across government, quasi-government, bank- and corporate-issued securities. While US MMFs can invest in corporate issuance, the US money market regulations specify that no more than 5% of corporate investments can be from a single issuer. In China, the maximum concentration is 10%.

Leverage International MMFs generally do not permit explicit leverage, meaning borrowing for purposes of creating more than 100% asset exposure. In China, the CSRC allows up to 20% leverage via borrowing cash/lending securities in repurchase (repo) markets.

Eligible Assets

Eligible assets for China’s MMFs include the following:

Treasury paper, which is issued by the Ministry of Finance and the People’s Bank of China.

Policy bank bonds are the largest segment of the fixed income market. These securities are issued by three 100% government-owned policy banks, the Agricultural Development Bank of China, Export Import Bank of China and the China Development Bank. Policy bank bonds are similar to Agency paper in the US and Europe.

Time deposits with which MMFs can invest in interbank negotiated deposits with banks.

Corporate securities are available in a variety of structures, including commercial paper and medium-term notes. Typically these instruments have variable liquidity.

Repos including interbank and exchange-traded repos typically with high grade collateral.

Role of ratings agencies

China’s standards are similar to international conventions in that the securities in MMFs are required to have top-shelf ratings. In the US, money market fund rules from leading rating agencies such as Standard & Poor’s, Moody’s Investors Service and Fitch Ratings stipulate that 100% of triple-A rated funds must generally be invested in first tier securities that are rated at least A-1/P-1/F-1.

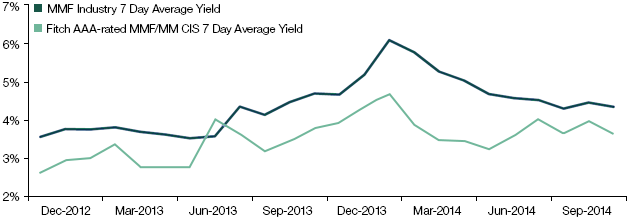

However, triple-A criteria for China’s local ratings agencies vary. When it comes to ratings of the funds themselves, the local agencies’ standards for MMFs are typically no more stringent than the CSRC guidelines. Fitch, the main international rating agency operating in China, sets tighter restrictions in line with global standards, but its triple-A rated funds account for just around 3% (as of September 30, 2014) of China’s MMF industry. Fitch’s1 criteria on factors such as leverage, liquidity and portfolio concentration are consistent with, though not identical to, triple-A guidelines in the US and Europe. For instance, Fitch’s maximum WAM of 75 days is well below the CSRC maximum of 180 days, but still above the global norm of 60 days.

“Fitch, the main international rating agency operating in China, sets tighter restrictions in line with global standards, but its triple-A rated funds account for just around 3% (as of September 30, 2014) of China’s MMF industry.”

1 Fitch triple-A rated funds: include all Fitch triple-A rated money market public funds and collective investment schemes.

The potential benefit in terms of risk management does entail some sacrifice when it comes to yield. Fitch’s funds exhibit a material difference in risk and return versus non-Fitch triple-A rated funds that use the full flexibility allowed under CSRC guidelines. Historically, non-Fitch triple-A rated funds have substantially outperformed, albeit in an environment where corporate defaults are still very rare.

Figure 2: Average Yield of non-Fitch MMF and Fitch rated MMF/MM CIS2

Source: WIND, as of October 31, 2014

2 Fitch triple-A rated MMF/MM CIS: includes Fitch triple-A rated money market public funds and collective investment scheme (“CIS”) in the China market, altogether four of them.

Manager discretion

While MMFs in China have the flexibility to access higher yields, the risks to capital preservation and liquidity can also be higher. This is where the expertise of the fund manager comes in, and risk management is a distinguishing factor in China’s increasingly crowded MMF space. The following are key areas in which a manager’s philosophy can make a difference in this regulatory environment:

Independent assessment of credit risk for various issuers, rather than relying solely on issuers meeting the minimum requirements of credit rating agencies.

Ensuring sufficient liquidity is maintained in the fund relative to the amount and variety of shareholders.

Calibrating duration, whereby some managers will voluntarily restrict WAM even further—down to 60 days—to be more consistent with global practice. This is very pertinent considering the pronounced interest rate volatility in China’s money markets (see China’s Markets: Interpreting Interest Rate Volatility).

“While MMFs in China have the flexibility to access higher yields, the risks to capital preservation and liquidity can also be higher. This is where the expertise of the fund manager comes in, and risk management is a distinguishing factor in China’s increasingly crowded MMF space.”

This expansionary phase of the MMF industry’s development in China is a boon for the growing population of corporate and retail clients seeking alternatives to bank deposits and help in navigating the domestic securities markets. However, investors should also exercise discernment in their choice of manager, given the range of relatively new entrants and the variation in their risk management expertise. In a growth industry so far untested by crisis, it pays to focus on the risks as much as the returns, in line with standards shared by a global community attuned to the challenges of today’s investment environment.

“In a growth industry so far untested by crisis, it pays to focus on the risks as much as the returns, in line with standards shared by a global community attuned to the challenges of today’s investment environment.”

For more information on Goldman Sachs Global Liquidity Management, please contact:

Investment in the money market public funds or CIS is not in the nature of a deposit with a bank or other deposit-taking institutions and is not protected by any government, government agency or other guarantee scheme. There is no representation or warranty as to minimum return derived from such investment, and a loss of principal is possible.

General Disclosures

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material is not financial research and was not prepared by Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of GIR or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and GSAM has no obligation to provide any updates.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by GSAM to buy, sell, or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as investment advice.

Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or its securities. It should not be assumed that investment decisions made in the future will be profitable or will equal the performance of the securities discussed in this document.

Emerging markets securities may be less liquid and more volatile and are subject to a number of additional risks, including but not limited to currency fluctuations and political instability.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

The website links provided are for your convenience only and are not an endorsement or recommendation by GSAM of any of these websites or the products or services offered. GSAM is not responsible for the accuracy and validity of the content of these websites.

The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

United Kingdom and European Economic Area (EEA): In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Asia Pacific: Please note that neither Goldman Sachs Asset Management International nor any other entities involved in the Goldman Sachs Asset Management (GSAM) business maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, Malaysia, and India. This material has been issued for use in or from Hong Kong by Goldman Sachs (Asia) L.L.C, in or from Singapore by Goldman Sachs (Singapore) Pte. (Company Number:198602165W), in or from Malaysia by Goldman Sachs(Malaysia) Sdn Berhad (880767W) and in or from India by Goldman Sachs Asset Management (India) Private Limited (GSAM India).

Australia: This material is distributed in Australia and New Zealand by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (’GSAMA’) and is intended for viewing only by wholesale clients in Australia for the purposes of section 761G of the Corporations Act 2001 (Cth) and to clients who either fall within any or all of the categories of investors set out in section 3(2) or sub-section 5(2CC) of the Securities Act 1978 (NZ) and fall within the definition of a wholesale client for the purposes of the Financial Service Providers (Registration and Dispute Resolution) Act 2008 (FSPA) and the Financial Advisers Act 2008 (FAA) of New Zealand. GSAMA is not a registered financial service provider under the FSPA. GSAMA does not have a place of business in New Zealand. In New Zealand, this document, and any access to it, is intended only for a person who has first satisfied GSAMA that the person falls within the definition of a wholesale client for the purposes of both the FSPA and the FAA. This document is intended for viewing only by the intended recipient. This document may not be reproduced or distributed to any person in whole or in part without the prior written consent of GSAMA. This information discusses general market activity, industry or sector trends, or other broad based economic, market or political conditions and should not be construed as research or investment advice. The material provided herein is for informational purposes only. This presentation does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation.

Canada: This material has been communicated in Canada by Goldman Sachs Asset Management, L.P. (GSAM LP). GSAM LP is registered as a portfolio manager under securities legislation in certain provinces of Canada, as a non-resident commodity trading manager under the commodity futures legislation of Ontario and as a portfolio manager under the derivatives legislation of Quebec. In other provinces, GSAM LP conducts its activities under exemptions from the adviser registration requirements. In certain provinces, GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts and is not offering to provide such investment advisory or portfolio management services in such provinces by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law by Goldman Sachs Asset Management Co., Ltd.

Confidentiality

No part of this material may, without GSAM’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized agent of the recipient.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.