It was yet another huge year for corporate bond issuance in 2013, with the combination of artificially low long-term interest rates and strong investor demand once again pushing debt sales to record levels in European markets.

The issuance boom has resulted in a change in the corporate debt stack. In Europe, companies have traditionally relied upon bank loans for their financing needs. But today, “the loan market share of the corporate debt stack in Western Europe stands at roughly 50%, a reduction of 10% from what it was just two years before,” says Karl Nolson, Managing Director, Debt Finance, Barclays. “In the UK the decline in the same period has been more abrupt, dropping from just over 70% to just inside 50%. Now, there is a considerable amount of liquidity chasing very few deals and this has helped pricing in the loan market to regain some of its competitiveness.”

In the Asia Pacific region, the balance of the corporate debt stack moved in the opposite direction. In the bond markets, the coupons paid on debt increased for many corporates during 2013 after the Federal Reserve’s announcement of its plans to unwind its asset purchases triggered a sell-off in dollar denominated debt across a number of emerging markets. Bond issuance, which had hit record highs in 2012, declined, driving companies back to the more competitive loan market for their financing needs.

Overall though, funding conditions for corporates remain favourable across the board. In Treasury Today’s 2013 European Benchmarking Study, a majority of treasurers (79%) indicated that credit costs had remained the same or declined during the past year. In the Asia Pacific region the figure (75%) was only marginally lower.

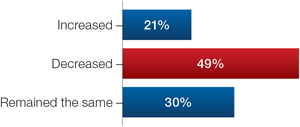

Chart 1: How has pricing changed in the last 12 months?

Source: European Corporate Treasury Benchmarking Study 2013

Corporates know that this era of cheap credit is not going to last forever. With the global economy recovering, interest rates are set to rise sooner or later. To make the most of low borrowing costs conditions while they last, a significant number of companies with existing debt due to mature in the next few years are now entering into negotiations with their lenders to modify and extend terms.

But what is the key to successful refinancing? Every company is different and, as such, are likely to approach such negotiations in their own individual ways. However, when Treasury Today raised the subject of best practices in refinancing with corporates and banks, it quickly became apparent that there are some general principles companies can follow to secure the best possible terms from their lenders.

Cash in on investor bond appetite

Both investment-grade and high yield corporate debt issuance have set new records in the US and Europe over the past year. But such is the volume of liquidity in the global economy at the moment that demand for non-financial corporate debt in the US private placement market is still outstripping the supply, says David Cleary, Co-Head of US Private Placements at Lloyds Bank. This supply and demand imbalance has led some US investors to attempt to differentiate themselves by offering, for instance, delayed funding or euro or sterling denominated debt. The trend might provide those corporates who have the ability to access capital markets some unique financing opportunities, whether that be for the purpose of restructuring existing debt, M&A or growth capex.

“That is one of the appeals of the private placement market to the UK or European corporate,” says Cleary. “Because investors are looking for ways to differentiate themselves, corporates issuing debt in this market can secure much greater flexibility in their financing. It gives them the opportunity to mix tenors and use different currencies and tranches.”

Treasurers evidently now have an abundance of options these days when it comes to refinancing on the capital markets. It is important to consider each of these options early on, says Cleary, referring to the core debt quantum in the business plan and considering the potential impact of any future developments such as mergers and acquisitions or unexpected capital expenditure requirements.

“Finance teams need to ensure that the finance they are putting in place today works over the life of that debt facility,” he says. And that is the case whether the company is looking to take on debt with five year maturity from the bank market, or ten or 15 years in the bond or private placement market. “Assess the options,” adds Cleary. “Ensure that each is fit for purpose, and ensure that the terms and conditions will meet your business needs going forward.”

Take it while it’s there

Ford Motor Company benefited enormously from taking such a forward looking approach when it restructured some of its debts back in 2006. Initially, the treasury at Ford merely intended to renegotiate the company’s revolving credit facility, but given the positive market conditions that existed prior to the onset of the credit crisis it soon turned into much more. In addition, a separate term loan was taken and a convertible bond issued securing a total of $23.5 billion of debt for the company, of which $12 billion was funded and $11.5 billion was unfunded as a backstop facility.

“In a good market without a lot of debt supply coming in you need to come prepared.”

Neil Schloss, Vice President and Treasurer, Ford Motor Company

Neil Schloss, Vice President and Treasurer at Ford Motor Company did not regret for one minute that the company squeezed all the credit it could manage out of the market. Less than two years later the US motor industry was in a dire condition. With the arrival of the financial crisis, Ford, alone among Detroit’s big three auto manufacturers, did not need to request Troubled Asset Relief Programme (TARP) money from the US Government, or declare bankruptcy. And it was the mixture of secured and unsecured funding acquired in 2006 that made the difference during this difficult period.

“It was critically important,” says Schloss when asked about the significance of the restructuring to the company. “It was one of the elements that prevented us from requiring government support during the crisis and meant that, unlike our two big competitors, we didn’t have to cut back on our capital expenditure during that period.”

One of the lessons from this, Schloss notes, is that markets tend to move in cycles which do not always align perfectly with business needs at every given moment. It is crucial therefore to take full advantage of favourable borrowing conditions when they arise. “You tend to take money when you don’t need it and don’t take money when you need it,” he says.

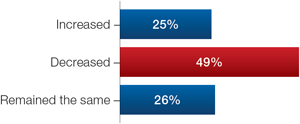

Chart 2: How has pricing changed in the last 12 months?

Source: Asia Pacific Corporate Treasury Benchmarking Study 2013

But in order to take advantage of favourable conditions when they materialise, corporate treasurers need to be on their toes constantly. “Availability today has much shorter windows,” he explains. Therefore, corporates who want to refinance when the market is positive need to be ready on any given day to do it. “In a good market without a lot of debt supply coming in you need to come prepared. If you come in one day thinking that the markets look great, but haven’t planned what to do then you are likely to miss it.”

Engage early with lenders

It is for this very reason that Barclays’ Karl Nolson says it is important for corporate borrowers to engage early and maintain regular conversations with their lenders. This will allow corporates to move quickly and execute a strategy at the point which they need to. It is something which he thinks applies even in the loan market which is not as dynamic as a market for bonds. “Finance teams often tell us that they need to anticipate when the Board is going to ask the question of how much debt can be raised and at what price,” he says. “For that reason, especially in a heightened M&A environment, the conversation with banks should always be ongoing.”

Keeping in touch with lead arrangers will not only help treasurers by preparing them with the information they need to act at short notice, but also take away some of the taxing aspects of the financing process such as documentation and coordinating with other banks in the syndicate to get the best pricing.

Finally, frequent communication with the lender can help the corporate to understand better what is going on at the regional level of the loan market. Although nations are often thought of as distinct markets, there are often considerable regional disparities in pricing. Demand for credit, and therefore the cost of it may, for example, be very different in the North of England than it is in Scotland or London. “If a lender is based in Manchester and it’s their job to look after that region, given the paucity of new loan volumes in general, they really can’t afford to miss out on any loan issuance emanating from that region. So one tends to see regional pricing variations, but staying in contact with the banks regularly can help the treasurer understand how those dynamics are playing out at any one time.”

Be transparent

Frequent communication with your banking partners is one thing, but as the experience of Royal FrieslandCampina testifies, the way in which you communicate is also important. In late 2011, the market for bank finance in Europe was deteriorating as the Eurozone’s debt woes escalated. Nevertheless, Royal FrieslandCampina managed, in spite of these very challenging market conditions, to successfully negotiate with their lenders an “amend and extend” of the company’s €1 billion general purpose syndicated credit facility.

The manner in which FrieslandCampina communicated its expectations with the banks included in the syndicate was critical to the success of the deal, says Klaas Springer, Director of Corporate Treasury at Royal FrieslandCampina. With the help of Zanders Consultancy, the company developed a tailor made solution it calls the ‘Wallet Sizing’ model to help frame the forthcoming negotiations. Using this model, treasury were able to perform their own analysis on the profitability of the business the company was doing with each of the 14 banks in the syndicate, before reporting back to them with the results.

Once treasury had completed this analysis and ascertained that a majority of the banks in the syndicate were satisfied with their relationships with the company, it began exploring the possibility of renegotiating the terms of the loan. In addition to extending the maturity of the loan, treasury also felt that pricing should be brought in line with what other companies of a similar size and creditworthiness were paying in the market.

“They basically couldn’t say no to us,” says Springer, explaining that having the syndicate banks confirm they were happy with the relationship prior to the discussions had put the company in a very strong negotiating position. Although a few banks displayed some hesitancy, as one might expect given the broader economic climate, Springer held that the vast majority responded positively and were tremendously cooperative.

The lesson from all of this, says Springer, is that when it comes to refinancing it pays to be as transparent as possible with your creditors. “They need to understand where you are coming from,” he says. “I always say, if you treat the banks with respect you will get respect back. It certainly helps your cause if you are transparent and involve your banks in the proper way.”

The year ahead

As the global economy improves, the prospect of higher rates is certain to increase. Any corporate with maturing fixed income debt would understandably want to refinance before the Federal Reserve reduces the pace of its $85 billion-a-month asset purchasing programme and yields begin to rise. This, perhaps, is one of the factors that has contributed to the extraordinarily high levels of issuance in recent months and why analysts expect to see it continue at least into early 2014.

The outlook for pricing in the loan market is less certain. In the US, analysts do not foresee any rise in short-term rates until at least the beginning of 2016 while, given the Eurozone’s ongoing troubles it seems likely that policy rates there will remain low for some considerable time. Although the Bank of England has raised the possibility of a rise in 2014, it goes without saying that such a move will be conditional on the UK sustaining its recent return to growth. Instead, the biggest issue for corporates accessing bank finance is likely to be regulation, with the leverage ratios introduced under Basel III, in particular, likely to either increase – or, at the very least, put a floor on – loan pricing.

But the impact at the investment-grade end, at least, shouldn’t be too adverse says Barclays’ Nolson. The corporate with “a good ancillary story” and lots of business to share between its relationship banks will, he adds, always be able to command improved pricing on loans. On that basis, in addition to all the liquidity that is still out there, Nolson expects to see the number of deals continue to pick up as Europe heads towards the next big refinancing spike in 2015. “The number of ‘amend to extends’ has increased significantly through 2013. We expect a lot of borrowers to continue exploring and executing refinancings as we move into 2014.”

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.