Establishing a methodology that enables a treasurer to better understand and react to corporate liquidity requires considerable thought and discussion; there is no one-size fits all solution because no two sets of business needs are exactly alike. That said, it is possible for an individual corporate to construct an accurate picture of how its cash and investment needs can be balanced for both safety and return without losing liquidity cover.

Cash is still king in the eyes of many; it offers flexibility and independence from financial institutions. It’s not surprising then that, as the economic crisis developed, those treasurers that could hold on to cash did so with increasing enthusiasm. “That’s not unreasonable given that there was an increasing fear-factor in the markets,” comments Stephen Houghton, Director, Financial Risk Advisory, Lloyds Bank. With the chief alternative form of short-term liquidity being bank overdraft/loans in the form of revolving credit facilities (RCFs), the fact that many banks had either scaled back on the offering of these facilities or pulled out of the market altogether after the crisis, stock-piling cash was the most logical action in the face of such uncertainty.

For the corporates holding cash, the instinctive reaction to keep investments short, and thus liquid, remains compelling. But Houghton puts the case for revisiting this strategy, arguing that if a balance can be struck between liquidity and return, the treasurer will be ahead of the curve.

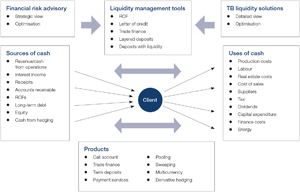

Cash sources and uses

In order to understand how such a balance can be achieved, the first stage is to fully determine the sources and uses of cash within the business and how these can be impacted by:

Business uncertainty (eg future earnings, costs, unexpected capital expenditure (capex)).

Market uncertainty (eg FX translation of foreign earnings, floating interest expense).

Typical sources of liquidity include cash (generated from operations), interest income, revolving credit facilities (RCF), issuance of long-term debt, equity and cash received from hedging activities. A corporate cash balance can be deployed for operational, reserve or strategic purposes and may find its way towards covering typical business costs such as production, labour, real estate, finance, sales, tax, dividends, capex and energy bills.

For some businesses cash flow is cyclical and potentially difficult to balance; for example, the travel sector has fairly well-defined peaks and troughs and many retailers need to build up inventory, pre-season, which must be paid for, before revenue is generated. Failure to adequately manage liquidity can see an otherwise healthy business suffer potentially severe consequences. Tapping reserves of cash may be the solution to protect a business from such adversity, but often other forms of liquidity are called upon.

If a business is unable to generate sufficient cash then it can obtain long-term funding using two of the most common methods: it can either seek equity capital (which can be seen as the ultimate ‘cash buffer’ in that there is no requirement to pay it back and losses are absorbed by the investors), or it can borrow. The latter could be as a long-term loan via the banks or capital markets which, although providing funding certainty over an extended period, can prove more expensive, especially if that cash is intended only as a buffer.

The second option is short-term debt – either through a bank facility such as a RCF, or, if the corporate is large enough, through issuance of commercial paper. The advantage of the RCF is that it can be drawn down and repaid as required and, although this flexibility means it can be expensive, it is nonetheless useful as a short-term solution and one that is almost universally employed. However, notes Houghton, some companies use it as a semi-permanent funding option (and in some cases, their only source of debt) deployed alongside cash from long-term debt as a means of stabilising any seasonality they may have in their cash cycle or as the short-term response to any unexpected outlay. This is not an issue in itself in benign credit market conditions but the scaling back of credit provision by banks after the credit crisis now leaves treasurers with the problem of less certainty around the availability of refinancing in future, which means a more diverse funding strategy is desirable going forward.

Indeed, taking this approach now practically requires businesses to be perpetually in a good state of credit, which clearly is not always the case: if the corporate needs the facility it could be they are in a very difficult financial state and thus may not be able to re-finance the debt when it comes due. At the very least, Houghton says, it is advisable for a corporate to ensure that its bank facilities do not all come up for renewal at the same time, as failure to roll-over debt could prove disastrous. Fortunately the capital markets are increasingly active and other longer-term funding sources such as retail bonds and US private placements are now making serious headway out of the crisis.

Diagram 1: All things cash

Source: Lloyds Bank, Financial Risk Advisory

How much and when

The skill and judgement of the treasurer rests in understanding how much, and when, funding is needed and the most appropriate instruments to use at the point of execution. For a cash generating business, the treasurer must additionally identify the value that cash has if it is retained as a liquidity buffer, to what degree that value may change over time and whether it may be better to re-deploy that cash.

Houghton notes that, historically, hanging on to cash has been seen as a buffer in many industry sectors. For those that hoard cash without considering the true impact of their action, he has a word of warning: “low returns from short-term cash investment can act as a drag on profitability”.

A corporate that has borrowed will face a ‘cost of carry’ on stockpiled cash simply because the rate of return on that cash, when invested short term eg overnight, will possibly be much lower than the cost of borrowing. The downward pressure on yield on short-term (less than 90-day) investments caused by bank regulations such as ILAS in the UK and the Basel III initiative, will maintain this for some time to come.

For corporates that have large cash balances, traditional finance theory suggests that money should be returned to investors, in the form of a dividend or share buy back, or used to repay longer-term debt (and save interest costs). However, given the unpredictable nature of the markets and uncertainty of future credit availability, should the corporate then need this cash, going back to investors with a cash call or rights issue may appear to be bad planning, or worse, the corporate may not be successful in raising the amount required.

An alternative option, says Houghton, is to retain the cash in the business, but move it out of short-term investments into those that potentially yield more – term deposits, longer-term government securities or high quality corporate bond portfolios – effectively creating an investment fund whose liquidity and risk can be defined to improve yield but not by unduly taking more risk to capital or sacrificing too much liquidity. Since the credit crisis, treasurers still take the view that, even if they only need half the cash they are sitting on they are only prepared to invest short, ‘just in case’. This, he comments, is often because they have not fully considered how they may use their cash to best advantage. “Treasurers may not have thought about optimally placing their cash because the reward of more yield may not counter the downside of tying up ‘too much’ cash and then finding they need it.”

Calculating excess and adding stress

Industries that have long-term liabilities, such as the insurance sector, have to make their investment portfolio work in order to meet their continuing obligations (often setting premiums according to anticipated returns). Corporate treasurers seemingly do not face the same pressure and thus may not see their cash in terms of investment opportunities. “But, in order to optimise the use of cash in the ‘investment option’ that Lloyd’s are proposing, they will now need to”, says Houghton. To determine how much could be deployed in such a way, a treasurer must start by calculating the corporate’s total cash liquidity requirement over the short and medium term (considering any RCFs or other credit facilities that act as a cash substitute for liquidity purposes) and then determine whether they currently have cash that is in excess of this requirement that they could invest for strategic purposes.

Internally reviewing and planning the sources and uses of cash both operationally and strategically may require the input of many functions because it may involve consideration not just of cash generation but also of future strategic planning elements such as M&A activity, debt re-financing, or major capital expenditure.

Having calculated how much cash will be generated and needed over a given period, it is essential then to stress-test the results to see the effect of volatility in the underlying assumptions used to generate the future cash balance of the corporate. This could be caused by, for example, lower than expected revenues, higher than expected costs, unexpected capex or worsening of working capital requirements. The approach will also need to take into account the likelihood of these events happening, according to certain assumptions and based on historical internal data (such as the historical range of actual costs, revenues and capex) and external data (including interest and FX rates or commodity price projections).

By using the worst case level in the possible range of these factors, a projection of the corporate’s ‘worst case cash balance’ over time can be constructed, which can then be used to determine how much of the current cash balance can be invested and for how long. “The idea”, says Houghton “is that the corporate does not need liquidity for the term of these investments and so can invest in less liquid investments and for a longer time horizon to improve returns with greater confidence, a confidence brought about by having a better liquidity model of the business”.

Modelling projections

This approach, therefore, not only requires an understanding of how much of the current cash balance is needed and how much can be invested but, says Houghton, from a planning perspective, of how much might be needed and the extent to which other medium-term factors such as future M&A, debt needs and capital expenditure need to be planned in. A corporate may typically build a cash flow forecast model to combine the future sources and uses of cash within the business into a projection of the future cash balance, which is then used by treasury to determine its liquidity management approach.

As described above, Lloyds seeks to take this process a step further by stress testing and factoring in a broad range of market uncertainties. “If the corporate has debt linked to interest rates, foreign currency earnings or inflation-linked income, for example, these are elements linked to actual market factors which we can model and hedge,” Houghton says. “At Lloyds Bank, we don’t just look at sources and uses of cash but also how financial market movements can affect a business.”

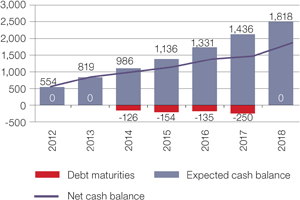

Chart 1: Projecting the future expected cash balance

Source: Lloyds Bank, Financial Risk Advisory

For many corporates this exposure to the markets is seen through their debt. If debt is fixed then it is not a problem, but if it is linked to LIBOR, for example, this is an explicit link to interest rate levels. “It could be argued,” admits Houghton, “that interest rates may increase because the economy is improving and so some of the market links a corporate is exposed to may be seen as benign or correlated with revenue and so they wouldn’t necessarily hedge them”. But, he continues, “uncertainty over the next five years in the cash and business cycle might equally stem from unknown elements which a business may wish to tie down”. For foreign currency exposures, for example, Lloyds can advise a business on how to reduce uncertainty so it can make its predictions with greater accuracy.

By building an element of stress into the forecasts it is possible to determine the minimum amount of cash over time that a corporate may need (its Minimum Liquidity Term Structure), Houghton explains. “Any cash currently held or forecast to be received in excess of this requirement over a period of say 12 months, can be treated as reserve cash and beyond that as strategic cash.”

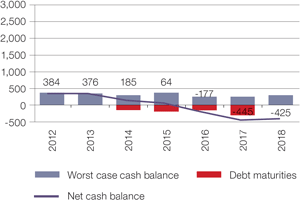

Chart 2: Projecting the future worst case cash balance

Source: Lloyds Bank, Financial Risk Advisory

The excess cash forms the Investable Cash Balance and, using the stressed cash flow forecast, it is possible to determine a precise term structure for the investable balances within the reserve and strategic cash pools (referred to by Houghton as the Investable Cash Term Structure) – without losing liquidity cover. “If a corporate wants excess cash, there is no reason why it can’t layer its investment over a given period to stagger the liquidity to earn a bit more on it,” notes Houghton.

The holistic approach to cash

If there is no short-term need for cash then why hold on to it? If the modelling and projection has been executed diligently and any potential for loss is perhaps three or four years out, then that excess cash could be better employed in a less liquid but higher yielding investment portfolio.

As has been made clear, cash is king in the eyes of many, but it can also be a drag on the profitability of the business; a RCF’s cost only ramps up when it is used, but there could be an issue of availability when it is rolled over – what is offered now may not be available in the future. Is there a formula to calculate the balance? Realistically, Houghton concedes that there are too many variables in terms of economic factors, business sector and individual corporate needs, risk appetites and so on to be able to offer an off-the-shelf solution. What can be delivered though, he says, is an holistic view of liquidity management within an individual business that takes into account internal and external factors, using historical data, assumptions and projections. Lloyds Bank’s Financial Risk Advisory Methodology is based on this model and can be used by treasurers as part of the financial planning process.

Ultimately, there is no one-size-fits-all liquidity solution that balances cash, debt and investment because no two companies are exactly alike. Of course, if the money runs out, all businesses meet the same end, but by knowing how much total liquidity is required and how to divide and balance its own cash and debt, a corporate will be in a far stronger position going forward.

✓ Summary checklist for corporate treasurers

What is your overall cash and liquidity management strategy?

What is your existing treasury policy/investment mandate and approval process?

How are cash balances maintained?

What liquidity facilities do you have?

Are there any constraints on your cash investments?

Are there any specific investments required? Is future capital expenditure planned?

Do you have any tax losses brought forward?

Are you planning to repay debt in the near future?

Do you plan to undertake any capital markets activity where raised funds can be invested in the near term?

Which wider market exposures (eg. FX, inflation) do you have and may wish to hedge?

What is your dividend strategy?

Lloyds Bank

Stephen Houghton, Director, Financial Risk Advisory

Stephen Houghton works in Lloyds Bank’s Financial Risk Advisory team and has worked in financial services for 22 years, covering roles in equity derivatives sales, ALM and Enterprise Risk Management advisory for corporate and institutional customers.

Lloyds Bank Commercial Banking provides comprehensive expert financial services to businesses of all sizes, from start ups, through to small businesses, mid-sized businesses and multinational corporations. These corporate clients range from privately-owned firms to FTSE 100 PLCs, multinational corporations and financial institutions. Maintaining a network of relationship teams across the UK, as well as internationally, Lloyds Bank Commercial Banking delivers the mix of local understanding and global expertise necessary to provide long-term support and advice to its clients.

Lloyds Bank Commercial Banking offers a broad range of finance beyond just term lending and this spans import and export trade finance, structured and asset finance, securitisation facilities and capital market funding. Its product specialists provide bespoke financial services and solutions including tailored cash management, international trade, treasury and risk management services. Its heritage means it has an unrivalled understanding of business needs and a proven track record of supporting businesses across the sectors and regions. Taking a relationship approach, it provides support to its clients throughout the economic cycle.

Lloyds Bank plc. Registered office: 25 Gresham Street, London EC2V 7HN. Registered in England and Wales No. 2065. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority under registration number 119278.

This article was sponsored and issued by Lloyds Bank plc.

Please enter the email that you signed up with below. If your email is

connected to a member account, we will send you a reset link.

This website uses cookies and asks for your personal data to enhance your browsing experience. We are committed to protecting your privacy and ensuring your data is handled in compliance with the General Data Protection Regulation (GDPR).