The coming year will no doubt bring with it some money market fund (MMF) proposals from the US Securities and Exchange Commission (SEC), as well as further reforms in Europe, in particular regarding constant net asset value (CNAV) MMFs.

In addition to these reforms, MMFs are battling myriad other difficulties: the European sovereign debt crisis, concerns about the stability of European banks’ credit quality, negative yields in Europe and fiscal cliff remnants in the US. Furthermore, the Federal Deposit Insurance Corporation’s (FDIC) unlimited deposit insurance coverage expired on 31st December 2012. If these vulnerable deposits are reallocated into MMFs and money market securities, it may push short-term investment rates down even further.

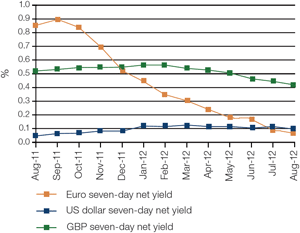

Managers of MMFs are already struggling to maintain investments that deliver positive returns despite low interest rates. Prime MMF sector gross yields have fallen from more than 0.75% per annum in January 2012 to around 0.13% per annum in December 2012. In an industry where liquidity and stability of investments normally trumps yield, tough market conditions are forcing fund managers to dedicate their efforts to generating yield against all odds. However, with returns on short-term MMFs trending lower and the supply of suitable high quality issuers declining, options are becoming increasingly limited.

The MMF industry is no doubt preparing itself for upheaval and modification with the introduction of inevitable reforms. But the global financial arena is also shaping the structure and various management approaches to funds and certain portfolios. The MMF environment has become quite a different one to the investment arena it once was.

Reforms and ratings

Ever since the Reserve Primary Fund ‘broke the buck’ (fell below one dollar a share) in September 2008, financial market regulators have stressed the need for additional MMF regulations. In 2010, the SEC adopted revisions to the regulations to enhance the resilience of MMFs. But when former SEC Chairman Mary Schapiro announced in August 2012 that the majority of SEC commissioners did not support her reform proposals for MMFs and therefore was not proceeding with a vote to solicit public comment, the money fund industry was suitably relieved. However, subsequent public comments indicate that additional reform is almost certain – the date that this is set to happen is rather more unpredictable. But by deciding not to hold a vote, Schapiro effectively handed the issue to the Financial Stability Oversight Council (FSOC).

Alastair Sewell, Director, Fund and Asset Manager Rating Group at Fitch, believes that the pace of MMF reform could accelerate significantly in 2013. “In the US, SEC Commissioner Luis Aguilar recently voiced his support for a floating NAV structure for MMFs, which makes it more likely for this option to be carried out by the SEC,” he says.

“This follows the FSOC proposals in November 2012 for MMF reform. These proposals included amendments to the existing MMF structure such as a floating NAV; a stable NAV with NAV buffer and “minimum balance at risk”; and a stable NAV with NAV buffer and other measures.” The public commentary period on the FSOC proposals, which was to close on 18th January 2013, has been extended to 15th February “to allow the public more time to review, consider and comment on the proposed recommendations”.

MMF regulation is also picking up worldwide. The International Organisation of Securities Commissioners (IOSCO), which the SEC is a member of, has published its policy recommendations for improving oversight and regulation of the ‘shadow banking’ industry (which includes MMFs). These recommendations are intended to complement existing regulatory frameworks where the IOSCO believes there is still room for further reform – including the US. In addition, the European Commission (EC) under the Undertakings for Collective Investments in Transferable Securities (UCITS) VI report is considering whether CNAV funds should be subject to additional regulations, such as capital buffers.

Sewell adds: “The European Systemic Risk Board (ESRB) is considering the report published by IOSCO in October last year that suggests that the global MMF industry should be further regulated to reduce systemic risk. Specifically, IOSCO recommends additional safeguards for those MMFs using amortised cost accounting and offering CNAV per share. Furthermore, IOSCO recommends a conversion of CNAV MMFs to floating NAV MMFs through limited use of amortised cost accounting only for assets maturing below 60 days.”

Fitch’s rating criteria is applicable both to floating NAV and CNAV MMFs. Under its Principal Stability Fund Rating methodology, Standard and Poor’s (S&P) also currently rates MMFs exhibiting a variable NAV as well as CNAV MMFs, according to Françoise Nichols, Director, Fund Ratings and Evaluations at S&P.

“We will monitor and review what impact further regulation of the MMF sector in the US, Europe and elsewhere may have on S&P rated MMFs. If CNAV MMFs were to become a less attractive investment opportunity (as a result of reforms), some investors may decide to move their investments to less regulated segregated managed accounts, or to directly transact in less diversified and liquid instruments such as bank deposits and/or repurchase agreements,” he says.

Recently, major providers have taken steps to provide more transparency in their money funds, disclosing values on a daily basis rather than monthly. Following the announcement by Goldman Sachs of its intention to disclose values of their funds each day, J.P. Morgan, BlackRock and Dreyfus said they will also list NAVs each day. Seen by many as a positive development, daily disclosures may also make investors more likely to pull money out as a result of seeing minor discrepancies.

Alternative approaches

In the past 12 months, euro-denominated funds have faced the brunt of the harsh economic conditions, prime funds and government funds have been withdrawn. There have also been numerous downgrades of European financial institutions and sovereign issuers. As a result, some funds have diversified into issuers outside of Europe, albeit in smaller amounts and for reduced maturities.

Amid this unprofitable environment, numerous MMF providers announced soft closes restricting new accounts and placing varying restrictions on new investment from existing clients. The soft closes were introduced in the summer of last year following the European Central Bank’s (ECB) move to lower its deposit rate facility to 0% with an aim to protect MMF investors from dilution risk, according to Nichols, but some have since modified their restrictions. “We see this trend evolving and predict funds reopening to new investors, since dilution risk has reduced, as higher yielding assets held by MMFs have matured.

“More recently fund providers have been looking at ways to handle negative yield for euro denominated MMFs. Certain providers have already announced fund restructuring involving a share cancellation mechanism to compensate negative yield and continue to maintain a CNAV,” he says.

In response to the prevailing low yields and a risk of deterioration of MMFs’ NAV, J.P. Morgan Asset Management (JPM AM) is one such provider that has elected to employ unconventional measures. The investment firm’s board of directors decided to restructure its euro-denominated MMFs, making share class amendments and updating the investment objectives for both the J.P. Morgan Euro Government Liquidity Fund and the J.P. Morgan Euro Liquidity Fund.

Sewell recognises the proactive approach European MMFs have taken to deal with the unfavourable future and offset the potential impact of negative rates on NAV. “Negative MMF yields stemming from the short-term market rate environment would not be a negative rating factor per se for Fitch-rated MMFs, including for those rated at ‘AAAmmf’,” he insists.

“Some fund complexes have already implemented new share class structures to pass on potential negative yields to fund investors. We expect several others to follow suit in the coming weeks. The essence of the negative yield distribution mechanism is based on keeping the NAV per share stable at the initial subscription price per share. Thus, if a fund suffers a negative overall yield then the fund redeems pro-rata investor shares such that the NAV per share remains stable (ie the number of units (shares) in the fund can vary, but the value per share remains stable at one).”

The introduction of flex shares is designed to ease investors’ accounting and tax issues through maintenance of share values at par. Yet the net result is that investors lose capital and this, according to some market experts, is at odds with the AAA ratings definition (Moody’s cites the ability to meet the objective of preserving capital as one of the key measures). That said, it can be argued that a MMF is a lower risk proposition than direct investment and that yields, although potentially negative, should compare favourably with market returns on similarly high-grade and liquid investments.

According to a Moody’s whitepaper, changing the fund’s structure is credit positive for JPM AM as it will enable it to operate in both a negative and positive yield environment. “Such flexibility will empower JPM AM to retain current investors and attract new assets under management (AUM), resulting in higher MMF revenues,” says the report.

MMF managers feel the strain

Elsewhere, the burden on providers continues to ramp up. With the pressure to achieve yield while remaining risk averse, portfolio managers have placed heavier reliance on barbell strategies. In the US, MMFs are expected to attract new assets as a result of the end of the FDIC’s insurance on bank deposits. This may place pressure on yields offered by US MMFs, according to Nichols. Furthermore, some generalist fund providers are focusing on distributing product generating higher fees than MMFs, resulting in further product rationalisation and consolidation in the industry.

Chart 1: Net yields for Standard & Poor’s ‘AAAm’ seven-day money market fund 2011-2012*

“The extremely low level of yield for euro-denominated MMFs has led some providers to offer higher yielding alternative products to their investors, which may be less liquid or riskier than ‘AAAm’ rated short-term MMFs,” he explains. The declining yield environment, reduction of eligible supply and tightening rating requirements have each, to varying degrees, impacted and accelerated the level of consolidation in the euro Institutional Money Market Funds Association (IMMFA) space, which represents European AAA rated MMFs, according to Mark Stockley, Managing Director, Head of International Cash Sales at BlackRock. “Consolidation to date has principally occurred with those providers who had smaller sized funds, limited distribution and have found managing their euro funds challenging.”

This theme of consolidation is a concept Sewell agrees with, mainly among MMF managers that are sub-scale and do not derive synergistic benefit from MMF offerings. “Niche MMF players are already under material profitability pressures in this prolonged, ultra-low interest rate environment. The impact of low yields on fund manager fees may cause some managers to reconsider their strategic commitment to the cash management industry. “In instances where MMF managers apply management fees, waivers are likely to persist, especially for US dollar-denominated MMFs, to maintain a positive yield to investors. We would question how sustainable these fee waivers are especially for small to mid-size MMF complexes,” he says.

And while Mike Hughes, Global Head of Fund Services, Deutsche Bank, doesn’t expect the larger players pulling back from the MMF market, he also notes that: “total expense ratios (TERs) are under severe pressure given the interest rate environment. Few MMF managers can really afford to absorb any fees, yet are being forced to subsidise charges from banks, administrators and custodians to protect TERs.”

An ongoing battle

The MMF sector would no doubt benefit from the resolution of the European sovereign debt crisis. A likely by-product of the resolution of this issue would be an increase in issuance of MMF-eligible securities due to the potential improvement in economic activities. According to Sewell, Fitch expects the limited supply of high quality short-term assets to continue to be one of the major challenges for the MMF sector in 2013, especially those portfolios denominated in euro and sterling. Nonetheless he remains positive for the future of the MMF industry and Fitch’s global outlook for MMF ratings in 2013 is stable.

“We see a few interesting trends: first, towards collateralised exposures (repo, ABCP); and second, to non-traditional geographies – we have seen an uptake in exposure to issuers from Asia in particular, although outside of US dollar denominated funds issuance levels will limit uptake in MMFs. We would expect liquidity levels to remain high in 2013, but weighted average life (WAL – used to measure credit risk)/weighted average maturity (WAM – used to measure interest rate risk) will increase slightly as funds selectively add longer dated exposures to higher quality issuers,” he says.

As the regulation debate on MMFs continues, market participants will likely present alternative ideas as they look for common ground on which to operate and aim to maintain a thriving fund industry. However, achieving sustainable yield and currency stability in the volatile financial climate will also play a major part in defining a new, improved fund environment. The question is: will the arduous search prove successful enough to restore investors’ confidence in MMFs, and thus stabilise the future of the industry?

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.