If you are a corporate pension fund trustee, the chances are that your exposure to alternative assets has increased considerably in recent years.

Despite a challenging investment environment, in which large returns have become ever scarcer, alternative investment managers have continued to attract record levels of capital, research shows.

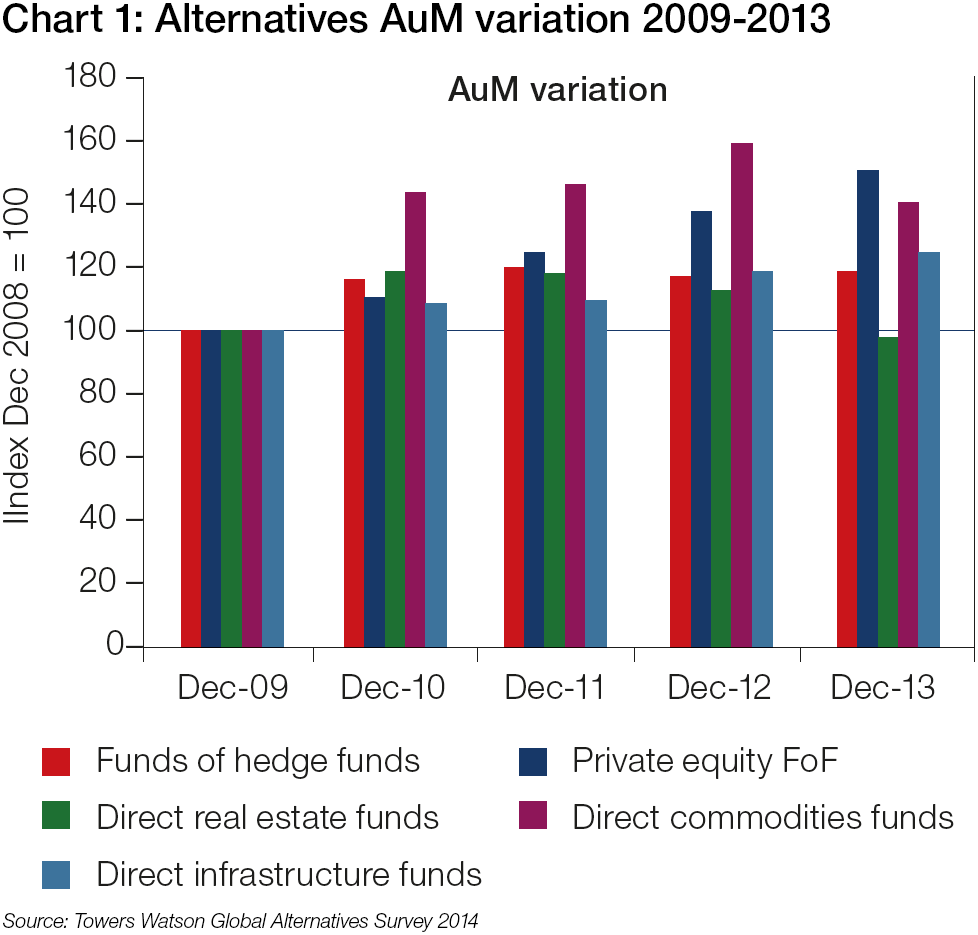

The 2014 Global Alternatives Survey by investment consultants Towers Watson shows pension fund assets held by the top 100 asset managers that deal with pension funds increased by over 5%, from $1.16 trillion in 2012 to $1.22 trillion 2013. Corporate pension funds have been big contributors to this growth. Like other institutional investors, they are continuing to diversify their portfolios away from traditional growth asset classes, such as equities, and into the world of alternatives, where they are able to insure their portfolios against the volatility of equities. It is a trend which has gathered pace since the financial crisis.

Investment trends will come and go, of course. But as tempting as it is to dismiss the recent shift in favour of alternatives as little more than a fad, the reality is that these investment tools are not simply growing in popularity; they are, in fact, becoming increasingly part of the mainstream investment landscape.

Already, most of these assets are such a common feature in investment portfolios that most asset managers will tell you that they no longer even think of them as ‘alternatives’, they are just another vehicle that can be used to secure stable, inflation-protected cash flows over long durations.

Not only does interest in alternatives continue to grow, but the range of alternative assets is also broadening. Direct real estate – the classic alternative asset – may continue to be the most popular type of investment for the time being, but we are also seeing increasing interest in other, formerly peripheral alternatives, such as infrastructure and distressed debt, in recent years too.

Beyond yield

To understand why alternative assets have become more prevalent in corporate pension fund portfolios in recent years, it would be helpful, perhaps, to take a closer look at the different characteristics of these tools and at what pension fund trustees hope to accomplish when they invest in them.

Corporate investors are not only changing the weighting they are giving to alternatives within their pension portfolios – they are also taking different routes to gain access to the asset class. Traditionally, most corporate investors make their first allocations in alternatives via the “fund of funds” route. By using a fund of funds, a professionally managed investment vehicle that allocates capital towards multiple underlying managers, investors are able to get instant diversification across sectors and geographies. There is a catch, however. Using a fund of funds also means the investor gets, in the words of Julian Brown, Director in the Investment Consulting team at JLT Employee Benefits, “a double layer of fees.”

“You have the underlying fees of the funds themselves first of all,” he says. Then, if anybody is doing anything over the top – allocating between, performing operational due diligence, consolidated reporting – there will be an additional charge on the top. “In the old days, it would be two and 20 at the underlying, and then one and ten on the top. That would mean there is a 2% management fee and 20% of all your profits are taken by the underlying managers, plus a 1% management charge and 10% performance fee by the fund of funds manager.”

Chart 1: Alternatives AuM variation 2009-2013

Source: Towers Watson Global Alternatives Survey 2014

The weight of such fees on investment portfolios is not insignificant. It means that investors require, at the very minimum, a 5% rate of return just to cover their fees. Accordingly, most investors go into alternatives with the expectation of high returns and, in the good times, that was exactly what they got.

In the early years of the new millennium, Brown was working as the investments officer at the UK’s Nottinghamshire County Council pension fund, when he first began investing funds in private equity. At that moment in time, thanks to the buoyant economic backdrop, investors like Brown had return expectations for alternatives that were very often in the “high teens”.

“That sounds incredible now, doesn’t it?” he exclaims. “But that’s why people traditionally wanted to be in alternatives. It was always thought of as the sparkle in the portfolio; the investment which will give you some extra returns.”

Look around and you won’t see much in the way of yield these days, however. In the period post financial crisis, those stratospheric returns have all but evaporated as central banks around the world cut interest rate benchmarks to record lows and embarked on programmes of quantitative easing. In today’s low yield world, investors are naturally less prepared to accept the extra layer of fees above the individual funds, and are exploring alternative routes, such as single-strategy funds, for example. “I think its forced investors to become a bit savvier, and so those fund of funds fee structures – they are just not prepared to accept them now.”

Even if the days when turbo-charged performance was the main attraction are now gone for good, that has evidently done little to dampen the growth of the asset class. Investors today are turning to alternatives, for the most part, because they want consistent, risk-adjusted returns that insure them against volatility in other asset classes; those ever mercurial equities in particular. If they are able to find that protection in an asset class that also mitigates the risk to their portfolios of price inflation, then so much the better.

“That is why we are seeing so much interest in alternatives such as infrastructure, forests, and some of the real assets,” says Olivier Lebleu, Head of International Distribution at the investment fund Old Mutual. “It’s because they tend to mean a low notional investment upfront, coupled with regular inflation proof cash-flows.”

What are the ‘alternatives’?

The label ‘alternative investment’ immediately raises the question: alternative to what? Most asset managers agree that an alternative investment is any asset that is not one of the traditional asset classes such as equities, bonds or cash.

As such, alternative investments are a very broad asset class that includes under its umbrella a set of products ranging from hedge funds and private equity, to infrastructure and private real estate.

Here we take a quick look at what each of these investments has to offer:

Private real estate

Globally, the real estate market has recovered reasonably strongly, after taking a hit from the subprime mortgage debacle. In Europe, it remains the main attraction in the alternatives space, with investors now said to be holding $5.3 trillion worth of real estate assets across the globe. There has been a small shift of capital into other areas, however. “I am seeing a rise in allocations beyond property, and I’m sure many of my peers would say the same,” says Old Mutual’s Lebleu.

Hedge funds

The key thing about hedge funds is that they are able to short-sell. This is attractive to pension investors since it should mean that the funds are able to secure some form of return, even in a bear market.

“Investors understand that equity markets go up and down, but what you want from a hedge fund is a stable, absolute return profile,” says JLT’s Brown. In the hedge fund space there are, of course, a range of different strategies for investors to choose between, which can be levered to meet higher return expectations. “But even those are relatively modest compared to the old days of ‘corporate raiders and red braces’,” he says.

Infrastructure

Infrastructure has been an increasingly common target for investment in the UK in recent years. There are two drivers behind this trend, says Old Mutual’s Lebleu. On the supply side, the need for private funding has grown as the UK government, constrained by fiscal pressures, has begun to step back from the financing of large infrastructure projects. Then, on the demand side, recent years have seen companies accumulate huge pools of capital that have a need for cash flows that are steady and inflation proof. “Given that governments have an incentive to push this agenda, we have seen infrastructure come to the forefront of discussions in the UK, relative to other asset classes such as forestry,” says Lebleu.

Commodities

“Commodities tend to be quite a specialist asset class for investors,” says JTL’s Brown. If a corporate is already familiar with a particular commodity – an energy company that trades in crude, for example – it certainly helps, as understanding the complexities of the asset class is often the first hurdle.

“The thing with commodities – and all alternatives for that matter – is that there has to be an adequate level of trustee understanding before an allocation can be made,” says JLT’s Brown. “So if you are a trustee for an energy company, you may be quite familiar with the spot and forward pricing for commodities, and if so you would know there is often a difference that can be traded. Trustees should not invest in anything they do not understand, thus it is helpful for an understanding to already be there when we come to provide specific alternative asset class training for trustees.”

The regulatory challenge

Like most corners of the financial universe, the alternative investment industry has had to manage significant regulatory changes in recent years. In Europe, particularly, we have seen the deadline for compliance with the EU Alternative Investment Fund Management Directive (AIFMD) pass in July this year.

The new directive requires all managers based and managing funds in Europe to seek official authorisation once they pass a certain threshold. By the same token, funds that are outside the EU but plan to market to institutional investors inside Europe will have to have a number of organisational and transparency controls in place, providing investors, for example, with pre-investment disclosures and, throughout the duration of the investment, keeping treasurers informed about any material changes on risks, leverage and investment strategy.

For the corporate pension fund with funds in alternatives, building a more open and transparent market can be only a good thing, right? “It is indeed raising the bar on transparency,” says Heleen Rietdijk, KPMG’s global leader of AIFMD tells Treasury Today. Corporates and other investors now get the information that they need straight away and without any hassle. That will certainly help to reassure investors that their funds are being managed in the correct way.

For that reason, investors have been largely supportive of the regulation. That does not equate to wholesale approval of each and every detail, however. In particular, trade bodies representing the investment industry, namely the Alternative Investment Association (AIMA), the Investment Management Association (IMA) and the National Association of Pension Funds (NAPF) have voiced concerns around certain aspects during the consultation process. In 2010, for example, the three agencies wrote a joint letter to MEPs asking for leniency on the “third country” proposals that they believed threatened to effectively restrict investors to their domestic markets. “Compromise amendment ‘N’ is, we fear, unworkable,” the trade bodies wrote. “In practice it will not provide access for non-EU funds and fund managers, but will instead ban European investors from investing overseas.”

Thankfully for investors the words of the trade bodies did not fall entirely on deaf ears. Earlier this year, a compromise was proposed which would allow non-EU fund managers to obtain the same pan-European marketing passport as their European-based counterparts. The proposal is currently under review with the European Securities and Markets Authority (ESMA) and, if positive advice is provided, will be sent to the European Commission (EC) to become enshrined in EU law.

However, other concerns are not likely to be resolved as swiftly. The growing disparity around how alternatives are regulated in other jurisdictions is perhaps the biggest issue, says Rietdijk. In the US, regulation of alternatives is not as strict on certain organisational aspects such as the appointment of a depositary, the implementation of a remuneration policy and structuring a risk management framework as it is in the EU. One could argue that the steps taken by the EU are a positive, given the turmoil we all know can result from taking a too ‘light touch’ approach to regulation. Yet, as Rietdijk stresses, the authorities should still be very careful in that they do not “overextend our regulation to the extent that it makes it difficult for European fund managers to have access to the US market, because they are too expensive.”

Rietdijk concludes with a warning that could be equally applicable in a multitude of other areas in the financial services ecosystem. Regulation, when it becomes overzealous, often ends up doing more harm than good. “All of this compliance can, of course, come with a cost.”

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.