All change: winners and losers emerge in the fight for global FDI

Published: Jan 2019

US tax reforms and trade disputes have led to a slump in global foreign direct investment but as corporates revise their investment strategies in the light of the changing operating environment, some regions are experiencing a boom in investment.

The last few decades have seen foreign direct investment (FDI) become a vital part of the armoury corporates can deploy to maximise returns on their investments. By securing controlling interests in foreign assets, firms can, for instance, rapidly acquire new products and technologies, sell their existing products to new markets and reduce production costs.

Governments too have been very keen on FDI, seeing it as an effective means of creating jobs and improving economic growth. That corporate-government consensus has reigned since at least the 1970s and resulted in FDI flows globally soaring from little over US$10bn in 1970 to well over a trillion dollars now. These flows, comprising as they do cross-border M&A activity, intra-company loans and investments in start-up projects, are also an indicator of growth in corporate supply chains and trading relationships and, more broadly, a powerful bellwether of globalisation.

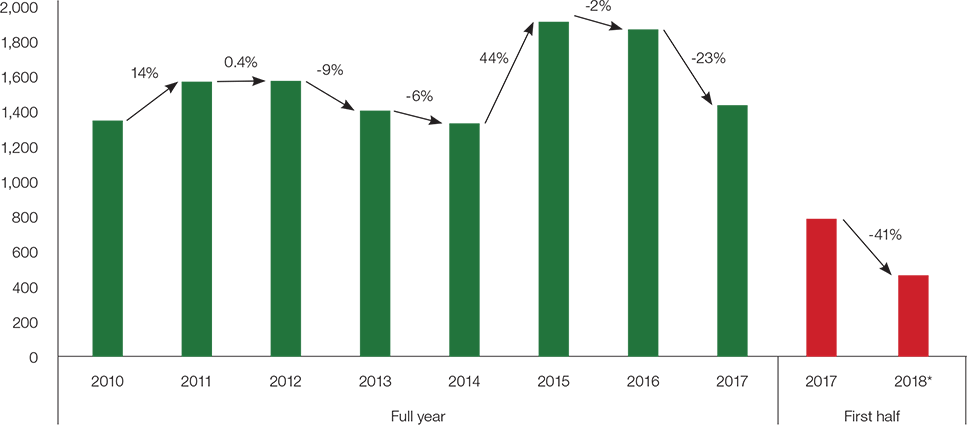

New data from United Nations Conference on Trade and Development (UNCTAD), however, shows that FDI worldwide is on the decline, with the US tax reforms introduced at the end of 2017 in particular resulting in a dampening of global investment activity. According to the data, FDI globally slumped 41% in the first six months of 2018 to US$470bn — the lowest since 2005 – from US$794bn in the same period in 2017.

UNCTAD says the big fall in FDI flows is mostly due to US tax reforms having encouraged big firms there to bring home earnings from abroad – mainly from western European countries. Trade disputes, notably the US-China tariff war, are proving to be another drag on flows, with the accompanying anti-trade rhetoric and protectionist stances further undermining investor confidence and forcing companies affected to review their investment strategies and locations of their operations.

James Zhan, Director of Investment and Enterprise at UNCTAD, is clear that the fall in FDI flows is being “driven more by policy than the economic cycle”. He points out that the agency had warned in early January that there was about US$2trn of stock in the form of cash or reinvested earnings of retained earnings outside the US that could be repatriated in some form following any wholesale tax reform: “And indeed, that is happening. We have seen that outward FDI from the US was US$147bn last year but turned to a negative US$247bn already this year.”

Winners and losers

Drilling down from the headline figures from UNCTAD’s latest Investment Trends Monitor, however, reveals interesting regional variations. The fall in first half flows has mainly impacted the richer nations. Europe declined by a hefty 93%, the most notable fallers being Ireland, down US$81bn; and Switzerland, down US$77bn. North America retreated by 63%, with US inflows diving 73% to just US$46bn.

At the same time, however, developing economies saw FDI flows decline only 4% over the first half of 2018 to US$310bn versus the same period in 2017. This grouping includes developing Asia, where flows declined 4% to US$220bn, mainly due to a 16% decline in investment in East Asia. China bucked the wider trend most though – it was the largest recipient of foreign direct investment in the first half, attracting more than US$70bn, indicating there is still significant long-term investor confidence in the country.

FDI to the “transition economies” – comprising mainly the former Soviet Union and Eastern bloc countries of Europe – meanwhile fell by 18% over the first half to an estimated US$25bn, mainly due to a drop of flows to natural resource rich countries of the Commonwealth of Independent States (CIS).

Elsewhere, Latin America and the Caribbean saw a 6% drop in investment, as uncertainty over upcoming elections in some of the major economies there were offset by higher commodity prices. In West Africa, UNCTAD data indicates a 17% fall in investment in the first half of the year, from US$5.2bn to US$4.3bn.

Grand for greenfield

The global decline in FDI flows over the first half contrasted with trends in cross-border merger and acquisitions (M&As) and greenfield investments. M&A sales managed to stay steady over the period at US$371m but investments in greenfield projects jumped 42% to US$454bn compared to same period in 2017.

The upturn in greenfield outlay by corporates is especially encouraging as this strand of investment is generally regarded as a strong indicator of future FDI trends. Greenfield typically involves companies building physical operations in a foreign country from scratch, for example by establishing a foreign sales office, manufacturing facility or an R&D centre. It is therefore the ultimate level of FDI, it’s riskiest form: if political, economic, currency or commercial risks materialise in the host country the investment cannot suddenly be relocated. But with the greenfield investing company typically having full authority over the operations and profit associated with the investment, the rewards can be substantial.

Drilling down into FDI flows across Europe shows clearly the big impact that repatriations by US parent companies of foreign earnings have had. Compared to the first half of 2017, US FDI outflows to Europe fell by a hefty US$136bn to result in a net divestment of US$49bn over the same period in 2018.

Outside of Europe, US FDI flows to “Other Western Hemisphere”, including offshore financial centres in the Caribbean fell by US$163bn.

But repatriations of accumulated foreign earnings were not the only explanation for the drop in global investment flows, says UNCTAD, pointing out that the 72% drop to just US$46bn in US FDI inflows came despite the potential stimulus effect of tax reforms on investments there by foreign multinationals. Uncertainty about the implementation details of the tax reforms over the first half, combined with uncertainty about US trade relations and fears over its more stringent investment screening procedures could all have been contributing factors, says the agency.

Boom for Southeast Asia

The big regional divergence in FDI flows, with the richer nations impacted by US repatriations and developing countries remaining broadly stable, meant the share of the latter in global FDI flows increased to a record 66%. Half of the top ten host markets for FDI continue to be developing economies including China, India and Hong Kong.

Even within Asia though there were notable variations in flow. While China became the largest global recipient of FDI, flows to Hong Kong fell to US$34bn – half the level it received in the first half of 2017.

Global FDI flows and growth rates, 2013-2017 and 2017: H1-2018: H1

(Billions of US dollars and per cent)

Source: UNCTAD

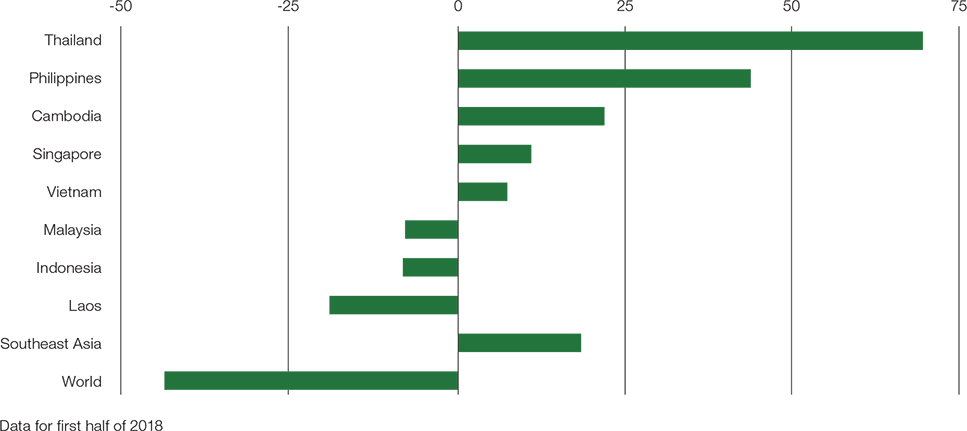

Most interestingly though, flows to Southeast Asia and South Asia rose by a strong 18% to US$73bn and 13% to US$25bn respectively, with manufacturing inflows a major feature.

In Southeast Asia, Singapore was the big attractor, securing US$35bn despite it suffering profit repatriations by US multinationals. Elsewhere in the South East, Indonesia secured US$9bn and Thailand US$7bn. In South Asia, India attracted US$22bn of FDI flows, contributing to the subregion’s 13% rise in FDI in the first half of the year.

The FDI boom for Southeast Asia has attracted considerable attention, with analysts saying the region is proving the biggest beneficiary of the intensifying trade war between the US and China, with the spat prompting companies to shift production to the area.

According to analysts at Maybank Kim Eng, the investment banking arm of Malaysia’s Maybank, even smaller economies across the region have experienced big FDI inflows over the course of the current year. Vietnam, for example, saw manufacturing inflows jump 18% in the first nine months of 2018, driven by investments including a US$1.2bn polypropylene production project by South Korea’s Hyosung Corporation. In the Philippines, net FDI into manufacturing soared to US$861m in the same nine-month period from US$144m a year earlier.

“The US-China trade war may be attracting more firms to set up in ASEAN countries to circumvent the tariffs,” Maybank economists Chua Hak Bin and Lee Ju Ye said in the note. “Companies in sectors such as consumer products, industrial, technology and telecom hardware, automotive and chemicals have indicated interest in Southeast Asia.”

Southeast Asia, it seems then, has become an alternative base for firms looking to avoid the fallout from the US-China trade war. American companies are by far the most active in China and a survey of 430 of them by the American Chamber of Commerce (AmCham) in China and Shanghai found 60% have been hurt by the tariff war between the two countries. Profit losses, high manufacturing costs, increased prices and lower product demand were among the biggest impacts cited by the companies. One third of those polled by AmCham China in late August and early September said they have or were thinking of moving production sites away from the country.

According to Maybank, notable arrivals to Southeast Asia as a direct result of the tariff wars include Harley-Davidson Motorcycles, which shifted part of its operations in the US to Thailand after closing a plant in Kansas City. Electronic giant Panasonic closed its US plant in early 2017 and switched to consignment production and exports from Malaysia. Shoes and accessories group Steven Madden has been shifting production of handbags to Cambodia from China.

Elsewhere, Delta Electronics, which supplies power components to the likes of Apple and Tesla is looking to de-risk from the current tariff war – and potential future ones – by spending US$2bn to purchase a Thai affiliate. The move would enable Delta to expand production outside China to territories such as India and Slovakia as well as Thailand itself. Merry Electronics which supplies headphones to firms like Bose intends to move some of its production to Thailand from southern China.

FDI growth in Southeast Asian countries

(Year-on-year change, in percent)

Source: UNCTAD, Mizuho Research Institute

Tricky times ahead for corporate investment

With the US threatening a further US$200bn in tariffs, and retaliation by China certain, the operating environment for multinational companies present in both countries could yet become a lot more onerous. Such an escalation in trade tensions, analysts agree, can only lead to multinationals acting even more aggressively to de-risk from them, in the process accelerating the ongoing trend to relocate, with Southeast Asia very well positioned to benefit from further robust FDI flows.

According to research published in October, Chinese investment alone in ASEAN countries such as Cambodia, Indonesia, Malaysia, Philippines, Singapore and Vietnam, is set to more than triple to US$500bn by 2035, with the US-China trade war likely to provide a catalyst for the spike. The study was issued by AMRO+3, a regional think tank that represents the ten members of the ASEAN alliance, plus China, Japan and South Korea.

While some regions will inevitably enjoy a boom in investment if trade and traffic wars intensify and protectionism continues to gain traction, for UNCTAD’s Zhan it is the bigger picture that really matters. The agency’s latest FDI data suggests a “gloomy” outlook for FDI overall, he says, adding that FDI is important because it gives countries access to external capital, technology, markets and tax contributions.

Investing corporate cash at the best of times can be complex and demanding, involving as it does the striking of a balance between security, liquidity and yield while keeping abreast of the varying regulations across the target countries. The actions being taken by companies in China and US indicates just how much boardrooms around the world are preoccupied with making sure that they achieve that balance as they look to avoid getting caught up in trade and tariff wars and rising protectionism generally.

Considered alongside the latest FDI data from UNCTAD, and signs we are entering a waning phase of globalisation, it all suggests that for treasurers engaged in FDI, the managing of investment funds has become rather more interesting and challenging.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.