Corporate investment decisions have always been influenced by three overriding objectives – security, liquidity and yield. But in recent years, the first two of these objectives have become paramount and yield has taken a backseat. Since 2008, companies have become increasingly conservative and risk-averse. Above all, they want to be able to convert their investments back into cash quickly to meet any unexpected demands or needs. And remarkably, this precedence has persisted even in an environment with burgeoning sums of cash on corporate balance sheets.

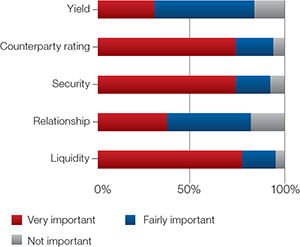

The trend is clearly represented in Treasury Today’s European Corporate Treasury Benchmarking Study published in 2012. In Europe, the vast majority of respondents (79%) described liquidity as a “very important factor” when making investment decisions, and for security the figure was 76%. Meanwhile only 28% of the corporate professionals surveyed considered yield to be a very important factor.

Beyond yield

Alex Riseman, Head of Liquidity Solutions, EMEA at J.P. Morgan Treasury Services, thinks the results of the 2012 Treasury Today Corporate Treasury Benchmarking Studies are a reasonably accurate reflection of what he has witnessed over the past five years with respect to the bank’s clients. According to him, they are keeping more in their liquidity buffer and looking to short-term investments in order to optimise liquidity. And although investment guidelines will always dictate security and liquidity as the priorities, that doesn’t necessarily mean that yield is entirely irrelevant.

“There is always a need to balance security or safety of principle with liquidity and yield. But I think that if you look at what has happened since 2008, there has been a definite sea-change where security has become even more important than it was previously,” Riseman says.

“That is really the number one priority for our clients – they are always going to be concerned about capital preservation above all else. Basel III is also having a significant influence, while making banks stronger than ever and creating a more consistent funding structure, it can also uncover new earning opportunities for clients’ operating cash.”

Chart 1: How important are the following factors when deciding investment policy?

Source: Treasury Today European Corporate Treasury Benchmarking Study 2012

Once bitten, twice shy

Although security and liquidity have always been priorities for corporates when it comes to investments, yield was not always considered to be quite such a subordinate factor for businesses when making investment decisions.

The situation in the immediate aftermath of the global financial crisis gives an inkling as to why this is. Today, the caution many corporates are showing with regard to investments is widely believed to be a symptom of the trauma that lingers from that period.

Before the world of banking descended into chaos in September 2008, many corporates enjoyed trouble-free access to revolving credit facilities from their banking partners. Banks would extend lines of credit to their corporate clients, who could, in return for a commitment fee, draw down on the facility when needed and repay the money when they reached a net-surplus cash position. But when the US sub-prime mortgage sector crisis began to spread across the globe, banks began to batten down the hatches.

“Corporates found that they couldn’t use those facilities in the immediate aftermath of the crisis,” says David Whelan, Director of Treasury Services at Capita. “Banks said if we are not able to fund your draw down, then you cannot use the facility – regardless of the agreement that was in place or the fact that they had been using them to date.”

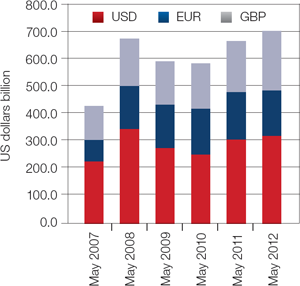

Corporates were quite understandably disturbed by what had followed in the aftermath of the crisis. They began to look at ways to diversify their funding base and reduce their dependence on traditional bank finance. As bank lending declined, asset finance, and particularly corporate bond issuance, skyrocketed. In 2009, $1.5 trillion of debt was issued by companies in the capital markets – a record which would eventually be surpassed three years later in 2012.

Cash stockpiles begin to grow

One consequence stemming from this determination to reduce their dependence on the banks was that companies began to build up large sums of cash on their balance sheets. Since the crisis, treasurers have been consistently increasing their cash balances in every economic quarter, as indicated in the 2012 Liquidity Survey by the Association of Financial Professionals (AFP).

In September 2007, exactly one year before the collapse of Lehman Brothers, UK non-financial corporate cash deposits stood at £622 billion. Just five years later, in September 2012, the corresponding figure had increased by £50 billion to £672 billion.

“Corporates now have less trust in the banks to be available when the going gets tough.”

David Whelan, Director of Treasury Services, Capita

Although this trend has caused a large degree of consternation – among shareholders, politicians and the press – others, like Whelan, see it as a natural, understandable reaction by companies to what they experienced after 2008. “Corporates now have less trust in the banks to be available when the going gets tough,” he says. “A CEO of a big business such as British Airways, for example, would say that they know these facilities are available once again, but they want to make sure that the credit lines are there when they want to draw down on them. If the CEO has a programme for capital expenditure which needs to be executed they don’t want to be told they can’t access the facility because the bank, or the country where the bank is based, is suffering.”

This may also explain why there is such a pronounced level of aversion from companies to seek ways of securing better returns.

But there are ways that banks can help clients to get better returns on the cash sitting on their balance sheets without compromising security and liquidity. One of the ways J.P. Morgan is doing this is through a product it has developed called the Liquidity Management account. With this product the bank looks at the value of the cash over its duration, returning some of the yield that it sees from the long-term value of operational cash back to the client. “It gives the clients benefits in a number of areas,” says Riseman. “From a security point of view the deposit is on J.P. Morgan’s balance sheet, which clearly helps them, but it also gives them the yield that comes as the balances stay with us over time as well as the liquidity that comes with leaving balances in an operating account.”

The bank is also developing other products that Riseman says will secure better returns for clients on their cash balances. It is not just yield that clients are concerned about, he says. Many of the bank’s customers are also looking for ways to manage down their fees and increase their operating margins. “We are looking at developing solutions in which clients can use their operating balances to offset their fees – either locally or on a global basis,” Riseman adds. “When you are looking at returns, yield is not the only factor, so we are also looking at enhancing the ability of our clients to improve their operating margins as well.”

“I think that is exactly the way we approach clients nowadays and how clients see the banks,” adds J.P. Morgan’s Wilco Dado, Head of Cash Management, EMEA, Treasury Services. “We basically say, bring the business with you and because it is linked nightly with operational balances, this type of product can give the client – maybe not better yield – but better overall return on the liquidity through a better pricing on the payment fees.”

In order to preserve their capital corporates in Europe, the UK and the US have also been increasingly turning to money market funds (MMFs), as a means of avoiding losses through inflation, but importantly, without compromising safety or liquidity.

MMFs have always been centred upon stability of principle as their main objective, says Ed Baldry, CEO, EMEA, at ICD-Portal, a software-as-a-service (SaaS) platform investors can use to analyse money markets. “I’ve been in the MMF business for over 20 years, and it has always been security as king, liquidity as queen and yield as the aspiring prince,” he says.

The popularity of MMFs has not been significantly diminished by the lack of yield. Baldry explains that currently in the AAA prime money fund space there is a range between 2bps and 18bps. In euro, the yields are even more marginal, ranging between zero and 4bps. But despite the emphasis of corporate investment strategies moving away from yield, MMFs remain a useful tool for corporate investors. “Effectively since 2008, when we had the Lehman Brothers meltdown and the beginning of the crisis, we could have completely removed the yield column altogether from our website and 80% of our clients wouldn’t have noticed,” he says.

“The focus has very much gone away from the yield on the funds. I would say that in terms of the stability of the funds, the astute corporate treasurers are – from a best practices standpoint – looking further into what they own. For virtually all of the large corporates, financial institutions – and anyone else using money funds via our platform – their focus is on the security of principle first and foremost.”

The looming regulatory challenge

There seems to be little possibility of the corporate investor’s current focus on security and liquidity changing at any time in the foreseeable future. Whelan says that Capita’s forecast for the next few years reveals that the UK and Europe will remain on the verge of recession until at least 2015 – if not descending fully into outright recession.

“The focus has very much gone away from the yield on the funds.”

Ed Baldry, CEO, EMEA, ICD-Portal

Furthermore, with the challenge of new regulatory standards for banks and other financial institutions looming on the horizon, the corporate investor’s job of finding the right balance between security, liquidity and yield, is not likely to become any easier. Most of the new regulatory changes in the financial sector – Basel III, Solvency II and the EU Green Paper on Shadow Banking – are concerned with ensuring that banks and other financial institutions put aside additional capital as a buffer to cover losses in the event of another crisis on the scale of September 2008.

These impending changes will inevitably impact the way in which corporate deposits and investments are handled, says Whelan.

“Banks and other financial institutions will change in order to reflect what the regulators are saying they now need to do in terms of shoring up and putting aside additional capital,” he says. “I believe that this will lead to these institutions seeking longer-term and stickier deposits. And I’m sure the corporate market is quite ready to make that leap. They still want to keep cash relatively short, liquid and visible.”

“I think it will be really interesting to see what happens next,” he adds. “How the structure of the market is going to change as a consequence of these new regulatory pressures and demands, and how the corporate customer base of these banks and financial institutions will react to that.”

Please enter the email that you signed up with below. If your email is

connected to a member account, we will send you a reset link.

This website uses cookies and asks for your personal data to enhance your browsing experience. We are committed to protecting your privacy and ensuring your data is handled in compliance with the General Data Protection Regulation (GDPR).