As cash pools grow in China, treasurers are looking for secure, highly liquid investment solutions in line with corporate policy. The CIFM RMB Money Market Fund1, pioneered by JPMAM, goes one step further.

In China, a country still relatively restricted in terms of cross-border money flows, multinational corporations (MNCs) seeking a short-term, more secure home for their excess cash have few options open to them. The traditional response has been to play safe and opt for bank deposits; however, their yields and tenors are regulated by the country’s central bank, People’s Bank of China (PBoC), making them less flexible than international bank deposits.

For a treasurer seeking more security, liquidity and optimal returns on their cash, there is a means of gaining packaged access into the underlying fixed income markets in China, which generally are much higher-yielding than regulated deposits. And there is one solution that has considerably more provenance than any other in China.

The China International Fund Management (CIFM) RMB Money Market Fund (CIFM RMB MMF), pioneered by J.P. Morgan Asset Management (JPMAM) through its joint venture company, CIFM, was the first – and is the largest2 – AAA-rated fund in China3 and has become one of the most popular investment choices for treasurers in China.

In the beginning…

The history of MMFs in China stretches back to 2003 when the China Securities Regulatory Commission (CSRC) first published MMF guidelines. In 2004, CIFM was created as a joint venture between JPMAM, itself the largest institutional AAA-rated MMF provider globally (with more than $506 billion under management as of 31st December 20124) and the non-bank financial institution, Shanghai International Trust Co (SITCo). The CIFM RMB MMF was launched in May 2005, leveraging on the product and investment expertise of JPMAM. JPMAM continues to be in direct communication with CIFM in regards to the investment process for this fund.

The CSRC guidelines are much broader than what we see in the existing international setting, comments Travis Spence, Head of Global Liquidity, Asia Pacific for JPMAM. The weighted average maturity guideline, for example, is 180 days in China, which is three times longer than typically allowed in the international context at 60 days. Having the appearance more of a short bond fund than a MMF, Spence says JPMAM saw the strategic opportunity to create a AAA-rated fund which would not only be more consistent with the guidelines understood and accepted by its global clients operating in China, but also better serve the needs of rapidly expanding local corporates who share the same investment objectives for their excess operating and reserve cash.

Travis Spence, Head of Global Liquidity

The rating is an additional level of comfort for treasurers, which is also often a requirement of investment policies. “We worked with the rating agencies to develop a rating structure for AAA MMFs in China,” Spence explains. The CIFM RMB MMF’s rating is provided by both Fitch and Moody’s local unit, which is a joint venture with CCXI, the first nationwide domestic credit rating agency created with the approval of the PBoC.

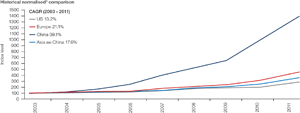

Cash balances are growing faster in China than other developed markets and this has fuelled a quest for better alternatives.

The publication of CSRC’s guidelines was a timely intervention and, as a pioneer in this space, the CIFM RMB MMF was proactively designed to fit neatly into most global investment policies while satisfying the burgeoning needs for better diversification, liquidity and yield optimisation. The CIFM RMB MMF’s T+1 liquidity gives it more flexibility than regulated call deposits, while typically out-performing the rates prescribed by PBoC.

As the concept becomes more familiar, increasing numbers of both local and MNCs are choosing to invest in MMFs in China. The CIFM RMB MMF in China, Spence adds, has doubled in size in the past five quarters, with RMB 21.99 billion ($3.5 billion) in assets under management as of 31st December 20126, and rose another 10% during January 2013 – there are more than 250 institutional investors using the fund, giving it a highly stable client base7.

Chart 1: Cash in Asia is growing even faster than other regions5

*Rebased to index level of 100.

Source: Bloomberg

The launch of the RMB fund was part of a long-term strategy in Asia to serve JPMAM’s global clients and develop new local currency solutions for domestic institutional investors, notes Spence. Since then JPMAM has developed its footprint in Asia with the addition of AAA-rated MMFs in Japanese yen (JPY) in 2007, Singapore dollar (SGD) in 2007 and Australian dollar (AUD) in 2010.

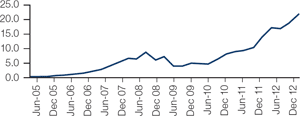

Chart 2: CIFM RMB MMF size since inception (RMB billion)8

Source: Wind data as at 31st December 2012

Taking it to the region

In taking this trail-blazing approach, JPMAM becomes the only provider with a consistent MMF strategy across the region, added to which it brings the benefits of its wider global investment experience. Despite its ongoing series of ‘firsts’ in this space, Spence feels JPMAM is still at an early stage of development of its regional solutions. This is not false modesty, he explains, but “part of our long-term strategy to build a complete platform of short-term solutions across key markets in Asia, and grow with the markets.” It has, he opines, “certainly been a very successful beginning. However, it is important that we continue to innovate in the largest markets like China and Japan, which is why we launched our second MMF in Japan in October 2012, the JPY Government Liquidity Fund, which became the first ever T+0 institutional MMF in the domestic market limited to government risk in the underlying portfolio.”

Indeed, in January 2013, total assets under management (AUM) for JPMAM’s Asian local currency MMFs exceeded $11 billion9, along the way securing its status as the largest institutional MMF provider in Japan10 (and only AAA MMF), the largest AAA MMF in China and the largest and only AAA-rated MMF in Singapore dollars11.

The CIFM RMB MMF was the fastest-growing MMF of the Asian platform for JPMAM during 2012, rising by about RMB 8 billion ($1.2 billion)12. “What we are experiencing is corporate demand driving growth of short-term fixed income markets in Asia, represented by the MMFs we manage,” comments Spence. “This will continue to allow us to create new and innovative solutions for our clients.”

What the treasurer wants

Treasurers generically look for five key attributes when evaluating new investment products, explains Spence:

Security of principal.

Liquidity, without hidden costs or penalties.

Diversification.

Transparency, with easy to understand structures.

Relative yield.

“The CIFM RMB MMF in China is successful because it hits all of these attributes and it is consistent with global treasury policies,” he states, adding that even the push for yield, which is typically the last in the list of demands, is satisfied. “The unique thing about China is that the regulations are still demanding: bank deposits, for example, are controlled by both tenor and yield. However, there is a deep and growing fixed income market that operates based on market yields.”

But the fixed income markets are not the easiest for a treasurer to gain direct access to, comments Spence. MMFs – especially the AAA-rated fund, which invests in the highest rated instruments available onshore (primarily treasury bills and other government-backed instruments, and repos) – provide a neatly packaged solution for those seeking to access the fixed income markets to achieve both diversification and higher yields than traditional bank deposits. For example, during January 2013, the seven-day repo market (the deepest most liquid market in China) provided yields averaging 3%, whereas a regulated seven-day PBoC deposit offered 1.35%13.

Besides improved yield, there is an additional advantage for treasurers. Dividends from mutual funds in general, which would include MMF’s are tax-exempt. With corporate tax in China up to 25%, this is potentially a material difference to other taxable investment options, including deposits and direct securities16.

In this context, if the prospect of MMFs in China sounds too good to be true, Spence refers back to the generally broader guidelines issued by CSRC. Of the 62 MMFs17 in the market today, most follow the broader set of guidelines. Investment practices, he notes, will therefore naturally differ from one fund to another and he urges investors to fully understand the investment processes and risks of the funds they are considering, as well as the experience of the manager, adding that due diligence has always been an important part of investment decisions.

The guidelines of the CIFM RMB MMF creates a unique appeal to prudent corporate and institutional investors in China. Indeed, with the demand in China increasing for alternative investment solutions beyond using simple bank deposits, the CIFM RMB MMF is seen by Spence as “a great first step” for companies to take.

Common Market Yields in China PBoC Deposit Rates14

JPMAM’s experience suggests that trapped cash will still exist, despite new programmes from the Chinese government designed to liberalise cross-border capital flows. For example, pilot schemes around RMB and foreign currency movements are underway, under the guidance of China’s State Administration of Foreign Exchange (SAFE), in consultation with PBoC. For now, these pilots are deliberately limited in their reach (around five banks and thirteen corporates to date).

While the pilots will offer some companies more flexibility in managing excess cash balances in China, Spence notes that there are also companies that are intentionally holding back annual dividends for future growth. “For many companies, there is much more potential to grow inside China than outside,” he notes, adding that local cash in the meantime could earn an average of 3-4% in China as opposed to “near-zero” in developed markets, with the opportunity also for currency appreciation.

As these reserve cash pools grow, treasurers are increasingly looking to segment cash in China, as many already do globally. More intensive cash flow forecasting processes will deliver more balanced decisions between the need for liquidity versus longer investment horizons. Currently the options available further out on the curve are “very limited – almost non-existent”, says Spence. So, as companies in China consider what to do with their cash reserves, he says discretionary investment portfolios, or separate accounts, are becoming “very interesting”.

CIFM, using the same investment process as the RMB MMF and in conjunction with JPMAM, launched the first short-term fixed income separate account in June 201218. Such solutions will play an increasingly important part of its solutions mix going forward. Companies will normally maintain diversification limits in individual mutual funds, thus restricting how much can be placed in a single MMF. The “almost unlimited” scale and diversification that can be achieved in a separate account will thus provide the ideal vehicle for the corporate treasurer with cash reserves that have a longer investment horizon.

Despite the obvious success of the CIFM RMB MMF, surprisingly it is only in the last 18 months that a small band of competitors has seen fit to enter the market. Whilst there are some natural barriers to entry, the most obvious being foreign fund managers’ requirement to operate through a joint venture (one of the reasons why JPMAM partnered with SITCo to create CIFM), Spence admits that he anticipated competitors would appear “much earlier on”.

Regardless of the how and when other players make their entrance, Spence welcomes these incursions into what has become JPMAM’s own high ground. “It will help to grow the overall market and provide some alternatives,” he comments. But then he can perhaps afford the easy acceptance of competition: with an eight-year track record in the market, it gives JPMAM a distinct advantage in terms of market knowledge and scale within its funds. “I think that is going to continue to differentiate JPMAM and CIFM for years to come.”

MMFs – A brief guide

Money market funds (MMFs) are short-term debt securities, forming a part of the fixed income market. There is no central exchange or trading floor and trades are executed via the dealer market only, which is to say transactions are made through the dealer’s own account; money markets rarely offer direct access for investors and so mutual funds tend to be the way in. Instruments traded are numerous but the main ones typically used in the international setting are treasury bills, certificates of deposit (CDs), commercial paper (CP), Eurodollar deposits, asset-backed securities and repurchase agreements (repos). MMFs tend to be rather conservative in their approach and therefore relatively low-yielding, but they are highly liquid, making them attractive to treasurers seeking a home for their excess cash.

The CIFM RMB Money Market Fund (the “Fund”) is a fund managed by China International Fund Management Co. Ltd. which is a joint venture between Shanghai International Trust Ltd and J.P. Morgan Asset Management (UK) Ltd. This Fund is not being offered through J.P. Morgan Funds (Asia) Limited. The information contained herein is for informational purposes. Shares of the Fund may be offered and sold only in China to: (i) individuals who are Chinese citizens and residents; (ii) institutions legally organised in China and permitted by Chinese law and regulation to invest in open-end investment funds; and (iii) entities with “Qualified Foreign Institutional Investor” status in China.

Source: Wind data, as at 31st December 2012.

Source: China Cheng Xin International Rating Co. Ltd. (CCXI), with technical assistance provided by Moody’s Investors Service, Inc. Moody’s), assigned a MMF national scale rating of Aaa to the CIFM RMB MMF. This level of credit quality qualifies for the highest fund rating on a national scale basis.

Source: iMoneyNet, selected AUM for the Asset Management (JPMAM PCS, PB) division of J.P. Morgan Chase & Co. and CIFM internal report, all data as at 31st December 2012.

Source: Bloomberg, as of 15th December 2013. Analysis done by looking at the cash and cash equivalents of the top 100 listed companies in each country/ region for each respective fiscal year Asia includes China, Japan, Singapore, Hong Kong, Taiwan, Korea, India and Australia

Source: Wind data as at 31st December 2012 and 30st September 2013.

Source: CIFM internal reporting 31st January 2013.

Source: Wind data as at 31st December 2012.

Source: JPMAM internal reporting including selected AUM for the Asset Management (JPMAM PCS, PB) division of J.P. Morgan Chase & Co. and CIFM internal report, data as at 31st December 2012.

Source: JPMorgan and The Investment Trusts Association, Japan (JITA), as of 31st January 2013)

Source: Bloomberg as at 31st January 2013.

Source: Wind data, as at 31st December 2012 and 31st September 2011.

Source: Bloomberg and PBoC website as at 31st January 2013.

Source: Bloomberg and PBoC website as at 31st January 2013.

Source: Bloomberg and PBoC website as at 31st January 2013.

Investors are advised to take, in advance, all necessary legal, regulatory and tax advice on the consequences of an investment.

Source: Wind data as of 31st December 2012.

Source: JPMAM internal reporting and CIFM internal report, data as at 31st January 2013.

Disclaimer

FOR WHOLESALE/PROFESSIONAL/INSTITUTIONAL CLIENTS ONLY NOT FOR RETAIL CLIENTS’ USE OR DISTRIBUTION.

For non-US Investors. Please note that this document is for professional, institutional or wholesale investors’ use only. It is not for public distribution and the information contained herein must not be distributed to, or used by the public.

The material and communication contained herein is intended as a general market commentary for distribution to investment professionals only. The above information does not constitute investment advice, or an offer to sell, or a solicitation of an offer to buy any security, investment product or service nor a distribution of information for any such purpose. Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The information provided herein should not be assumed to be accurate or complete. The views and strategies described may not be suitable for all investors. These materials are not intended to constitute legal, tax, or accounting advice.

The value of investments and the income from them may fall as well as rise and you may not get back the full amount invested.

J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. This communication is issued by the following entities: in the United Kingdom by JPMorgan Asset Management (UK) Limited which is regulated by the Financial Services Authority; in other EU jurisdictions by JPMorgan Asset Management (Europe) S.à r.l., Issued in Switzerland by J.P. Morgan (Suisse) SA, which is regulated by the Swiss Financial Market Supervisory Authority FINMA; in Hong Kong by JF Asset Management Limited, or JPMorgan Funds (Asia) Limited, or JPMorgan Asset Management Real Assets (Asia) Limited, all of which are regulated by the Securities and Futures Commission; in India by JPMorgan Asset Management India Private Limited which is regulated by the Securities & Exchange Board of India; in Singapore by JPMorgan Asset Management (Singapore) Limited which is regulated by the Monetary Authority of Singapore; in Japan by JPMorgan Securities Japan Limited which is regulated by the Financial Services Agency; and in Australia by JPMorgan Asset Management (Australia) Limited which is regulated by the Australian Securities and Investments Commission; in Brazil by Banco J.P. Morgan S.A. (Brazil) which is regulated by The Brazilian Securities and Exchange Commission (CVM) and Brazilian Central Bank (Bacen); and JPMorgan Asset Management (Canada) Inc. is a registered Portfolio Manager and Exempt Market Dealer in Canada (including Ontario). In addition, it is registered as an Investment Fund Manager in British Columbia. In the United States by J.P. Morgan Investment Management Inc. which is regulated by the Securities and Exchange Commission. For U.S. registered mutual funds, J.P. Morgan Institutional Investments Inc., member FINRA/SIPC. Accordingly this document should not be circulated or presented to persons other than to professional, institutional or wholesale investors as defined in the relevant local regulations. The value of investments and the income from them may fall as well as rise and investors may not get back the full amount invested.

Please enter the email that you signed up with below. If your email is

connected to a member account, we will send you a reset link.

This website uses cookies and asks for your personal data to enhance your browsing experience. We are committed to protecting your privacy and ensuring your data is handled in compliance with the General Data Protection Regulation (GDPR).