Over the past two years, tough economic conditions have forced treasurers to adopt a ‘back to basics’ approach to treasury management, tapping all possible internal sources of funding. Now is the time for treasurers to take the next step and start positioning their organisations for growth. Can further internal efficiencies help achieve this goal? In this Business Briefing we look at the relevance of DSO (days sales outstanding) and achieving efficiency in the order-to-cash cycle to source funding in a post-crisis environment.

A different approach

With credit likely to remain scarce – and expensive – identifying alternate sources of internal funding remains a priority for organisations worldwide.

So what options are available? The sale of assets or the cutting of dividends are certainly examples of alternate sources, but working capital management (WCM) has probably become recognised as one of the most lucrative and sustainable methods of internal funding. WCM has also seen the treasurer’s role expand to an integral partner of the commercial business. But where should the treasurer be looking to unlock the next layer of trapped liquidity?

DPO is yesterday’s news

Before the financial crisis hit, organisations focused on the internal processes that were immediately controllable. First in line was DPO (days payable outstanding). Streamlining and optimising payables became the treasurer’s mantra, together with a focus on straight through processing (STP).

While DPO and STP remain integral to achieving internal efficiencies, these efforts alone do not provide a complete WCM solution. With STP rates often nearing 98%, treasurers need to understand that the internal efficiency gains from DPO are all but exhausted and that there are new sources to be explored.

The time has therefore come to shift the thinking from P2P (procure-to-pay) to O2C (order-to-cash), from DPO to DSO (days sales outstanding) and from STP to STR (straight through reconciliation).

STP to STR

Straight through processing is a commonly used measure of success across the global treasury community. However, STP usually focuses on corporate-to-bank flows or the sending of payments (or direct debits) in an automated fashion with limited – or no – focus on the bank-to-corporate flows. To achieve end-to-end efficiency requires a move beyond STP to STR, where all flows to the corporate including payment rejects/returns, reconciliation of balances and incoming transactions or collections are automated. STR steps in to fill the current gaps on bank-to-corporate flows automating both financial and operational reconciliation, providing a more complete measure of success.

DSO and its impact on working capital

Unlike DPO, DSO – the average number of days taken by a company to collect payment from a completed sale – is still a largely untapped source of internal funding. Poor receivables management is reflected in high DSO and affects a company’s ability to access internal funding sources. In other words, the longer it takes for a payment to be collected, processed, matched and applied, the longer it is until that cash can be used for other purposes or until the credit lines can be freed up and the next sale or shipment made to the customer. Addressing DSO is therefore an achievable way of taking the efficiency agenda to the next level.

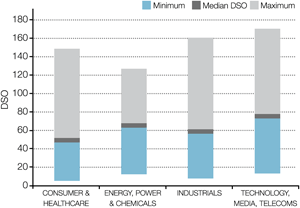

Figure 1: DSO Analysis by Industry Sector

So why wasn’t DSO first in line to be controlled? The processes involved often belong to multiple departments and are therefore harder to monitor and influence. That said, the hard work does pay off, in particular in industries with complex supply chains and global operations.

An analysis of Citi’s top 3,000 global companies around the world shows that these customers have, on average, $1.3 billion in trapped internal working capital which could be unlocked by reducing their DSO to within the median range for their industry.

Across sectors, there is sometimes a discrepancy of over 150 days between the ‘best’ (shortest) and ‘worst’ (longest) DSO. This large discrepancy means that many companies have significant room for improvement.

While these improvements look attractive – and simple – on paper, achieving them requires dedication and determination.

Order-to-cash: the challenge

One of the hardest parts of tackling DSO is that it has to be done cross-functionally. In other words, some of the processes in the order-to-cash cycle are outside of the full control of treasury, either in the hands of other departments, or, crucially, with the customer. DSO is also subject to other external influences – particularly between markets/countries – in terms of the collection instruments commonly available and also the collections culture. In Italy for instance, DSO is typically 30 days longer than in Ireland, mainly because Italian companies view long collection windows as standard.

These factors alone, or in combination, may lead to disconnects or inefficiencies in the cycle, which will ultimately have a detrimental effect on the efficiency of the company’s working capital – possibly even creating a need for external funding.

So where are the main DSO pain points that are causing breakdowns late in the cycle, what are they and how can they be addressed?

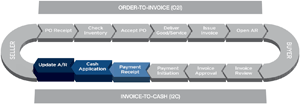

Figure 2: Friction in the order-to-cash (O2C) cycle

Update AR

Cash Application

Payment Receipt

Pain Points

Paper based/non system readable data

Poor data quality

Limited AR matching

Lack of remittance information

One payments for many invoices

Partial payments

Multiple collection types

Multiple outputs

Country differences

Average DSO Saves

–

1-2 days*

3-5 days*

Faster Revenue Recognition

2-3 days*

2-3 days*

–

* For a company with a turnover of €10 billion, one day of average DSO saves or of faster revenue recognition has a positive impact of €27m.

Pain points

Unfortunately for treasury, pain points exist all along the order-to-cash cycle. However, three of the most commonly identified areas of ‘pain’ are:

Multiple collection types.

There is currently no best practice around collection instruments. Not only is there variation from industry to industry, but also from country to country. While SEPA is aiming to make improvements in this space, there is still no common collection method. The channels vary from cash picked up by a ‘man in a van’ in some markets, to cheques, or to the more advanced electronic means such as electronic transfers or direct debits.

Proliferation in instruments leads to multiple output channels, which means increased manual reconciliation tasks and therefore increased margin for error. This leaves DSO vulnerable to significant increases.

Lack of remittance data.

If accounts receivable (AR) matching is carried out manually at an entity level, lack of remittance data is often not such a prominent challenge as there are far fewer payments to marry up. At an SSC level, however, where there may be thousands of payments, many from accounts with similar references or codes, the real importance of remittance data can be seen. With truncated data on the receipts, receivables matching becomes an extremely time consuming task.

This is exacerbated by customers sending, for instance, one payment to settle several invoices, partial payments, or on occasion, overpayments. Without full remittance data for these exceptions, DSO begins to soar as investigation work is required.

Non-system readable data.

Delivery of better information alone does not, in itself, however, enable operational reconciliation if the systems being used by a company are not able to handle the information. If collections and rejected/returned items are not automatically driven through to all the downstream workflows, the manual labour to reconcile and apply a payment to an AR open item is high – as are the hidden costs.

Case study

Centralised payments and collections improves visibility and efficiency

Jérôme Miara

European Treasurer

S&P 500-constituent Newell Rubbermaid is a global marketer of leading consumer and commercial products with sales of around $5.6 billion in 2009.

The challenge

Following a series of mergers and acquisitions, Newell Rubbermaid maintained 190 accounts with 22 different banks resulting in a large number of manual processes, few economies of scale and limited control. The company decided to centralise the accounts payable, accounts receivable and general ledger functions into a Shared Service Centre (SSC) in The Netherlands. In order to benefit from economies of scale, the company also recognised that it needed to rationalise its bank structure.

In the first quarter of 2007, Newell Rubbermaid issued a RFP with the objective of finding a single banking partner for payments and collections across 22 countries in EMEA (excluding the UK). One of the company’s most important criteria for selecting a partner was the bank’s capability to manage local collections, especially domestic instruments, as well as payments in each market. “Accounts receivable were a key consideration because while Newell Rubbermaid can determine how it pays its suppliers, customers inevitably determine local collection methods,” explains Jérôme Miara, European Treasurer.

The solution

Citi’s proposal envisaged that starting in 2007 and finishing in mid-2009, 126 Citibank accounts would be opened for Newell Rubbermaid’s 54 different legal entities across EMEA. Payments would be made using Citi’s state-of-the-art platform for file transmission and translation, Citi® File Xchange, and the web-based banking platform CitiDirect® Online Banking. Domestic solutions would be implemented in each country to support the local entities’ requirements, including the use of instruments such as LCRs, RIBAs and Pagares. A pan-European lockbox for cheques would be established.

The result

Citi was selected to become Newell Rubbermaid’s partner in EMEA (excluding the UK) in the second quarter of 2007. “The bank’s geographic footprint is unique and is made up of fully owned branches – we didn’t want to introduce complexity arising from additional local partners,” says Miara. The Citi bank accounts were opened in phases as planned and in parallel, Newell Rubbermaid closed 148 legacy bank accounts and exited 17 non-strategic bank relationships. The simplification of Newell Rubbermaid’s bank structure in EMEA has delivered a wide range of benefits. “We have gained control and visibility through the use of a single centrally-controlled internet banking platform,” says Miara. Increased visibility of its order-to-cash cycle processes has helped the company to improve decision-making, reduce credit risk and enhance working capital management

Newell Rubbermaid has also gained numerous benefits from increased automation: a single interface has been set-up with the company’s Movex ERP from which payment and collection files can be submitted directly. It uses one inbound file for the upload and automated cash application of its accounts receivable balances using GetPaid software. Consequently, manual processes have been reduced and treasury staff have been redeployed to value-added tasks. At the same time, the rationalised bank structure has helped Newell Rubbermaid to gain efficiencies in the order-to-cash cycle which contributed to an improvement in DSO. The company has used the project as an opportunity to harmonise its banking processes, enabling the migration of accounts payable and receivable and general ledger processes to its European SSC – something that would have been more difficult without account rationalisation. It will also facilitate a forthcoming move to SAP. “Our streamlined structure as a result of this project will make the process easier,” says Miara.

Easing the pain

It is unlikely that receivables management will ever be 100% perfect: not everyone will pay electronically, remittance data won’t necessarily be complete and there will always be exceptions that need to be handled manually,” says Francyn Stuckey, Client Sales Management, Treasury and Trade Solutions, Global Transaction Services, Citi. “However, there are many solutions that banks can offer, ranging from the basic to the sophisticated, that can help companies improve receivables management, drive STR and optimise DSO.”

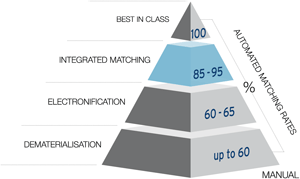

Citi has identified four stages where it can assist its clients in achieving optimum levels of efficiency and automation:

Figure 3: Receivables – cash application

Dematerialisation

Moving away from paper-based collection instruments is the first step to achieving system-readable, comprehensive data. To some companies this may suggest that investment will be needed in their technology infrastructure, but in fact companies may benefit more by using the financial outlay to provide incentives for their customers to use direct debits or other forms of electronic payments.

The use of electronic payments, electronic invoice presentment and payment (EIPP) will also help eliminate paper earlier in the order-to-cash cycle and improve remittance capture. Companies will, however, need to take into account the markets in which they are operating as it is not always achievable – or indeed permissible – to move away from paper instruments. An initial focus on largely ‘electronic’ markets will give quick rewards.

Electronification

The second step is to move away from paper-based reconciliation to electronic delivery and a system-based (ie ERP/TMS) matching process. It is at this stage that banks can add real value by enhancing and standardising the data that they provide to the client. In addition to advanced techniques, data enhancement can be done by using existing services in a smarter way. For example, lockboxes can be used as a way of gathering remittances for all payments, which are then further enriched by the banks to ensure all data is passed on to the client in an ERP/TMS readable format.

Integrated matching

Using receivables solutions that are integrated into the company’s ERP/TMS is vital to achieving STR. However, standard solutions do not address the problems of multiple data sources and incomplete remittance data. Advanced techniques, such as automated account reconciliation reports which deliver enriched information for all collections – both paper and electronic – based on set algorithms and customer data, do help address these problems, thus reducing the effort and the associated costs of manual intervention. Virtual accounts are another technique to help solve the challenge of insufficient remittance data.

Best in class

The final step is to become ‘best in class’. At this point in time, the only manual reconciliation that should be carried out is for exception handling, at which point business process outsourcing can be introduced to manage these AR exceptions. Regardless of whether corporates opt to take this step, they should still be looking to fully leverage their bank’s AR offering in order to achieve the final percentage points of STR and to maximise impact on their DSO.

Conclusion

While addressing receivables management may seem daunting, the size of the reward is commensurate with the effort required, as Karin Flinspach, EMEA Receivables Head, Treasury and Trade Solutions, Citi, explains, “Often treasurers don’t feel empowered to interfere with the sales organisation and the client’s payment behaviour. However with the renewed focus on working capital and its significant contribution to the net margin of the company, the treasurer can seize the opportunity to get buy in from the top of the organisation to force wide reaching changes in the order-to-cash cycle, thus achieving huge efficiencies.”

The significance of these efficiencies should not be underestimated. After all, it is not just a question of unlocking trapped working capital. There is the potential to bring down full time employee costs through improved automation, for instance, IT costs can also be reduced and operational efficiencies ranging from harmonisation of reporting to improved AR accounting can also be achieved. Together, these efficiencies will be instrumental in positioning companies for growth in the post-crisis environment.

Citi’s experience as a trusted partner

For more than 100 years, Citi has been successfully partnering with clients and enabling them to benefit from extensive product capabilities, geographic reach and local market expertise. With a footprint in more than 103 countries, encompassing full local capabilities which are complemented by local network partnerships, Citi is perfectly positioned in the receivables space to address our clients’ needs. Our dedicated in-country professionals can assist in advising on the best-in-class receivables management solutions.

Citi’s suite of receivables services goes beyond the traditional collection channels and instruments. We are working closely with our clients to optimise their order-to-cash cycle and to help them achieve greater efficiencies, translating into increased match rates, cost savings, DSO reductions and improved working capital management. We pride ourselves in being an industry leader through continuous product innovation and sound investment in technology and people.

Contact details:

Karin Flinspach

EMEA Receivables Head Treasury and Trade Solutions, Global Transaction Service

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.