Managing liquidity through periods of rising interest rates

Published: Nov 2013

Investors have grown accustomed to an environment of record low interest rates. However, comments from the world’s major central banks, coupled with improving economic growth expectations, suggest that investors may soon have to adapt to a changing rate environment. For those investing for the short term to meet cash management needs, ensuring preservation of capital and maintaining liquidity as interest rates rise is a key priority. An understanding of how different cash-like investments are affected by rising rates can help treasurers position their portfolios to achieve this.

The current, yield-constrained environment

Since the financial crisis of 2008, the world’s major central banks have, to varying degrees, pursued ultra-loose monetary policies to stimulate economic activity. The US Federal Reserve (the Fed) was the earliest advocate of this approach, taking its benchmark federal funds rate to a record low of 0-0.25% in December of 2008, where it has remained since. The Bank of England followed suit soon thereafter, in March 2009 reducing its key rate to 0.50%, while the European Central Bank has gradually cut Eurozone interest rates from 2.00% in 2009 to their current record low level of 0.50%.

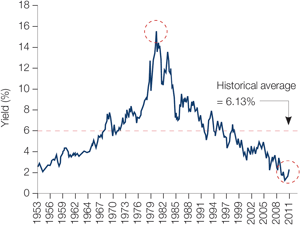

While interest rates have languished at historic lows, the unprecedented asset-purchase programmes of the Fed, the Bank of England and the Bank of Japan have served to inflate the prices of bonds, supressing yields further still. With the debt crisis in the Eurozone periphery raising concerns over a possible break-up of the currency bloc, and with developed markets in a prolonged slump, the yield on the US ten-year Treasury bond hit an all-time low just below 1.4% in July 2012. This was down from a high of nearly 15.9% in September 1981, as shown in the chart below. UK Gilt and German Bund yields have also fallen to their lowest ever levels.

Chart 1: Yield on US ten-year Treasury bond

Source: The Federal Reserve; monthly data as of July 2013

The yield-constrained environment of the last few years has been a challenging one for liquidity investors looking to meet their short-term cash needs, particularly as inflationary pressures have served to erode returns. Conditions, however, now look to be changing and yields are picking up from their lows – since April, the interest rate on the ten-year US Treasury has risen by more than 100 basis points. Although this is likely to be a gradual process and central bank policy rates may remain on hold for some time yet, liquidity investors need to be prepared for an eventual normalisation of interest rates.

Lower for how much longer?

As the outlook for economic growth in the developed world has improved, investors are increasingly focusing on how much longer central banks will keep interest rates at record lows and when they will change the trajectory of their asset-purchase programmes. This focus by investors has already led to a significant rise in benchmark bond yields from their record lows. For the first time in many years, the broader fixed-income asset class has experienced negative returns.

The current era of extraordinarily low interest rates is best explained by the unprecedented actions by the Fed and other central banks in response to the financial crisis. We have already seen above how the Fed initially employed traditional monetary policy tools, lowering the federal funds target rate from 5.25% in September 2007 to a 0%-to-0.25% range in December 2008 (where it has remained since). Then, in November 2008, amid near-frozen credit markets, overnight rates close to zero and the US economy mired in the worst recession since the 1930s, the Fed embarked on a programme of quantitative easing (QE). The central bank extended the size and average maturity of their balance sheet assets through the purchase of Agency debentures, Mortgage Backed Securities (MBS) and Treasuries. These actions sought to contain the financial crisis, limit its impact on the broader economy, and aid the prolonged recovery by lowering longer-term interest rates to encourage investment and consumption.

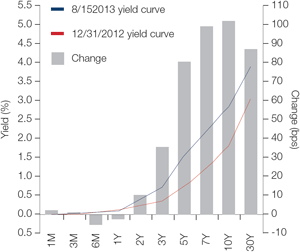

Roll forward to May 2013, and Fed chairman Ben Bernanke was indicating that the Fed could begin reducing its monthly asset purchases later this year if improvements in economic growth seemed sustainable. This indication was followed in June by a statement that asset purchases may end altogether in 2014. As a result, investors aggressively sold both risk assets and Treasuries, causing the yield on the ten-year Treasury to rise to over 2.60% in June, from just 1.63% at the beginning of May. Credit spreads also widened approximately 30 bps over that period (as measured by the Markit CDX North America Investment Grade index). While yields have retraced somewhat since that initial reaction, they remain higher for UST maturities longer than two years as of mid-2013. The rise in yields across the curve, from two years out, is shown in Chart 2.

Chart 2: Yield curve US Treasury’s

Source: Bloomberg; data as of 15th August 2013

Note: X axis is not to scale

As the central bank has signalled, reductions in asset purchases will be the first step toward the normalisation of monetary policy (the Fed has repeatedly emphasised that this decision will be “data dependent”). Ending the QE programme would be its second step. If economic conditions warrant, the Fed’s next moves would include modification of forward guidance regarding, and the eventual raising of, the federal funds target rate.

Fed communications suggest that the current level of the target rate will likely remain appropriate for a considerable period of time. But as investors anticipate diminished monetary accommodation and eventual tightening by the Fed, demand for fixed income securities will fall, causing prices to drop and market interest rates to rise.

In Europe, monetary authorities have begun to issue forward guidance about the future direction of rates to try to stem rising bond yields in reaction to US tapering. Both the European Central Bank and the Bank of England have sought to reassure markets that rates will remain at record lows for a prolonged time so that borrowing rates remain attractive and continue to stimulate economic growth. Nevertheless, with interest rate policy having been effectively made conditional on improvements in the real economy, there remains considerable uncertainty about the actual timing of rate rises.

Allocating cash most effectively ahead of rising rates

Given rates are at record lows and unlikely to fall much further, and with economic activity picking up in North America and in Europe too, it is safe to say that interest rates will begin to trend upwards at some point. We have seen that bond markets are already adjusting to a period of interest rate normalisation. As interest rates and yields rise, short-term cash investors will also have to adjust to ensure that capital is preserved and liquidity is maintained.

This is because all fixed income and short-term portfolios carry an inherent level of interest rate risk, so rising rates will have an impact on the current and future values of existing cash holdings, as well as influence the relative attractiveness of different investments for meeting specific investment needs. Investors with short-term investment horizons should therefore consider the potential effects of rising interest rates on the instruments at their disposal and adjust their exposures accordingly.

Strategies to insulate a portfolio from rising rates

How can an investor protect a portfolio of bonds in a period of rising rates? Though some investors may choose to simply exit the asset class, there are strong arguments for maintaining a core allocation to fixed income. In most rate environments, fixed income provides diversification, a steady stream of income and a lower volatility investment over time. Additionally, fixed income portfolios with greater duration have historically provided higher returns, albeit with greater volatility, over longer time horizons. However, for investors with shorter investment horizons (especially those with potential near term cash needs), or those looking to protect profits from longer duration strategies, a key priority is to mitigate potential volatility during the anticipated rising rate period. To that end, investors should consider how they can best deploy two effective strategies for managing a rising rate environment: shortening duration and increasing income.

Shortening portfolio weighted average duration

The most effective way to protect a portfolio from the impact of rising rates is to reduce its weighted average duration. In traditional fixed income portfolios, this is typically achieved using one or more of the following methods:

Sales of longer dated fixed coupon securities, and/or reinvestment of interest income, into those with shorter tenors.

Investments in higher income or higher yielding securities, which will have shorter interest rate durations relative to bonds with the same maturity. By investing in credits with spreads over the risk free rate, more cash is received on the coupon payment dates thereby shortening the duration and increasing the cash available to be reinvested at higher rates.

Purchases of floating rate notes, whose interest rates reset on a regular basis. As a floater’s interest rate resets to adjust for market changes, its price should typically experience less volatility and thus it will have a lower duration.

With the latter it is worth pointing out that most floating rate notes reset interest rates on a monthly or quarterly basis thus durations on these securities are typically shorter than three months. However, it is important to note that while the owners of such bonds have limited exposure to changes in interest rates, they are exposed to the creditworthiness of the borrower until the final maturity of the bond. This means that floating rate bonds, not issued by the US Treasury, can have longer spread durations than interest rate durations. This can result in greater volatility should credit conditions change.

Increasing the interest income component of total return

Increased income or yield not only lowers duration but also provides greater income return helping offset declines in price in periods of rising rates. However, higher yields due to increased credit exposure do not come without added risk. Should credit spreads widen in conjunction with rising rates, these securities will under perform. Similar to interest rate duration fixed income investors must be cognizant of spread duration as well. Longer spread durations will typically be more negatively impacted by widening credit spreads.

Due to the risk of widening credit spreads it is important that an investor examine where credit spreads are relative to historical patterns at the beginning of a rising rate period. In recent years, extremely low levels on risk-free rates have forced investors to seek yield in riskier securities, resulting in tighter credit spreads. It is possible that as investors sell fixed income securities in anticipation of higher rates, sales will not be limited to risk-free Treasuries alone and credit product may see spreads widen.

Examples of short duration product styles

As they consider the key elements of investing in a rising rate environment–shorter duration, income cushion, lower credit spread duration – investors can choose among a variety of traditional short-term fixed income products. Rising interest rates will affect different cash-like investments in different ways. Understanding how various cash investments are effected by interest rates allows investors to take action to mitigate the impact of a rising interest rate cycle. The following is a summary of the impact that investors can expect to see from rising rates on the main types of short-term investments:

Overnight bank deposits:

Rates tend to track rises in interest rates quite closely, although investors should be aware that, due to being exposed to a single counterparty, credit risk may be higher. Counterparty risk can be reduced through diversification, while potential returns may also be higher from a more diversified investment.

Term deposits:

Tend to lag shorter-dated deposits due to the need to wait out the term of the deposit before re-setting to a higher interest rate. These carry the same counterparty risk as overnight deposits, but as they are not marked-to-market, investors are not exposed to unrealised losses.

Money market funds:

Will see their yields rise in line with prevailing interest rates, although with a small time lag. Due to their diversified portfolios, they carry a significantly lower level of counterparty risk than overnight or term deposits. Also these are not marked-to-market, so there are no unrealised losses.

Managed reserves funds:

Usually have durations between 0.25 and one year, and invest primarily in higher income-generating short-term corporate securities. Due to higher durations, unrealised losses can occur when rates rise. Managed reserves funds have historically outperformed money market funds over longer time periods, as well as offering a higher yield.

Short-term bond funds:

Potential to earn higher yields than cash instruments, but longer duration and marked-to-market pricing means that they are more sensitive to interest rate movements. Investors may therefore experience unrealised losses, and therefore need to be certain about the accuracy of their cash flow forecasting before investing in longer duration in a rising rate environment.

Separate accounts:

Offer investors the flexibility to tailor portfolios so that they have the specific duration and other risk characteristics that they are comfortable with. However, separate accounts are marked-to-market, and may suffer unrealised losses as interest rates rise.

Conclusion

With the right investment strategy in place, cash investors can ensure that they are best positioned to benefit when interest rates eventually begin to rise. Given that timing the market is fraught with difficulties, treasurers may benefit from a flexible approach that allows them to move cash reserves between different options to suit the prevailing interest rate environment. The first step to designing a robust cash strategy is to recognise that different short-term investments carry different yield, security and liquidity considerations through the interest rate cycle.

For a copy of the whitepaper ‘Managing Liquidity through periods of Rising Interest Rates’ please contact your client adviser or Travis Spence, Head of Global

Liquidity, Asia Pacific +852 2800 2808 or travis.w.spence@jpmorgan.com

J.P. Morgan Asset Management

J.P. Morgan Global Liquidity is part of J.P. Morgan Asset Management and offers a range of comprehensive global short-term and medium-term fixed income investment solutions. A combination of these products can assist our institutional clients to achieve the liquidity, security, risk and return profile that you desire. By entrusting your liquidity investments with J.P. Morgan Global Liquidity you can be sure that you are investing with a market leader.

As the largest AAA-rated money market fund provider in the world and more than $478 billion in assets under management1, we provide institutional clients with best-in-class investment solutions. This scale gives us strong purchasing power and creates exceptional levels of liquidity and diversification within our liquidity funds which are denominated in USD, GBP, EUR, BRL, AUD, SGD, JPY, CNH and RMB2. J.P. Morgan Global Liquidity also offers additional diversification through government only liquidity funds in a range of currencies including USD, GBP and JPY3.

For investors with a slightly longer-term investment horizon, we also offer short-term fixed income solutions such as our current reserves and managed reserves funds as well as separately managed accounts which may be suitable for investors globally looking for potentially higher returns than a liquidity fund, but who are prepared to incur a higher level of risk in order to achieve this.

J.P. Morgan is also one of the leading liquidity advisors in China for RMB investment solutions. After China International Fund Management Co., Ltd (CIFM), our joint venture company in China4, partnered with J.P. Morgan Asset Management to pioneer the first onshore AAA-rated5 RMB money market fund in 2005, J.P. Morgan Chase Bank (China) Company Limited received approval in September 2013 from the China Securities Regulatory Commission (CSRC) to distribute domestic mutual funds to investors in China. The license unites nearly a decade of investment experience from the partnership between J.P. Morgan Asset Management and CIFM with the global resources of the world’s largest liquidity manager to allow J.P. Morgan Global Liquidity China6 to provide investment advisory and structuring services, market insights and best execution of RMB investments directly to corporate and institutional clients in China.

Source: Based on AUM for the Asset Management (JPMAM, PCS, PB) division of J.P.Morgan Chase & Co. as at 30th June 2013.

JPY for qualified Japan domiciled investors only and RMB for qualified China domiciled investors only. The RMB fund is managed by China International Fund Management Co. Ltd (CIFM), a joint venture company between Shanghai International Trust Co., Ltd. and J.P. Morgan Asset Management (UK) Ltd. in China. The shareholders do not engage directly in the investment management of funds managed by CIFM. The information contained herein is for informational purposes.

JPY for qualified Japan domiciled investors only and RMB for qualified China domiciled investors only.

The RMB fund is managed by China International Fund Management Co. Ltd (CIFM), a joint venture company between Shanghai International Trust Co., Ltd. and JPMorgan Asset Management (UK) Ltd. in China.

Source: China Cheng Xin International Rating Co. Ltd. (CCXI), with technical assistance provided by Moody’s Investors Service, Inc. (Moody’s), assigned a money market fund national scale rating of AAA to the CIFM RMB Money Market Fund in May 2005. This level of credit quality qualifies for the highest rating on a national scale basis.

J.P. Morgan Global Liquidity China is the brand for the fund distribution business of J.P. Morgan Chase Bank (China) Company Limited in China. J.P. Morgan Chase Bank (China) Company Limited is a local incorporated bank in China with a fund distribution business qualification (基金销售业务资格). J.P. Morgan Chase Bank (China) Company Limited is a subsidiary of J.P. Morgan Chase & Co. and regulated by the China Banking Regulatory Commission (CBRC), and for fund distribution, it is also regulated by the China Securities Regulatory Commission (CSRC).

Disclaimer

FOR INSTITUTIONAL AND PROFESSIONAL CLIENTS ONLY | NOT FOR RETAIL USE OR DISTRIBUTION

This document has been produced for information purposes only and as such the views contained herein are not to be taken as an advice or recommendation to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all-inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. Both past performance and yield may not be a reliable guide to future performance and you should be aware that the value of securities and any income arising from them may fluctuate in accordance with market conditions. There is no guarantee that any forecast made will come to pass. Information herein is believed to be reliable but J.P. Morgan Asset Management does not warrant its completeness or accuracy. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.