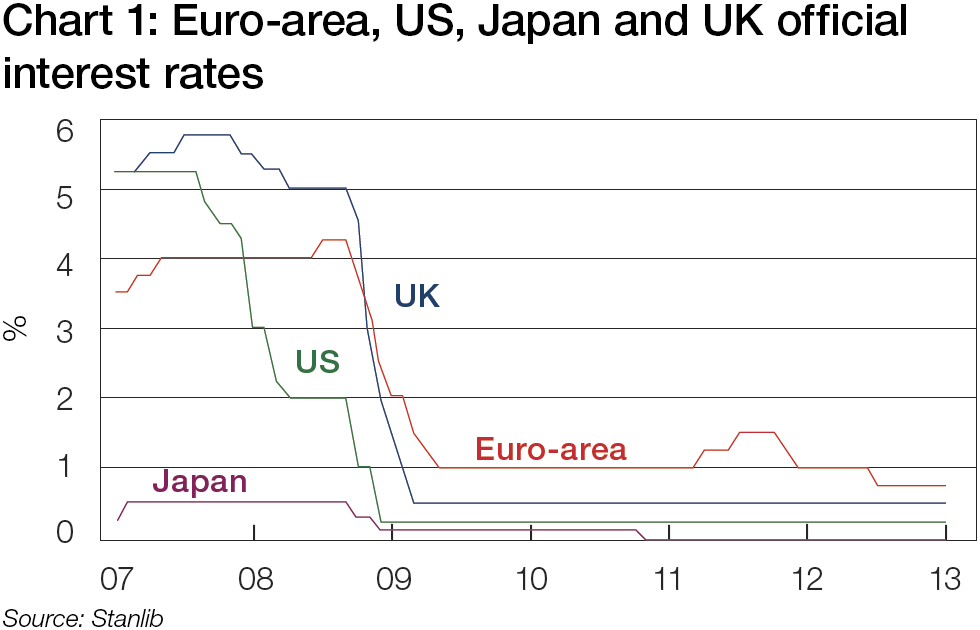

It seems that low interest rates are here to stay. In the wake of the global financial crisis, the central banks in a number of western economies – most notably in the US and Europe – cut short-term rates in tandem with a range of other unconventional monetary policies designed to restore liquidity to glacial credit markets by driving yields down at both the long and short ends of the curve.

Rates are at rock bottom across the board. In the US, the Federal Funds Rate has remained at 0.25% since the onset of the crisis, as has the benchmark interest rate in the euro, while the Bank of Japan, under the ‘Abenomics’ doctrine, have gone one step further by bringing their benchmark rate down to 0%. Even as the recessionary gloom finally begins to lift in some countries, central bankers seem in no rush to change course. Indeed, a number of economists believe that the ‘new normal’ on interest rates in the US, UK and Eurozone will not be nearly as high as it was in the decades prior to the crisis.

A low rate environment is very much a double-edged sword for the corporate treasurer. On the one hand, it is a great opportunity to refinance and lock in lower priced debt; we have seen no shortage of corporates taking advantage of that in the past several years. However, in the context of liquidity management, a prolonged period of low rates is less of a cause for celebration. “If you are a corporate with a lot of cash on the balance sheet then these are clearly very challenging times,” says David Morton, Asia Head of Corporate Banking at HSBC. This is because investing in such conditions is difficult for the corporate treasurer – and not only because of the increasingly elusiveness of yield. It also poses great challenges in the context of risk management.

Time to prepare

One danger that might stem from talk of a ‘new normal’ in interest rates is the complacency it could foster amongst corporate treasurers. If central banks do indeed decide to hold rates below historical averages in the years to come, corporates will be assured that any inefficiencies in their management of the working capital cycle can be papered over by their continuing access to cheap funding. But to rely on that would be a momentous mistake says Sandip Patil, Asia Head of Liquidity Management at Citi. Superimpose that with Basel III implementation in the banking industry and its impact upon credit availability, and this requires serious consideration.

The more sophisticated of Patil’s corporate clients recognise that now is the right time to prepare for the future, to establish good liquidity risk and control policies, to determine long-term funding needs, and to improve cash flow forecasting and working capital management. “Treasurers now have more time to plan and focus on core treasury infrastructure,” says Patel. “Given that a couple of years down the road we might be in a higher rate environment, I think this is an essential step at this juncture.”

For many, the low rate problem is compounded by the growing pool of cash sitting on the balance sheets of corporates across the globe. According to the estimates of the Economist Intelligence Unit (EIU), total cash positions held by non-financial companies range as high as $18.5 trillion globally, of which 41% is held in the Asia Pacific region. The initial focus then should be on making better use of the capital across the group, rather than on looking for higher yield. In most cases, a typical corporate with several hundred entities will have cash surpluses in some areas and deficits in others. “This is the time,” says Patil, “for them to try and figure out whether they can introduce a more centralised structure, such as a regional pooling solution, that will give them the ability to use their surpluses to fund shortages in a structured and sustainable manner.”

On this point, transaction banks are at least singing from the same hymn sheet. Liquidity pools are a tool that corporates should be seeing a lot of value in at the moment, Mireille Cuny, Global Head of Liquidity and Investment Solutions, Société Générale. “A global approach is increasingly important,” maintains Cuny. “That is something we are continuing to work on here at SocGen, to provide our clients with a global view of what is happening in their subsidiaries across different geographies.”

Chart 1: Euro-area, US, Japan and UK official interest rates

Source: Stanlib

Synthetic repatriation

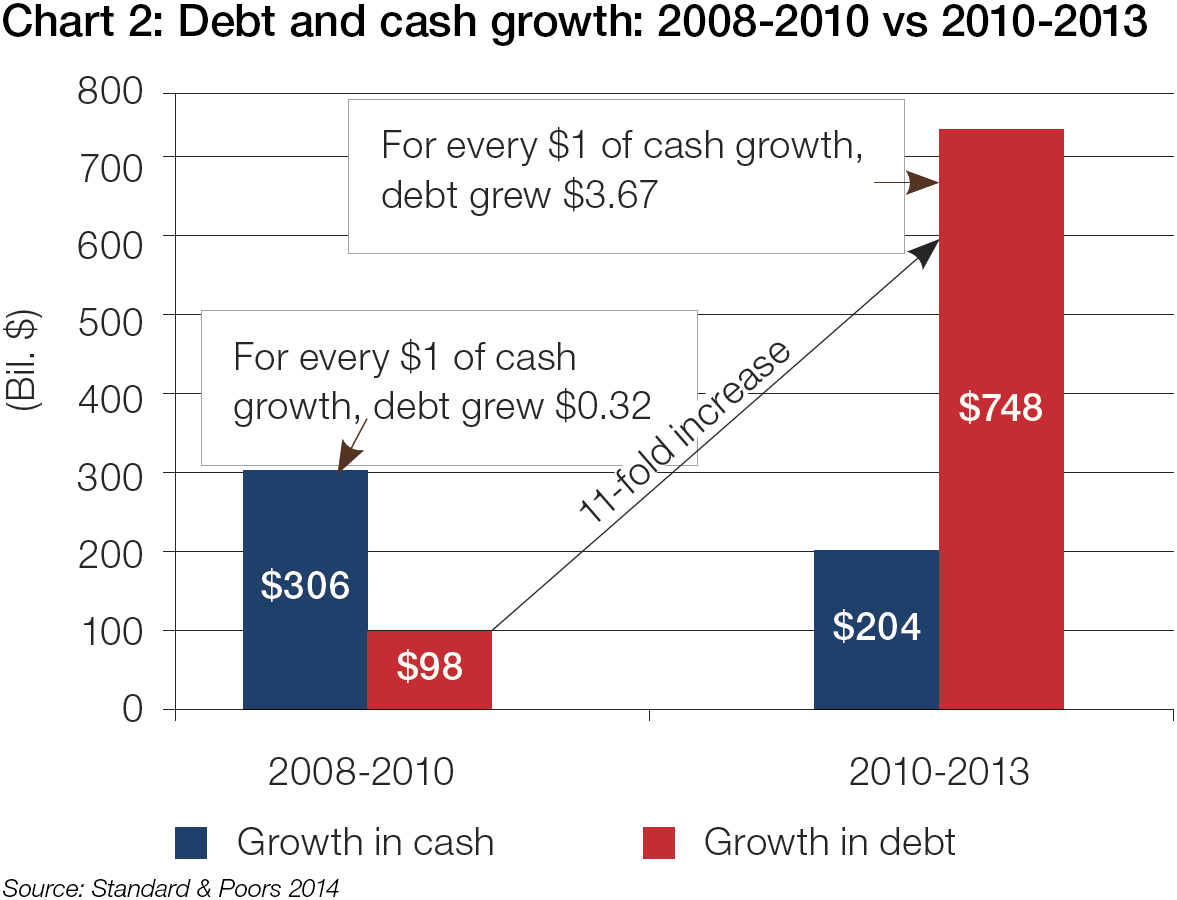

Using cash surpluses to balance shortages across the group could also have the benefit of reducing reliance on debt. After all, if companies are holding more cash on the balance sheet, why borrow to raise funds? However, a recent report by Standard & Poor’s appears to indicate that the very opposite is happening at large US companies. The report quantifies that since 2010, for every $1 of cash growth among issuers that S&P rates, debt increased by $3.67.

That may seem paradoxical at first glance, but there are two apparent reasons. Firstly, and most obviously, rates are so low right now that it is both easy and cheap to take on debt. The second reason is that most of this cash is being generated offshore. As it is often difficult to repatriate these balances, due to a combination of local regulation and domestic tax considerations, companies are instead choosing to supplement their domestic cash deficits with debt with debt issuances. It is a trend the report refers to as “synthetic repatriation”; a means for companies to deliver shareholder returns while avoiding the tax penalties for repatriating foreign earnings.

Help from your banks

The “synthetic repatriation” phenomenon is, of course, mainly a product of US tax law. A corporate headquartered in Europe or Asia should enjoy more flexibility in the way it manages cash across the group, particularly now that China is beginning to relax its foreign exchange restrictions. Assuming that it is possible to release cash, and that there is still some liquidity left after entities have been funded, treasurers must then figure out what to do with it. At this stage, taking a more proactive approach by speaking to banking partners and finding out about products that offer better returns often pays off. Such is the current environment that any additional return may not be that substantial, but the treasurer’s prerogative, of course, is to preserve the principle, not to make a profit.

“There are a few basis points available for those treasurers who are a little more proactive,” says HSBC’s Morton, adding that he finds it rather surprising how many companies still keep money in “rainy day accounts” that are not actively managed. A sensible first step would be to look again at the composition of the cash on the balance sheet. There is room to be a bit more adventurous and extend maturities of deposits when it comes to so-called ‘steady cash’, evidenced, says SocGen’s Cuny, by the growing attention in term deposits of up to 12 months, witnessed by the bank in recent years. “But even with longer maturity it is still very difficult to increase the return at the moment,” she adds.

Since deposit facilities suitable for the investing of operational cash must come with a cash or cash equivalent classification, the options are more limited still. Nevertheless, treasurers who maintain regular dialogue with their relationship banks should be aware of the growing range of new products and solutions most global banks now offer.

At SocGen, for example, fidelity premiums are offered the longer cash is held in the deposit account. “It is easy to administer because it is similar to deposits, and provides the same level of liquidity as it can be stopped every month or every three months, depending how it is tuned.” The fidelity premiums mean the return on the deposit is much improved, with rates on $1 ranging between 50 and 75 basis points, relative to the rate on a typical SocGen account which is presently around the 30 bps mark. “So they can double or even triple the return they would normally expect through this scheme.”

A perfect storm

An uncertain economic environment demands, more than ever, that treasurers spread risk by diversifying their investments. That might mean spreading deposits between a greater number of banking partners or, perhaps by using money market funds (MMFs).

In Europe, the past couple of years have borne witness to something approaching a perfect storm for investors at the short end. The funds, which manage approximately €1 trillion in assets – mainly on behalf of corporates and institutional investors – saw net outflows almost double last year to €69.2 billion. “If you look back five years, the market then was really dominated by bank supply,” says Bea Rodriguez, Head of Portfolio Management for Cash Management at BlackRock. But that is no longer the case. Banks began to deleverage and simultaneously term out their funding to make them more sustainable. That along with their declining credit quality left a shortage of investible short-dated money market instruments.

The consequence of all this is less liquidity and returns so wafer-thin that investors are often in the negative after accounting for inflation. “For a treasurer that will be a big concern,” says Rodriguez. The trap for the treasurer is that, in this environment, the incentive to stretch for yield is very strong, she explains. “The danger, of course, is that in most cases it will mean a drop in credit quality.”

For asset managers, the challenge is to develop liquidity funds that are able to provide their corporate clients with a incremental return without adding material risk. As a result of this endeavour, a mass of new products have arrived on the market in recent years, such as BlackRock’s Euro Assets Liquidity Fund. The fund was launched on to the market in 2013. The rationale was to move away from the requirements imposed by ratings agencies on AAA-rated MMFs. It gives the fund the freedom to go longer on investments they believe offer value and have less invested in near yield-less government securities.

But for the corporate treasurer, surely the peace of mind provided by credit ratings is half the point of MMFs? Are treasurers not raising questions with Rodriguez regarding risk management? “We say to treasurers, there is nothing in our Euro Asset Liquidity fund that is not in our prime rated fund,” Rodriguez says – the only difference is in the way the fund is weighted. “The biggest thing a treasurer needs to worry about is whether the fund is credit worthy. If you think that we are good as your prime rated fund manager then there is absolutely no reason that you should be uncomfortable with our Euro Asset Liquidity Fund offering.” Although the product might seem rather exotic to the European treasurer, similar structures have been used in some US funds for some time now. A year on since its launch, the model is now beginning to gain a foothold in Europe, surpassing the billion euro mark in March.

Chart 2: Debt and cash growth: 2008-2010 vs 2010-2013

Source: Standard & Poors 2014

What else is there?

If the absence of yield did not present a big enough problem for the MMF industry, there is also the prospect of unwelcome regulatory changes in the coming year. Although yet to be confirmed by the respective legislatures, regulators in both the US and Europe have announced proposals that will require funds to sell and redeem shares based on variable net asset value (VNAV) rather than the constant $€£1 per share asset value determined by amortised cost accounting. “That is a very different mindset,” says Rodriguez. “Some of our more sophisticated clients are happy with that as they understand that the variability will be very low as we invest in very short-term assets. But some corporates may still be a little concerned about that and decide they want to keep the money elsewhere.”

The problem is that for treasurers the number of suitable homes to deposit operating cash is shrinking fast. One alternative solution that has received a lot of attention of late is separately managed accounts (SMAs). These individually managed investment accounts have been around since the 1970s, and are now receiving increasing attention in light of all the uncertainty surrounding MMFs.

“We’ve had more conversations around those than at any other point in time,” Rodriguez remarks. For larger corporates holding substantial amounts of excess liquidity, SMA are at least worth considering, even if one loses the full liquidity benefits of being in a fund. “You can get around the maturity mismatch that is being created if you choose a SMA because you can be bespoke, and you can really tailor the risk to meet your needs,” she adds. “If you are smart, you will also understand the mismatches that are happening in the market structurally and allow yourself to be playing in them.”

It’s good to talk

Perhaps the overriding lesson that treasurers can derive from the above is that low rates, while problematic from a liquidity management perspective, can be countered. Often better rates on deposits can be achieved simply by proactively talking to banking partners and fund managers, and keeping up to date with new liquidity products and solutions.

Finally, while some experts forecast rates to remain far from their historical averages for some years to come, recent central bank announcements appear to indicate that – with the possible exception of Europe – they will begin to slowly push upwards again in the coming years. With that in mind, treasurers need to do all they can in the meantime to prepare for the future by improving, as much as possible, the way in which the group manages working capital. That, of course, is the hallmark of any forward-looking treasury.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.