If you are a corporate treasurer working in Asia, short-term investment strategies will almost certainly have been front of mind in recent years.

Wherever one looks, corporate cash piles are on an upward trajectory. Right now, non-financial companies in the Asia Pacific region are sitting on more idle cash – an average of $4.2 billion each – than firms from any other region listed in the S&P Global 1200. In South Korea, companies have around $270 billion idle on the balance sheet, while in China, the largest 500 companies have $405 billion. Japanese companies are the most cash rich of all, meanwhile, with a stockpile close to $3 trillion.

The question of what to do with such sizable cash balances is by no means a straightforward one, particularly in Asia. In this region, corporates have different financial infrastructures to negotiate; investment strategies – and the products and solutions which facilitate them – must therefore be tailored to different currency markets and different banking systems governed by different rules. Such diversity presents corporate investors with opportunities, for sure. But it also creates significant challenges.

Regulatory flux

We will turn to regulatory matters first. Asia’s famously heterogeneous regulatory regimes remain the most salient feature of the regional liquidity landscape, governing to a large extent what a business can or cannot do in terms of investment. In India, for example, interest payments on current accounts are prohibited, while in China interest is allowed but the pricing is regulated.

Change is in the air, however. The big story, as everyone surely knows by now, is China. Rewind several years and establishing any kind of liquidity pooling structure for renminbi (RMB) cash balances was close to impossible. In fact, moving any money in or out of China meant jumping through various bureaucratic hoops as set out by the State Administration of Foreign Exchange (SAFE). Not any more. Cross-border two-way sweeping – in RMB or foreign currency – is now commonplace across China, having been successfully piloted first in the Shanghai Free Trade Zone (SFTZ) over the course of 2013.

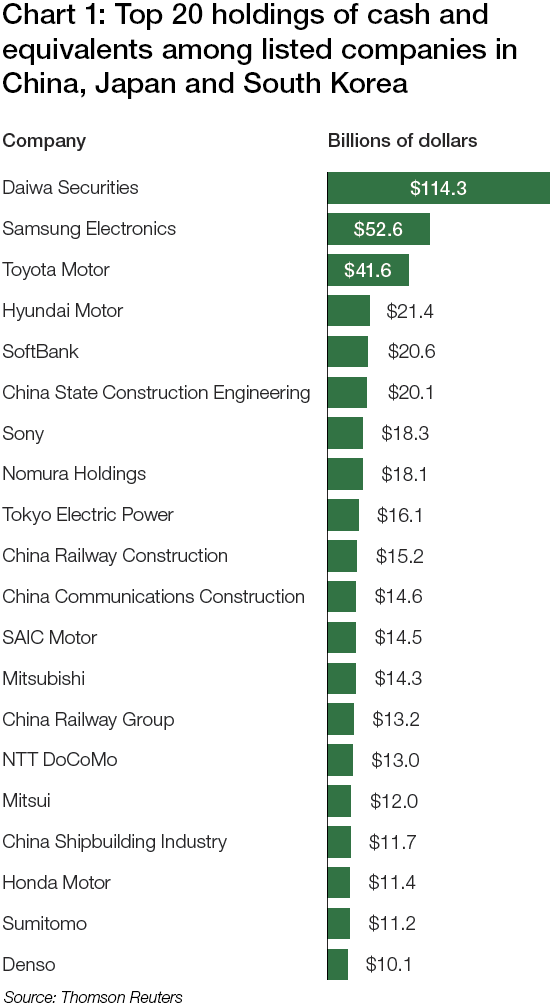

Chart 1: Top 20 holdings of cash and equivalents among listed companies in China, Japan and South Korea

Source: Thomson Reuters

“The entire cross-border commercial activity which was previously restricted in China is now completely allowed,” says Sandip Patil, Regional Head of Liquidity & Investments, Treasury and Trade Solutions at Citi, Asia. “If a multinational has a surplus in China and your subsidiary in Singapore is in deficit, they can now do inter-company lending and, vice-versa.” The increasing liberty businesses enjoy when handling Chinese yuan is reflected in the growing numbers using it for the purpose of trade and treasury funding. At the end of January, SWIFT reported that the currency overtook both the Canadian and Australian dollar as a global payment currency and, is now at number five globally.”

Although what’s happening in China has naturally dominated the headlines over recent months, they are not the only Asian country with a liberalisation agenda. “We have been seeing a similar trend in cross-border freedom being given to our customers across many markets including Malaysia and Thailand. It is certainly not fully liberal but it is directionally suggestive,” says Patil. What this means is that wherever your business is operating in Asia today, it is gradually becoming easier to put in place an efficient liquidity structure for corporates compared to the past. This liberalisation coupled with the growing cross-border businesses and better technology tools are the right reasons for clients to pursue treasury centralisation agenda, not just in Asia, but worldwide.

The ‘Bear Stearns rule’

Rules may be loosening in areas like foreign exchange, but in others – such as the banking industry – we are seeing just the opposite. The beginning of this year marked the introduction of the Liquidity Coverage Ratio (LCR) under Basel III, designed to ensure that banks have sufficient assets on hand to withstand any liquidity crunch the market might throw at them. It is expected that this will have a profound impact on both the structure of the banking sector across Asia and the various products and services it provides to corporates.

“Basel III obviously has an impact on the value of cash,” says Karin Flinspach, Head of Cash Products at Standard Chartered. The LCR requires banks to hold sufficient levels of high-quality liquid assets (HQLA) to cover their total net cash outflows over a 30-day stress period. This will change completely the view banks take on corporate deposits. Operational deposits will continue to be sought-after, but non-operational deposits, which have been assigned a higher run-off rate due to their perception as being less stable, are becoming a far less attractive proposition under the new rules.

Differences will also begin to emerge in how corporate deposits are treated from bank to bank, given the disparities we can observe in the pace of compliance across Asia’s banking sector. “There will be Basel III compliant banks, and non-Basel III compliant banks, and there will be a difference in the value of cash at each of these institutions,” says Flinspach.

A situation like this puts Asia’s corporate investors in quite an unenviable position. As we have seen, idle cash on corporate balance sheets is accumulating fast and banks are actively discouraging, through higher pricing, the depositing of anything other than operational balances.

Beyond term deposits

Bank deposits have long been the ‘go to’ liquidity solution for corporates in Asia. Might the regulatory changes we are currently witnessing precipitate a shift away from this model and greater uptake of alternative solutions, such as money market funds (MMFs)? That is a possibility. Interest in MMFs has been lukewarm in Asia in recent years since, following the financial crisis, many treasury mandates were changed limiting treasurers to use only bank deposits insured by governments. Moreover, with the market on many local currency MMFs – Thai baht or Indian rupee, for example – not especially deep or liquid, the difference between yields was minimal. There was simply very little incentive for treasurers to invest in MMFs, even if they were mandated to do so under treasury policy.

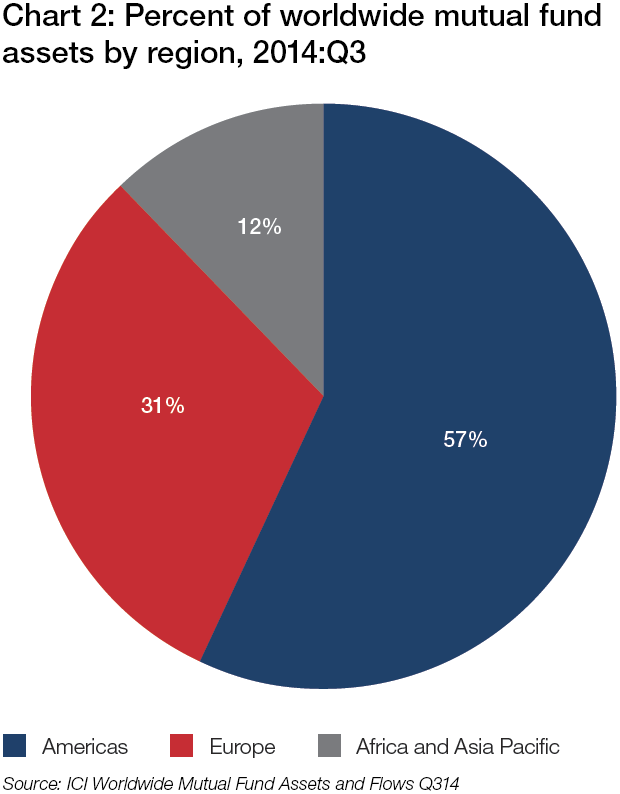

Chart 2: Percent of worldwide mutual fund assets by region, 2014:Q3

Source: ICI Worldwide Mutual Fund Assets and Flows Q314.

“I think that is slowly changing now,” says Martijn Stoker, Head of Liquidity and Escrow Product, Asia Pacific, J.P. Morgan. “The Basel III rules where the short-term deposit is seen as wholesale funding, it’s becoming much less attractive for banks and, as such, pricing is becoming less aggressive especially with the large international banks.” As a result, mutual funds such as MMFs are now beginning to regain ground lost during the financial crisis, largely as a result of funds flowing out of bank deposits and seeking higher returns. “There is definitely a shift happening, and I think it will accelerate once the regional and local banks adapt to a similar regulatory framework.”

However, even accounting for regulatory forces, there seems to be little chance of Asia’s MMF industry developing to size where it rivals its counterparts in the US or Europe – unless something extraordinary happens that is. According to the Investment Company Institute’s (ICI) Q314 report, Asian mutual funds represent a mere 12% of mutual fund assets worldwide, compared with 31% in Europe and 57% for the Americas. Clearly, this is an industry still in the early stages of development.

New rules, new products

Rumours of the demise in bank deposits across Asia may have been somewhat exaggerated, therefore. Product design in the banking sector has not taken long to catch up with the latest rule changes, in any case. Visit any one of your bank managers to open an account today and you will be faced with an almost bewildering array of options, including newly rolled out ‘rules-based liquidity’ or ‘Basel-friendly’ products, now being used to grow balances with attractive LCR value.

These come in various forms and configurations, but each ultimately shares the same objective: incentivising the type of corporate deposits that will receive favorable treatment under Basel III’s LCR. J.P. Morgan’s Liquidity Management Account (LMA), for example, measures the stability of client accounts over time, and then rewards them accordingly. If the balance remains consistently above a certain level – let’s say $10m – then everything below that level will be subject to a higher rate, not the overnight rate. “That’s how we encourage clients to leave their more stable balances with us, because they add value to the bank’s balance sheet,” says Stoker.

Citi has implemented Basel III recommendations and as a result, also recently added a suite of LCR-friendly accounts to its product range (for example, the 31-day notice account, is an evergreen deposit account with 31 day withdrawal notice feature for breakage). “On one hand, it helps the bank raise LCR friendly deposits and on the other, helps the clients gain better yields for their short-term surplus deposits,” says Citi’s Patil. “So far there has been a good reaction from the market” he adds. Citi has implemented a number of changes to its services and offering as a result of these developments and these changes are likely to be replicated by the broader market participants.

A region coming together?

All of Asia’s diversity notwithstanding, we can identify several distinct trends affecting the cash and liquidity landscape and, within that, corporate liquidity strategies and solutions. The regulatory landscape is changing with countries, liberalising restrictions around trade and FX, allowing corporates, more and more, to manage their liquidity on a par with their operations in western economies. The implantation of global banking regulation, meanwhile, is driving banks to be more creative with the solutions they devise for their corporate customers.

Knowing all of this, can we find an answer to the conundrum that is where to put Asia’s cash mountain? That will vary between companies. What works for a large US-domiciled corporate treasury that enjoys the most sophisticated of technological set-ups, will not necessarily play as well in the treasury of a smaller Malaysian mid-cap corporate, of course.

For the majority of MNCs, however, the best advice would be to make the most of cash balances across the group. Deregulation in China, particularly, has presented corporates with a fantastic opportunity to begin establishing pooling structures in RMB. Similar initiatives to increase economic competitiveness are taking place in Malaysia and Thailand. If trapped cash can be released from subsidiaries in surplus to fund other parts of the group with deficits then the corporate will be operating much more efficiently.

If having done all of this and there is still excess sitting on the balance sheet, however, then it may be worthwhile exploring either MMFs or what the banks call their ‘rules-based’ family of products to ensure that value isn’t being lost as a result of unfavourable pricing and low yields. The decision is for the treasurer to make, but the clock is ticking.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.