With recent events transforming the banking industry, corporates can be forgiven for focusing their attention on liquidity rather than on questions such as if, how and when they should be considering joining the SWIFT network. In the wake of events including the collapse of Lehman Brothers, LloydsTSB’s acquisition of HBOS and the decision by Goldman Sachs and Morgan Stanley to lose their investment bank status, corporates are more focused than ever on optimising their own liquidity. Although maintaining sufficient bank relationships is a key aspect of this, treasurers are also considering how liquidity can be maximised through solid cash management processes.

Changing priorities in a changing world

Corporate treasurers continue to place a high priority on the rationalisation of bank accounts. In the current environment, this needs to be balanced against the availability of funding.

Furthermore, they are focusing their efforts on maximising their own liquidity through solid cash and treasury management processes. Many corporate treasurers are going back to the basics of concentrating on receiving timely and accurate bank account information globally, visibility, transaction execution and their other core responsibilities within the treasury function. This often includes the establishment of payment and/or collection factories and shared service centres to realise economies of scale, drive automation and improve the order to cash/purchase-to-pay processes.

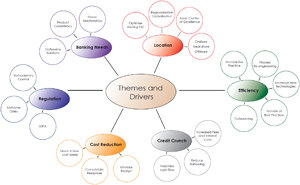

When companies embark upon this re-engineering journey there are a number of factors to consider:

Diagram 1: Considerations when rationalising bank account structures

In this Business Briefing we look at how the outsourcing challenge can be applied to a commodity such as core payments processing. We also consider how this may provide a path to full business process outsourcing (BPO) using SWIFT as one, but not the only, enabler.

The SWIFT approach

If we revisit the subject of corporate access to SWIFT, we can begin to see how SWIFT can become the enabler to achieving many of these objectives. After all, some 350+ corporates are already accessing SWIFT either directly or indirectly and this number is set to increase as SWIFT makes it easier and cheaper to access its network.

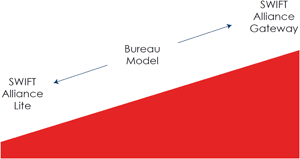

SWIFT has plans to improve the standardisation of messaging and processes including the new Bank Account Mandate (BAM) process, ISO20022 and exceptions and investigations. It also plans to implement trade finance messages and enhance its existing FIN message type. It has launched a new interface product, Alliance Lite, targeted at the mid-market enterprise which provides access to SWIFT over the internet via a USB stick. There are significant opportunities for the banks to harness these developments in partnership with SWIFT, to leverage the introduction of SEPA (Credit Transfer and Direct Debit) and the Payments Services Directive (PSD) for the benefit of their corporate clients as they look to re engineer their processes.

Diagram 2: The Connectivity Scale

What a SWIFT solution offers to corporates:

Open standards

Single channel

Non-proprietary

Multi-bank

Secure

Resilient

Integrated

Low cost

Scaleable

Outsourcing

Connectivity alone is not enough, however. Many banks today are reviewing how they leverage the different access options, their own solutions and use of ‘best of breed’ technology partners to deliver real value-added solutions to their clients with outsourcing a possible option.

Outsourcing is defined as subcontracting a process, such as product design or manufacturing, to a third-party. The decision to outsource is often made in the interest of reducing costs, redirecting or conserving energy directed at the competencies of a particular business, or to make more efficient use of resources. Outsourcing has been part of the business lexicon for well over 20 years and is certainly not an uncommon term in the world of corporate treasury operations.

However, the word outsourcing usually sets emotions running high within businesses of all shapes and sizes as those undertaking the processes/tasks identified to be outsourced often feel threatened – and for good reason. Outsourcing has historically resulted in those cost reductions referred to above being realised through job losses in many cases. The journey along the outsourcing road is a difficult one and the corporate treasury environment has not been immune over the last 20 years.

During this period we have witnessed a number of examples of outsourcing, ranging from a simple case of foreign exchange transactions to agency banking, automated cash pooling and the full blown outsourcing of the entire treasury function. Service providers are increasingly looking at innovative ways to harness their processing and transactional execution expertise, size, coverage and scale to deliver real value to their customers.

Drivers for outsource providers

Any change in strategy on the part of the service providers looking to win a slice of this business usually starts with a review of the key drivers and aims. By understanding these, treasurers may in turn have a better understanding of the types of product on offer. The following therefore lists these drivers from the outsource provider’s perspective.

A desire to grow business via its front-office.

Globalisation and leverage enhanced product offerings such as global liquidity solutions, SEPA and SWIFT connectivity for corporates.

A reduction in back-office costs by leveraging scale as a major payments processor.

A technology refresh utilising ‘best in breed’ partners for back-office payments processing and improved integration with corporate back office systems architecture.

Alignment with regulatory compliance/KYC and other external factors.

A wish to rationalise its own relationships.

What does the outsource solution need to cover?

Any decision to outsource will obviously need to deliver tangible improvement on what is being done today; a positive ROI is essential. Companies looking at these issues often share common characteristics and needs. Many organisations today accept they need the banks as an intrinsic component of the final solution and they share very similar needs in terms of systems connectivity and integration. These are a key part of the final product delivered. In response, service providers are beginning to develop solutions which really do address these requirements and deliver quantifiable benefits to their clients.

HSBC’s solution

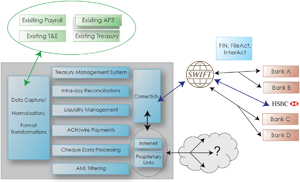

HSBC has developed a proposition defined as ‘Payments Managed Services’. This provides a variety of connectivity options within a secure environment and interfaces with the systems of HSBC’s clients.

The solution provides a multi-bank proposition via the SWIFT network with automated linkages to the various payment/clearing systems. It also offers a completely managed, and modular, service including data capture and transformation, limit checking, anti-money laundering screening, wire and ACH payments, warehousing, intra-day reconciliation and liquidity management all via a single provider. This model has the potential to grow where the client can ‘pay as they go’ and ‘pay as they grow’ as additional services can be included within the managed services framework.

Diagram 3: The HSBC Payments Managed Service

In setting up in-house banks, corporates are able to process all payments from central bank accounts on behalf of multiple subsidiaries. Integrated within the HSBC solution is a market leading Treasury Management System. The TMS supports all in-house banking features, including intercompany funding, intercompany netting and in-house bank accounting entries.

Commercially, all of this is offered as a bundled solution via a single contract with HSBC, whilst minimising the need for capital expenditure on the part of the client. HSBC believes this is laying the foundation for a full business process outsourcing solution.

Standard Bank Offshore Group

Approximately 25,000 clients – with 40,000 accounts and a deposit base of £2.1 billion – are handled by Standard Bank Offshore Group Limited. The company wished to improve its efficiency and STP rates, reduce operational risks, eliminate manual processes and reduce costs. In order to achieve this, following an RFP process, SBOG turned to HSBC.

HSBC was able to provide a solution that encompassed full management of SBOG’s global nostro account structure through a single portal capable of providing global payments, collection, reconciliation, real-time monitoring and full AML compliance capability. The solution also included the use of a SWIFT service bureau that provides an environment to improve straight through processing and reconciliation. Integral to meeting the requirements of SBOG was the chosen provider’s ability to deliver complete cheque book ordering and printing management, the outsourcing of cheque stops and returns, and both domestic and foreign cheque collections. These obligations were fulfilled through a combination of the bank’s own products and key third-party suppliers. Furthermore, the bank’s solution involved packaging inward and outward clearing solutions including deployment of the bank’s internet platform, implementation of electronic solutions for Bacs, multi-currency cheque outsourcing, agency clearing via SWIFTNet FileAct and the use of SWIFTNet FIN to support payments across accounts in 23 currencies for which the bank is acting as SBOG’s settlement agent. The provider is also responsible for managing SBOG’s SWIFT interface and infrastructure and managing/mapping data flows to the SBOG back office to achieve full reconciliation and exception reporting.

Jonathan Reynolds, Director – Operations at SBOG says, “I can advise that in the past year the volumes of our incoming payments have increased by 27% and volumes for UK clearing have increased by 8%. Prior to implementation of the outsource partnership, these activities were handled manually and the increases would have resulted in a significant increase in headcount. However, this has not been necessary due to the outsource service.

“Furthermore, the outsource service has enabled us to capitalise on our partner’s capability for the routing of payments and negated the necessity for us to either utilise a further payment routing application which, for the volume of our traffic, would have proven difficult to justify on a cost-benefit basis, or ensure all staff responsible for payment capture are sufficiently proficient in the complexities of international payments. We are now able to visit a change to our operating model, putting the capture of client instructions closer to the point of receipt and the staff who have the day-to-day contact with our clients.

A further benefit of the outsource service has been the removal of the need to manage and maintain our SWIFT connection. Whilst some activity is still required when SWIFT updates its packages, this is considerably less than when we were directly responsible for our own connection and software.

In summary, the outsource service has enabled SBOG, in its payment activities, to enjoy and offer the benefits of a large global bank whilst focusing on service delivery to its clients in its chosen key areas of expertise.”

The business case

Most decisions to incur any major expenditure will normally require a business case to proceed and outsourcing is no different. The decision on the solution detailed above will focus upon two options; installed or ‘in-house’ solution versus the outsourced or managed service.

The in-house solution will need to consider the following components: –

Computer operations.

Support.

Maintenance.

Communications.

Implementation.

Software licences.

Hardware and operating systems.

Disaster recovery.

Human Resources.

Depreciation of capital and equipment.

In contrast to the above, the outsourced option requires a sign-on and annual service fee which can be combined with all costs spread over the life of the contract. The outsource solution effectively becomes a pay as you go option with reduced investment and a greatly improved return on that investment.

Benefits

The benefits of migrating processes to the model described above can be summarised as follows:

Reduction in initial and ongoing costs.

Elimination of in-house software and licensing fees.

Elimination of in-house value added software application costs.

Elimination of ongoing development and project costs.

Reduction in support maintenance costs.

Reduced operational costs.

Provides enhanced speed to market.

Costs spread over the life of the contract.

Full access to best of breed banking services.

Solutions such as HSBC’s may also bring the following benefits:

Future proof outsource solution.

Compliant with regulatory and SEPA rules.

Scaleable.

Bureau hosted in fail-safe 24/7 dual data centres.

SWIFT used as a secure delivery channel or other secure FTP.

Full transaction audit trails.

Variable cost model.

All contracting is undertaken with the service provider.

Conclusion

The decision to outsource is a delicate one. Service providers are moving away from using the word outsourcing to avoid misinterpretation. This is more about delivering real value to their clients and HSBC, for example, has decided on a proposition which uses best in breed components and puts the client at the heart of the solution. It also positions the bank to expand this model by including additional services through an enhanced Application Service Provider (ASP) proposition within the bureau offering – effectively a ‘one-stop shop’ with HSBC.

In essence, these types of solutions put connectivity to work for the client. This modular type approach, using best in class components, allows the client to build out from a foundation of SWIFT connectivity to include: data mapping from/to legacy back office formats; overnight, intraday or real-time reconciliations and exception reporting; filtering and capture of payments against AML checklists; bulking of payments into cost-effective ACH-formatted files; use of SWIFTnet FIN and FileAct to connect to banking partners.

HSBC

HSBC has global coverage and local capabilities to provide you with innovative banking, cash management and cash investment solutions tailored to your needs.

HSBC Global Transactional Banking – provides transaction banking services to corporations, financial institutions and non-bank financial institutions globally. HSBC Global Asset Management – the core investment platform of the HSBC Group, our products and services include Global Liquidity Funds, a range of cash management investment vehicles for corporate and institutional clients.

HSBC Global Markets – specialises in foreign exchange, credits and rates, structured derivatives, equities and debt, equity and equity-linked capital markets. In addition to continued investment in products and services, we develop long-term relationships with our clients and deliver the highest level of service at regional and local levels.

The HSBC Group is one of the largest banking and financial services organisations in the world and has around 10,000 offices in 83 countries and territories. http://www.hsbcnet.com/hsbc/solutions

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.