Bulk payments and collections have become a pitfall for global treasury

Treasurers at large multinational companies have to use a multitude of tools to monitor their cash, to control their working capital, to maximise inter-company netting and to keep a close eye on subsidiary cash forecasting.

In principle, a treasurer can receive data feeds providing intra-day information on all the accounts and transactions of the Group. It is also technically possible for the same treasurer to initiate payments and collections from bank accounts all around the world, but this implies a multitude of e-banking solutions. Another solution is to streamline payments and receivables processes by centralising them in a shared service centre or a payments factory using single bank accounts in each country.

However, in a world where tax, legal and financial infrastructures remain stubbornly different, a consistent ‘one country, one bank and one bank account’ setup is never achievable in practice. Despite the introduction of a common currency in the EU, the advent of truly efficient pan-European payment systems still lies several years ahead. Europe remains a fragmented environment for transaction initiation and processing. Each country still has its own domestic payments and collections systems. These systems all use different messaging protocols and format standards.

So how can a company make cost effective payments (especially bulk payments) and collections across all these systems? And how can it effectively manage cash?

The w1se Corporate e-Banking application and MA-CUG services of KBC offer solutions to these problems.

A ‘w1se’ solution

w1se Corporate e-Banking offered by the KBC Group is a multi-currency, multi-country, multi-language, multi-user gateway, running on a common server and accessible through the internet from any location in the world.

There is no need for on-site implementation, a characteristic of most traditional electronic banking solutions, and staff worldwide all use the same application and databases. The system is very flexible and can be tailored to meet the company’s individual requirements and to match its organisational structure – particularly those with multiple operating units in several countries.

w1se provides direct access to manage and monitor local bank accounts, supporting the full range of local payment and collection systems in all countries covered by the KBC Group and providing remote access to accounts held at over 200 other banks worldwide. Using w1se corporate e-Banking, a treasurer can centralise liquidity positions and yet still initiate payments and collections by using less expensive local payment systems for their bulk transactions.

KBC Group’s strong position in Central Europe strengthens the strategic importance of the w1se Corporate e-Banking solution. KBC Group owns major banks in Hungary, the Czech and Slovak Republics and in Poland. Any company can benefit from w1se, but the application has been designed specifically for corporate customers who are looking for a single solution covering all their electronic banking needs in many countries.

The w1se concept

KBC Group invested over several years to develop the w1se Corporate e-Banking, aiming to create as much value as possible for its customers by taking maximum advantage of web based technology. The concept is simple – replace a host of domestic e-banking applications in several countries with a single system.

w1se facilitates multi-country transaction flows

Companies that expanded internationally before ERP systems allowed them to integrate payables and receivables across regions, often face big problems. Their different ERP systems may generate several different payment formats depending on the countries where they are active. w1se offers them several advantages:

w1se supports all the most common national payment formats.

w1se also supports the most common national electronic collection formats.

w1se enables efficient input of individual payments and collections – a built-in guidance logic defines the payment type and displays the appropriate payment or collection screen for completion.

w1se helps the user to initiate country-specific low value and high value payments, salary payments, global debit instructions, recurrent payments and (non) pre-authorised collections.

Companies with ERP systems that allow the generation of Swift MT101 files (Request for Transfer) can import mixed files containing both domestic and cross-border payments in different currencies and even different countries. The w1se infrastructure ensures a seamless interface from the various KBC Bank entities and partner banks all the way to the end user.

National and international file formats supported by w1se

Belgium

Netherlands

France

Germany

Czech Republic

Slovakia

Poland

Hungary

UK

USA

SWIFT

Payments

✔

✔

✔

✔

✔

✔

✔

✔

✔

✔

✔

Collections

✔

✔

✔

✔

✔

✔

✔

✔

Information Reporting

✔

✔

✔

✔

✔

✔

✔

✔

✔

✔

✔

Super User concept

‘Super Users’ are appointed within the company by the company’s management. They are entitled to create and delete users who may access the company’s w1se contract and administrative set-up.

The advantages of this concept are:

Super Users define the roles, entitlements and authorisations of users having access to the w1se application around the world.

The impact of any staff turnover is reduced, as Super Users can create new users on an as-needed basis and grant them specific authorisations within the w1se application.

In fact, w1se enables companies to create an e-Banking access framework that fully corresponds to their organisational structure. Geographically separated departments, branches and/or subsidiaries can individually access the same application and databases.

‘State-of-the-art’ security

Security is a key issue in e-Banking. Therefore, Isabel has been selected as the security provider for w1se.

Isabel secures e-Banking and e-Commerce applications for more than 30,000 companies in Europe. Its security application, based on Public Key Infrastructure, has an excellent proven track record.

Isabel’s security platform uses a smart card (containing the user’s secret key). w1se Corporate e-Banking verifies the user’s certificate and his/her entitlements any time he/she tries to access the application or sign any payment or collection instruction.

Powerful information reporting tools

Proper financial management is based on timely, accurate and comprehensive information. Users can retrieve account information or bank statements for consultation on-line, for the generation of pre-formatted reports or for export to other database applications in multiple formats.

w1se supports:

Intra-day reporting, either generated automatically, upon request or at pre-defined times.

End-of-day reporting.

Bank statements which can be made available to various employees at different locations.

Account information which can be downloaded in country-specific formats.

Flexible generation of standardised reports.

For corporates with advanced account reporting needs, KBC offers an add-on tool installed on a local PC. This offers a wide range of extra reporting and data manipulation functionalities based on the account statements exported via w1se, such as:

Value dated balances and history.

Management of in-house (internal) current accounts.

Extensive search possibilities in the transactional database.

Easy integration into General Ledger and Cash and Treasury management applications.

“When migrating towards w1se, one of our Dutch branches wanted to keep the report of their former Electronic Banking solution. With w1se e-reporting, we were able to create even better customised reports then before.”

Ivo Mollee, Assistant Treasurer, Royal Wessanen NV

w1se user support

w1se is a multi-lingual application that allows the user to switch easily between languages (Czech, Dutch, English, French, German, Hungarian, Polish and Slovak). The w1se helpdesks, located in KBC entities in Western and Central Europe, provide support to the w1se users in their own language. The embedded shadowing function facilitates a high quality support by focusing on the customers’ specific issue.

Dominique Stevens

Treasury Manager for Europe, Middle East and Africa

FedEx Corporation Treasury department was looking for a secure web based banking platform that would:

Provide easy access to its local entities to electronic banking for payments initiation and information reporting.

Support its move towards a centralised payment factory.

Dominique Stevens, Treasury Manager for Europe, Middle East and Africa wanted to ensure that while FedEx operations continue to expand in Central and Eastern Europe, good controls and visibility was being kept centrally over payment and collection flows.

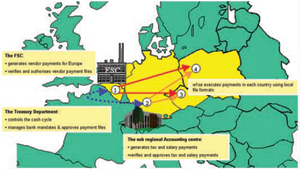

Ms Stevens comments: “w1se Corporate e-Banking successfully replaced local electronic banking systems for both Belgium and the Netherlands, but additionally it provided us with a single banking platform to handle cash management for our Czech and Polish operations. There are several parties involved in different phases of the working capital cycle that all required access to either the payments module, or to relevant bank information related to cash flows. Amongst these parties we have:

The Finance Service Centre (FSC), located in Brussels, which acts as a payment factory for FedEx in Europe. The FSC handles primarily vendor payments.

The sub regional accounting centre, based in Frankfurt for Central Europe, which handles critical tax and salary payments. Credit allocation and reconciliation of customer receipts is also handled at that level.

The Treasury department, also located in Brussels, which manages the treasury flows for all entities in Europe, Middle East and Africa.

Thanks to the web-enabled banking solution, payments are initiated and collection files are imported from multiple locations/countries, and made available to all respective authorised users on the platform regardless of their location. The verification and approval process of such transactions follows the same logic, and is done in accordance with the powers of attorney, which are maintained on-line in w1se.

Through one single w1se contract, FedEx manages the financial flows of eight different legal entities with accounts in several countries. The multilingual application covers 24 users sharing one global e-banking solution.”

FedEX initiates Central-European payments through w1se

Fedex locations:

Brussels

Frankfurt

Czech Republic

Poland

What makes w1se unique?

The possibility of managing all your accounts, worldwide, via one single uniform e-banking solution with the same look and feel, available in 8 languages.

One single database, accessible for all entitled users, at any location.

The ‘Guidance Logic’ concept helps you to use the correct payment screens, for all payments and collections and to achieve a higher degree of STP processable transactions.

Remote direct debit for your accounts at most KBC Group entities.

Flexible user-management via the Super User concept.

Some very large companies with high payment volumes may prefer to access their banks via SWIFT and use KBC’s MA-CUG gateway.

KBC MA-CUG: A flexible, added-value SWIFT gateway approach for corporates

Large multinational companies have been looking at ways to communicate with all their banking partners via one platform and one connection. SWIFT decided to grant corporate customers access to their secure network via MA-CUGs ( = Member Administered Closed User Groups), guaranteeing a communication gateway with a high level of reliability, availability and security.

KBC Bank, one of the major Belgian banks, strengthened its image as an innovative partner in e-business by launching the first corporate in the Benelux onto the SWIFT network via a MA-CUG in December 2002. Since then, a growing number of ‘corporate’ customers have joined this new ‘gateway’ to communicate with their banking partners.

KBC has gradually enlarged its MA-CUG service offering by adding new functionalities on top of the basic offering of sending ‘request for transfer’ payments instructions via FIN MT101 or receiving Customer Statements via FIN MT940 over SWIFTNet.

By offering access to SWIFTNet FileAct, KBC enables corporate customers to exchange structured payment files and account reporting with the Bank in a secure and reliable way. SWIFTNet FileAct is particularly suited for bulk payments and bulk account reporting.

An important drawback of the MA-CUG concept is that a corporate must join the MA-CUG of each banking partner they are working with. KBC has bilateral agreements in place with over 220 (mostly corporate) banks worldwide and decided to offer that reach to its MA-CUG customers by creating a conduit function, covering both payments and reporting.

The KBC SWIFT Distributor functionality enables the corporate customer to forward his payment instructions through his KBC MA-CUG gateway, irrespective of where the corporate customer’s account is held.

Similarly, the KBC SWIFT Collector functionality allows a corporate treasury to centralise receipt of all his end-of-day or intra-day account statements via a single MA-CUG connection with KBC Bank. This implies that the account holding subsidiary instructs its bank to forward these statements to KBC Bank.

With the conduit service, the KBC MA-CUG solution fully responds to the requirements of multinational companies who want to centralise their transfer flows and treasury management in an integrated way and who look for a single, uniform gateway solution to communicate and exchange files with their banking partners worldwide.

KBC Bank

KBC Bank, the largest Belgian financial institution, has over 52,000 staff, servicing its customers in more than 40 countries worldwide. The Bank has the largest branch network in Central Europe through leading domestic banks that are part of the KBC Bank in the Czech and Slovak Republics, Poland, Hungary, Slovenia, Russia and in most of former Yugoslavia. The cooperation agreement with the IBOS Worldwide Banking Alliance extends our geographic coverage to the whole of Europe and North America.

Both KBC and NLB Slovenia are proud to have been selected by ‘the Bankers’ magazine as the best bank in 2005 in their respective countries. This award reflects the full range of domestic, crossborder and cross-currency liquidity management services and our commitment to providing customized corporate cash management solutions. KBC has an impressive track record as innovator, being the 1st bank to launch cross-border notional cash pooling and to implement corporate access to SWIFT via a MA-CUG solution. W1SE Corporate e-Banking illustrates our continued commitment to corporate cash management. Covering 9 European countries, supporting the local languages, all domestic payment and collection instruments, national and common international file formats and a flexible report generator, W1SE makes remote initiation of domestic direct debits as easy as can be.

KBC specializes in multi-bank solutions, including multi-bank cross-border cash concentration. With more than 220 bilateral bank-to-bank contracts in place, KBC enables multinational corporates to manage their accounts with third party banks using W1SE or our SWIFT MA-CUG solutions.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.